AI for Sustainability

CSRD Compliance in 2026: New Scope, Thresholds, and Reporting Timeline

The 2026 CSRD guide for enterprises: what Omnibus I changed, who remains in scope under the new EUR 450M threshold, and how AI automates ESRS reporting.

Sofia Fominova

Apr 19, 2026

TL;DR: The EU's Omnibus I Directive, in force since 18-19 March 2026, raised the CSRD scope threshold so that only companies with more than 1,000 employees AND more than EUR 450 million in net annual turnover must report, cutting the in-scope population by approximately 80 to 90 percent. The "Stop-the-Clock" Directive pushed Wave 2 reporting to 2028 (on FY 2027 data) and Wave 3 to 2029 (on FY 2028 data). For the roughly 5,000 enterprises still inside the scope, the full European Sustainability Reporting Standards (ESRS) disclosure workload remains, and AI-driven data infrastructure is now the practical path to meeting it.

Key Takeaways:

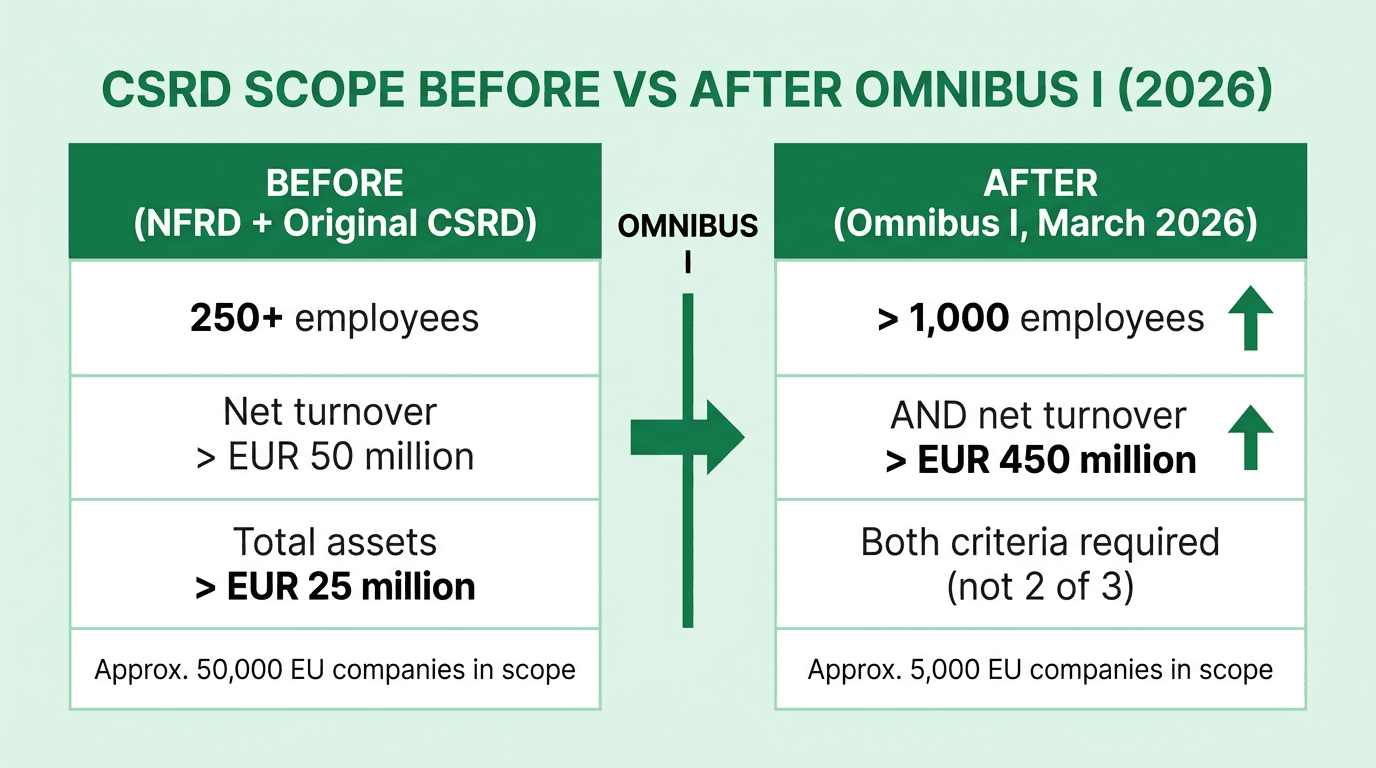

The Omnibus I Directive, published in the Official Journal on 26 February 2026, narrowed CSRD scope from roughly 50,000 to approximately 5,000 companies (Dcycle, 2026).

New mandatory thresholds are cumulative: more than 1,000 employees AND more than EUR 450 million net turnover, replacing the original 2-of-3 NFRD criteria.

