AI for Sustainability

Decarbonization: The 2026 Enterprise Guide to Science-Based Targets

A 2026 framework for building credible, science-based decarbonization strategies — covering baselining, target-setting, scenario modelling, and multi-framework disclosure for Fortune 500 enterprises.

Sofia Fominova

Apr 17, 2026

TL;DR. Decarbonization is the enterprise discipline of reducing greenhouse gas emissions across operations, supply chains, and products in line with a 1.5°C pathway. Setting credible decarbonization goals now requires a quantified Scope 1, 2, and 3 baseline, science-based targets validated by a recognised framework, a prioritised abatement roadmap, and disclosure against CSRD, CDP, IFRS S2, and the SEC Climate Rule. Net0, an AI infrastructure company for governments and global enterprises, provides the AI-powered measurement, simulation, and reporting layer that makes this workable at Fortune 500 scale.

Key Takeaways

As of the end of 2024, 4,205 companies had SBTi-validated near- or long-term targets, covering roughly 39% of global market capitalisation (SBTi Monitoring Report 2024).

Companies with SBTi-validated targets cut their Scope 1 and 2 emissions by 12.3% between 2020 and 2023, compared with a 3.7% increase across the global economy (SBTi Monitoring Report 2024).

Scope 3 accounts for an average of 75% of enterprise emissions and up to 99% in consumer-facing sectors (CDP Supply Chain Report 2024).

The EU's Corporate Sustainability Reporting Directive (CSRD) applies to ~50,000 companies and requires a Paris-aligned transition plan under ESRS E1 (European Commission, 2024).

McKinsey's 2024 abatement cost analysis found that roughly 25% of required 2030 emissions reductions can be delivered by levers with a negative or near-zero marginal cost — meaning they pay for themselves (McKinsey Sustainability, 2024).

What decarbonization means for enterprises in 2026

Decarbonization is the systematic reduction of carbon dioxide and other greenhouse gas emissions from an enterprise's operations, energy use, supply chain, and products, with the goal of aligning the business with a 1.5°C pathway. It is not a single initiative. It is a multi-year capital allocation, procurement, and operating model problem that touches every part of a large organisation.

The decarbonization conversation has moved well past pledges. The UN Race to Zero's 2024 review found that 47% of companies with public net-zero targets lacked credible near-term interim milestones (Net Zero Tracker, 2024). Regulators, ratings agencies, investors, and customers are now distinguishing firms with quantified, audited, science-based decarbonization plans from those that rely on headline commitments and offset-heavy "neutrality" claims.

For a Fortune 500 enterprise, this means three things: emissions data must be financial-grade; reduction targets must be externally validated; and progress must be reported consistently across multiple disclosure frameworks that are converging but not identical.

The state of enterprise decarbonization

Several recent datasets give a precise picture of where large enterprises stand.

Target coverage. As of December 2024, 4,205 companies had SBTi-validated targets, roughly 39% of global market capitalisation. An additional 3,000+ have committed but not yet had targets validated (SBTi Monitoring Report 2024).

Progress where targets exist. Companies with SBTi-validated near-term targets cut their Scope 1 and 2 emissions by an average of 12.3% between 2020 and 2023. Over the same period, global energy-related CO2 emissions rose 3.7% (SBTi Monitoring Report 2024; IEA, 2024).

Scope 3 remains the blocker. CDP's 2024 supply chain data shows Scope 3 accounts for an average 75% of corporate emissions, rising to 99% in food, retail, and apparel (CDP, 2024). Only 41% of CDP respondents reported any Scope 3 category with reasonable assurance.

Disclosure is now mandatory in major markets. CSRD, CDP climate questionnaires, IFRS S2 (adopted in 30+ jurisdictions as of early 2026), and state-level rules like California SB 253 are making Scope 1, 2, and material Scope 3 disclosure legally required for large and foreign-parented companies.

The implication: a decarbonization strategy that was defensible in 2022 — a long-dated pledge and annual CSR report — is no longer sufficient. The 2026 bar is a quantified baseline, an externally validated target, an auditable roadmap, and machine-readable disclosures.

Why decarbonization now requires AI infrastructure

Enterprise decarbonization is a data problem before it is a capital problem. A global manufacturer might have 50+ legal entities, 100+ facilities, 10,000+ suppliers, and hundreds of product lines. Measuring, modelling, and reducing emissions across that footprint exceeds the capacity of spreadsheets, consultants, and point tools.

Three data challenges define the bottleneck:

Ingestion. Emissions-relevant data lives in ERP systems, utility bills, fuel cards, travel platforms, procurement systems, logistics telematics, and supplier disclosures. Most enterprises have 20+ systems that must be connected before any baseline is possible.

Classification and emission factors. Every transaction must be mapped to the correct emission factor — activity-based where possible, spend-based as a fallback. Factor libraries have 50,000+ entries across regions, fuels, grids, and years.

Scenario modelling. Once the baseline exists, leaders need to simulate the emissions and financial impact of thousands of possible interventions — fuel switching, electrification, supplier substitution, product redesign — to know which to fund.

This is an AI infrastructure problem. Net0's AI platform automates ingestion from 10,000+ enterprise systems, classifies activity data against 50,000+ emission factors, flags anomalies, and runs scenario simulations against financial and operational data. The same platform generates the formatted outputs required by CSRD, CDP, IFRS S2, and the SEC Climate Rule — a task that consulting engagements typically deliver once a year and that modern disclosure regimes now require continuously.