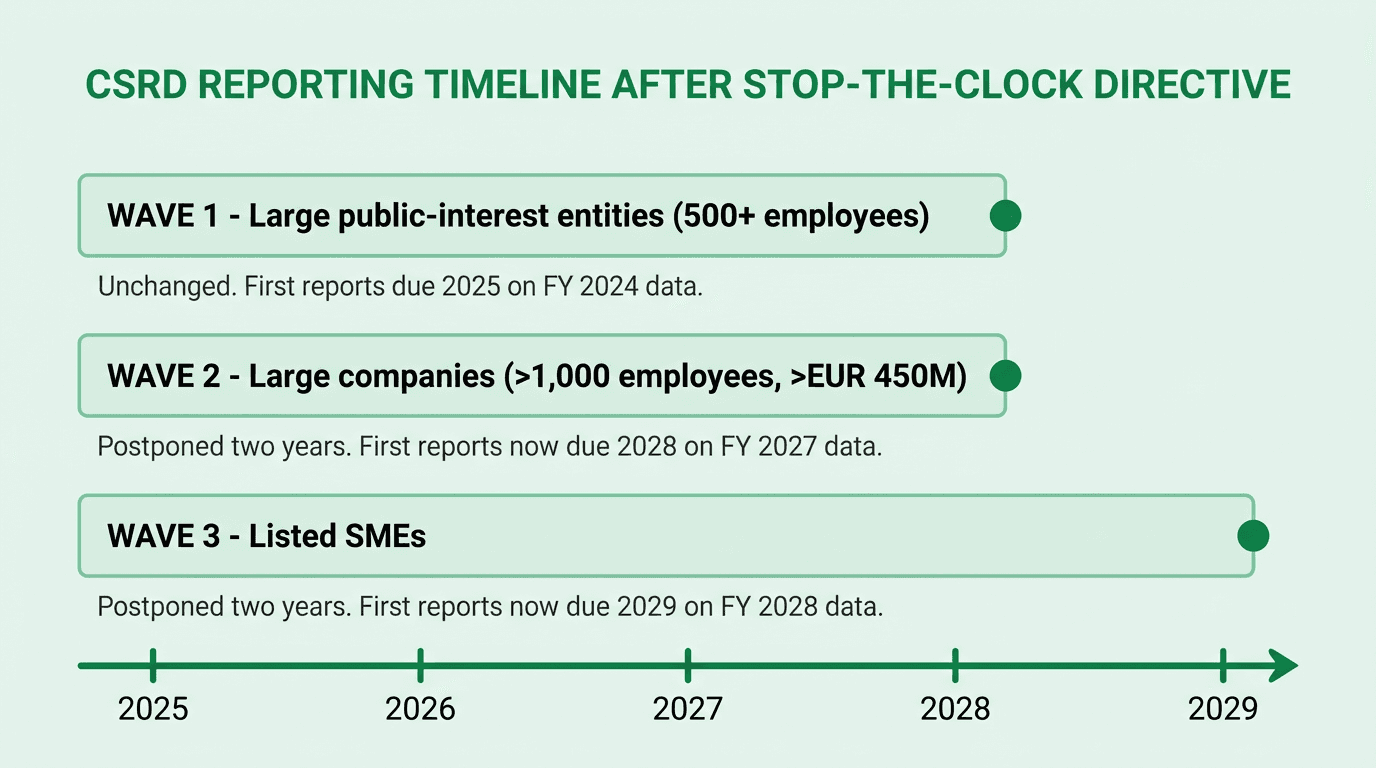

Wave 2 large companies now report in 2028 for fiscal year 2027; Wave 3 listed SMEs report in 2029 for fiscal year 2028 (Stop-the-Clock Directive, 2025).

Non-EU parents with more than EUR 450 million in EU-generated turnover remain in scope via a qualifying EU subsidiary or branch.

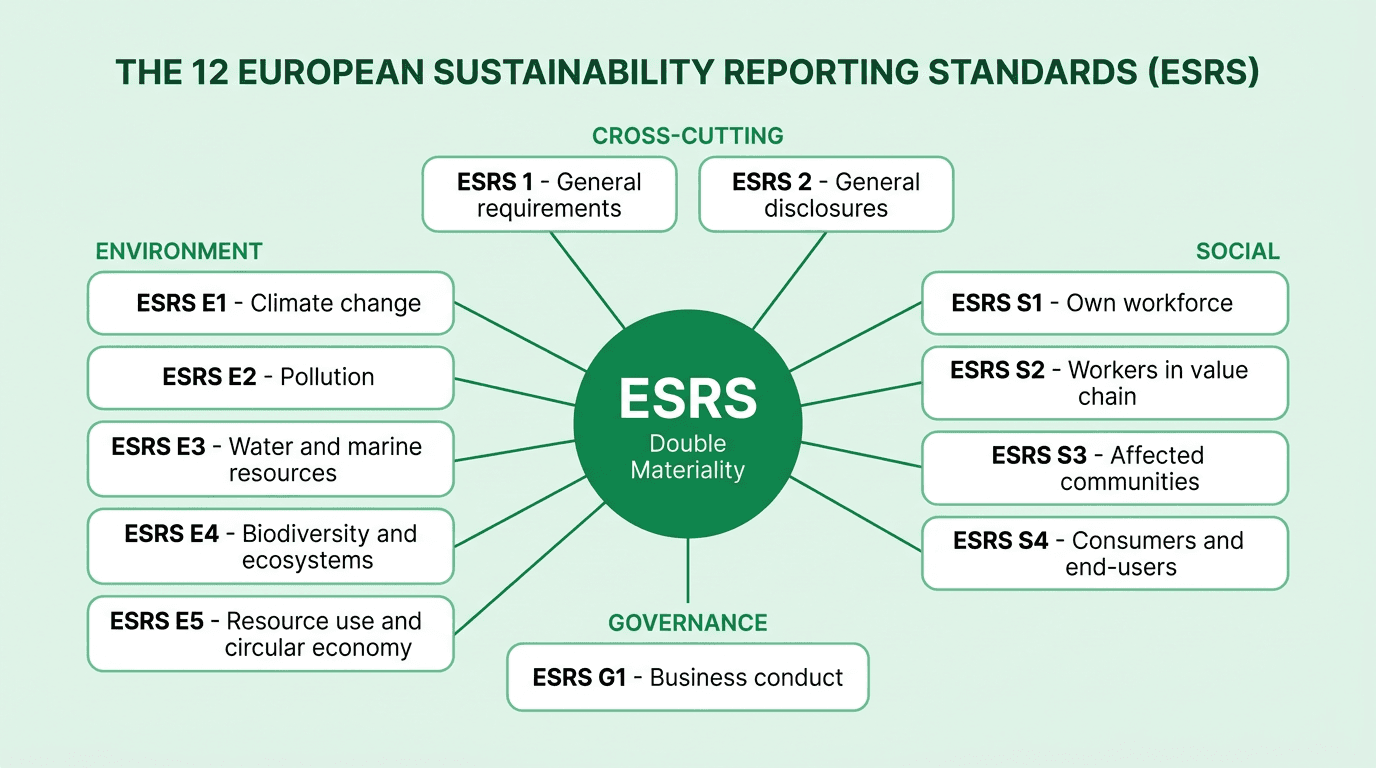

Double materiality, third-party assurance, and the 12 ESRS remain the disclosure baseline for in-scope companies; EFRAG's simplified ESRS, expected mid-2026, reduces mandatory data points by approximately 61 percent.

Member States must transpose the Omnibus changes into national law by 19 March 2027.

Introduction

Net0 is an AI infrastructure company that builds intelligent systems for governments and global enterprises, with a sustainability vertical that automates regulatory reporting across more than 30 frameworks, including the Corporate Sustainability Reporting Directive (CSRD). CSRD compliance in 2026 has been reshaped by the Omnibus I simplification package, which dramatically reduced scope while preserving the underlying ESRS disclosure architecture for the largest enterprises. This guide explains exactly who remains in scope after Omnibus I, how the reporting timeline was rewritten by the Stop-the-Clock Directive, what did not change, and how AI infrastructure compresses the reporting workload for the companies still required to file.

What changed under the 2026 CSRD Omnibus

The Omnibus I simplification package is the most significant revision to EU sustainability reporting law since CSRD was adopted in 2022. It introduced two separate but linked directives: the Stop-the-Clock Directive (adopted and in force 17 April 2025) and the substantive amendment directive (Directive EU 2026/470), published in the EU Official Journal on 26 February 2026 and entering into force on 18-19 March 2026, according to Mondaq's legal tracker.

The three headline changes:

Scope is narrower and stricter. Companies must now cross both employee and turnover thresholds, not two of three criteria.

Deadlines moved. Wave 2 and Wave 3 reporting are each postponed by two years.

Data demands are being simplified. EFRAG's revised set of European Sustainability Reporting Standards, expected mid-2026, is reducing mandatory data points from approximately 1,100 to around 430, a 61 percent reduction.

Who is in scope under the new CSRD thresholds

A company is in scope of the 2026 CSRD if it crosses both of the following thresholds simultaneously, tested on successive balance sheet dates:

More than 1,000 full-time equivalent employees (annual average), AND

More than EUR 450 million in net annual turnover

This replaces the original 2-of-3 framework (250+ employees, EUR 50 million turnover, EUR 25 million balance sheet assets). According to financialregulations.eu (2026), the change removes approximately 80 percent of previously in-scope entities, including all Wave 3 listed SMEs, Wave 2 companies with fewer than 1,000 employees, Wave 2 companies below EUR 450 million in turnover, and financial holding companies.

Non-EU parent companies remain subject to CSRD if consolidated EU-generated turnover exceeds EUR 450 million, provided the group has a qualifying EU subsidiary classified as a large undertaking, or an EU branch generating more than EUR 50 million in net turnover. Non-EU company reporting begins in 2029 for fiscal year 2028 data, unchanged by Omnibus I.

For enterprises now outside mandatory scope, voluntary disclosure remains strategically important: investors, banks, insurers, and customers increasingly require ESG data through supply chain and finance questionnaires, and EFRAG's Voluntary SME Standard (VSME) provides a proportionate framework. Many exempt companies continue to use CSRD-aligned reporting because capital markets and counterparties expect it.

The revised CSRD reporting timeline

The Stop-the-Clock Directive postponed the reporting obligations of Wave 2 and Wave 3 by two years, giving companies additional time to implement the new scope rules and simplified ESRS. Wave 1 (large public-interest entities with more than 500 employees that were already reporting under NFRD) was unaffected and continues reporting through the transition.

Member States must transpose the substantive Omnibus I amendments into national law by 19 March 2027, per Directive EU 2026/470, so national-level variations may emerge during 2026 and 2027. Enterprises with operations in multiple EU jurisdictions should track transposition timetables by country, because assurance, filing formats, and enforcement pathways are set at Member State level.

Several other 2026 developments sit alongside the CSRD changes. The EU Carbon Border Adjustment Mechanism entered its definitive regime on 1 January 2026, and California's SB 253 and SB 261 impose overlapping climate disclosure obligations on companies operating in the United States. Multi-framework reporters now have to reconcile ESRS with IFRS S1 and S2, GRI, and CDP disclosures within the same financial cycle.

ESRS and double materiality: what did NOT change

The European Sustainability Reporting Standards (ESRS) are the mandatory disclosure framework for in-scope CSRD filers. There are 12 standards in the current set: 2 cross-cutting, 5 environmental, 4 social, and 1 governance, each requiring structured disclosure under the four-pillar architecture of governance, strategy, impact and risk management, and metrics and targets.

The double materiality principle is unchanged and remains the conceptual core of ESRS. Reporters must disclose both:

Impact materiality -- how the company's operations affect people and the environment.

Financial materiality -- how sustainability issues affect enterprise value, cash flows, access to finance, and cost of capital.

A topic that is material under either lens triggers disclosure. This is a materially higher bar than single-materiality frameworks because it obliges companies to measure and disclose outward-facing environmental and social impacts even when those impacts are not financially material to the company itself.

Third-party assurance also remains required for in-scope filings. CSRD disclosures start with limited assurance and are scheduled to move to reasonable assurance once the Commission issues the relevant standards. Assurance providers must be independent and certified, and they rely on the same source data the company uses for its reporting. Weak or fragmented data systems translate directly into assurance findings.

EFRAG's ongoing technical work on simplifying ESRS reduces the mandatory data-point count but does not repeal any of the 12 standards, remove double materiality, or withdraw assurance requirements.

Non-EU companies with EU operations: the third-country threshold

Non-EU headquartered groups remain in scope of CSRD if three tests are met, according to the post-Omnibus rules documented by BDO (2026):

Consolidated EU-generated turnover exceeds EUR 450 million for each of the last two consecutive financial years.

The group has at least one qualifying EU subsidiary classified as a large undertaking under EU accounting rules, OR an EU branch generating more than EUR 50 million in net turnover.

The required report is issued at the consolidated third-country parent level and filed through the qualifying EU subsidiary or branch.

Third-country reporting begins in 2029 for fiscal year 2028 data. Non-EU reporting standards (a lighter-touch variant of ESRS) are being developed by EFRAG on the same timeline as the sector-specific ESRS, both postponed by the Council to 30 June 2026.

U.S.-headquartered multinationals face overlapping regimes: CSRD for EU-booked revenue, SEC climate disclosure rules at the federal level (pending litigation), and the California climate disclosure laws at the state level. IFRS-aligned reporting under IFRS S1 and S2 is increasingly used as the interoperability layer because more than 20 jurisdictions have formally adopted the ISSB standards.

How AI infrastructure accelerates CSRD reporting

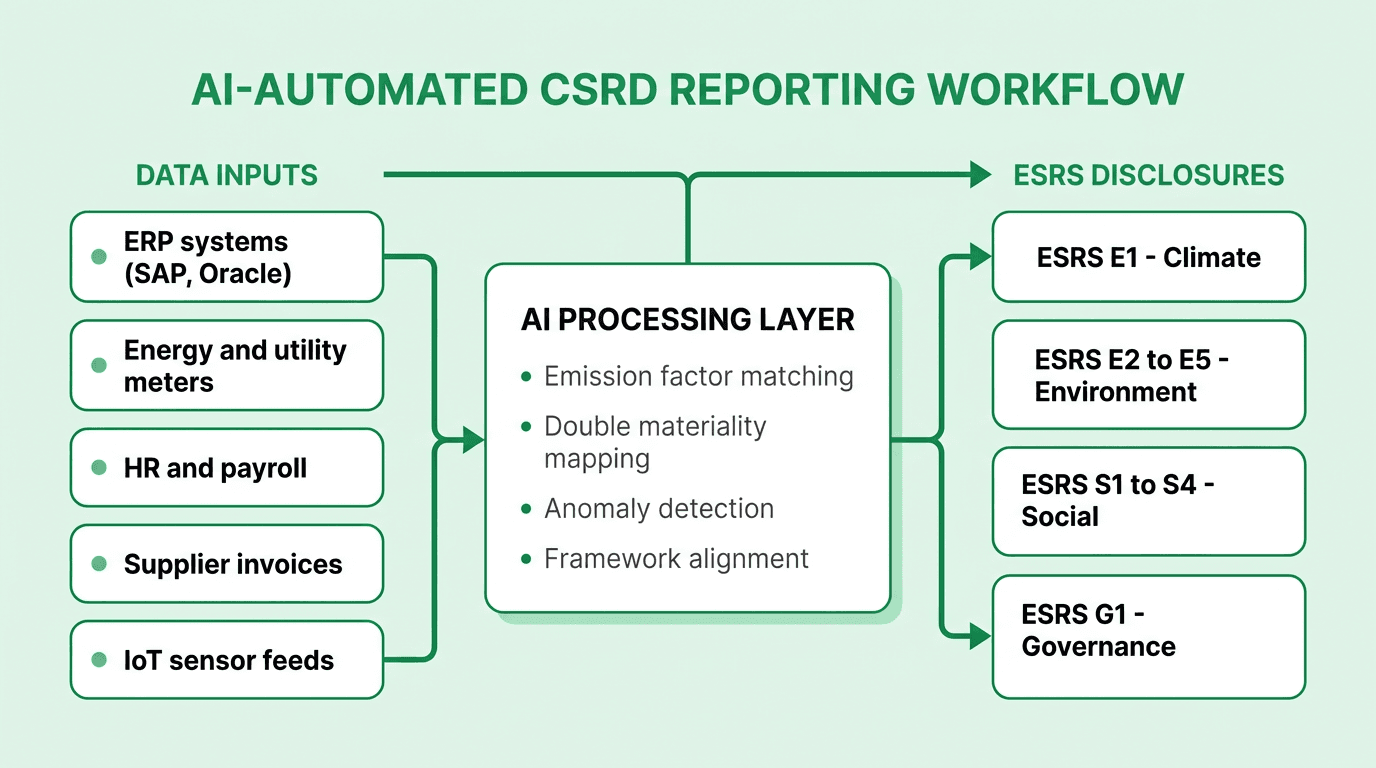

The 5,000 companies still in scope of CSRD after Omnibus I are disproportionately large, multi-country, and data-heavy. For these reporters, the reporting problem is not legal interpretation. It is data engineering at scale.

A typical CSRD filing requires structured data pulled from enterprise resource planning systems, energy meters, fleet management, HR and payroll, supplier invoices, travel platforms, and increasingly from IoT sensor feeds. The data then needs to be normalised, matched against tens of thousands of emission factors, aligned with ESRS data-point definitions, mapped through double-materiality logic to the 12 topical standards, and produced in machine-readable XBRL format for the European Single Access Point.

AI infrastructure addresses this workload at three layers:

Automated data capture. AI-powered pipelines for automated data collection ingest data from thousands of source systems, eliminating manual spreadsheet aggregation and the error rates that accompany it.

Intelligent classification and calculation. Machine learning models match transactional data to activity-based, production-based, or spend-based emission factors, compute Scope 1, 2, and 3 emissions in real time, and flag anomalies before they reach the assurance team.

Multi-framework alignment. A single data backbone produces disclosures aligned to ESRS, IFRS S1/S2, GRI, CDP, and GHG Protocol, rather than running each framework as a separate project. This matters because most in-scope enterprises file under three or more frameworks in parallel.

The measurable outcome is a shift from CSRD as a once-yearly crisis to CSRD as a continuous reporting capability, with live dashboards, audit trails, and scenario-ready data.

How Net0 supports CSRD compliance

Net0 applies its AI infrastructure directly to the CSRD reporting workload. The platform integrates with more than 10,000 enterprise systems, maintains a catalogue of more than 50,000 emission factors, and supports more than 30 sustainability reporting frameworks, including ESRS, GHG Protocol, CDP, GRI, IFRS S1 and S2, the EU Corporate Sustainability Due Diligence Directive, SECR, and ESG disclosure regimes globally.

Specific capabilities relevant to CSRD filings:

Double materiality automation. Structured workflows for stakeholder engagement, impact scoring, and financial risk quantification, producing an audit-ready materiality assessment mapped to the 12 ESRS.

ESRS E1 climate module. Full Scope 1/2/3 accounting covering all 15 Scope 3 categories, transition plan scenario analysis, and physical risk mapping.

Multi-framework output. A single source of truth produces ESRS, IFRS S1/S2, GRI, and CDP disclosures without re-keying data.

Continuous assurance readiness. Evidence trails, source-system lineage, and versioned calculation logs are retained by default so assurance providers can verify every number back to its origin.

Decarbonization planning. The same platform supports profitable decarbonization strategies, marginal abatement cost curve analysis, and target setting aligned to CSRD transition plan requirements.

Net0 is used by Fortune 500 enterprises and governments across four continents, with deployment options covering cloud, hybrid, and sovereign on-premise architectures. For regulated industries and national agencies, the same AI infrastructure is delivered with full data residency and sovereign control.

Book a demo to see how Net0 automates CSRD reporting end-to-end.

Frequently Asked Questions

Is CSRD still mandatory in 2026?

Yes. CSRD remains mandatory EU law in 2026 for companies meeting the new thresholds. Omnibus I narrowed scope but did not repeal the directive. Wave 1 large public-interest entities continue reporting on schedule, and Wave 2 and Wave 3 filings begin in 2028 and 2029 respectively under the Stop-the-Clock Directive.

What are the new CSRD thresholds under Omnibus I?

A company is in scope if it has more than 1,000 employees AND more than EUR 450 million in net annual turnover, both tested on successive balance sheet dates. Both criteria must be met; the original 2-of-3 test from the NFRD era no longer applies.

When do Wave 2 companies need to report?

Wave 2 large companies meeting the new thresholds must report in 2028 on fiscal year 2027 data, after the two-year postponement introduced by the Stop-the-Clock Directive adopted on 17 April 2025.

Does CSRD apply to US companies?

CSRD applies to US companies indirectly. A US parent group is in scope if its consolidated EU-generated turnover exceeds EUR 450 million for two consecutive financial years and the group has a qualifying EU subsidiary or an EU branch with more than EUR 50 million in turnover. Non-EU reporting begins in 2029 for FY 2028 data.

Has ESRS changed under Omnibus I?

The 12 ESRS and the double materiality principle remain in force. EFRAG is producing a simplified ESRS revision, expected mid-2026, that reduces mandatory data points by approximately 61 percent, from around 1,100 to around 430, without removing any of the 12 standards or the double materiality requirement.

Can AI automate CSRD reporting?

Yes. AI infrastructure automates the data collection, emission factor matching, double materiality mapping, ESRS alignment, and XBRL output required for CSRD filings. For in-scope enterprises running more than one reporting framework in parallel, AI platforms such as Net0 consolidate the underlying data pipeline and produce ESRS, IFRS S1/S2, GRI, and CDP disclosures from a single source of truth.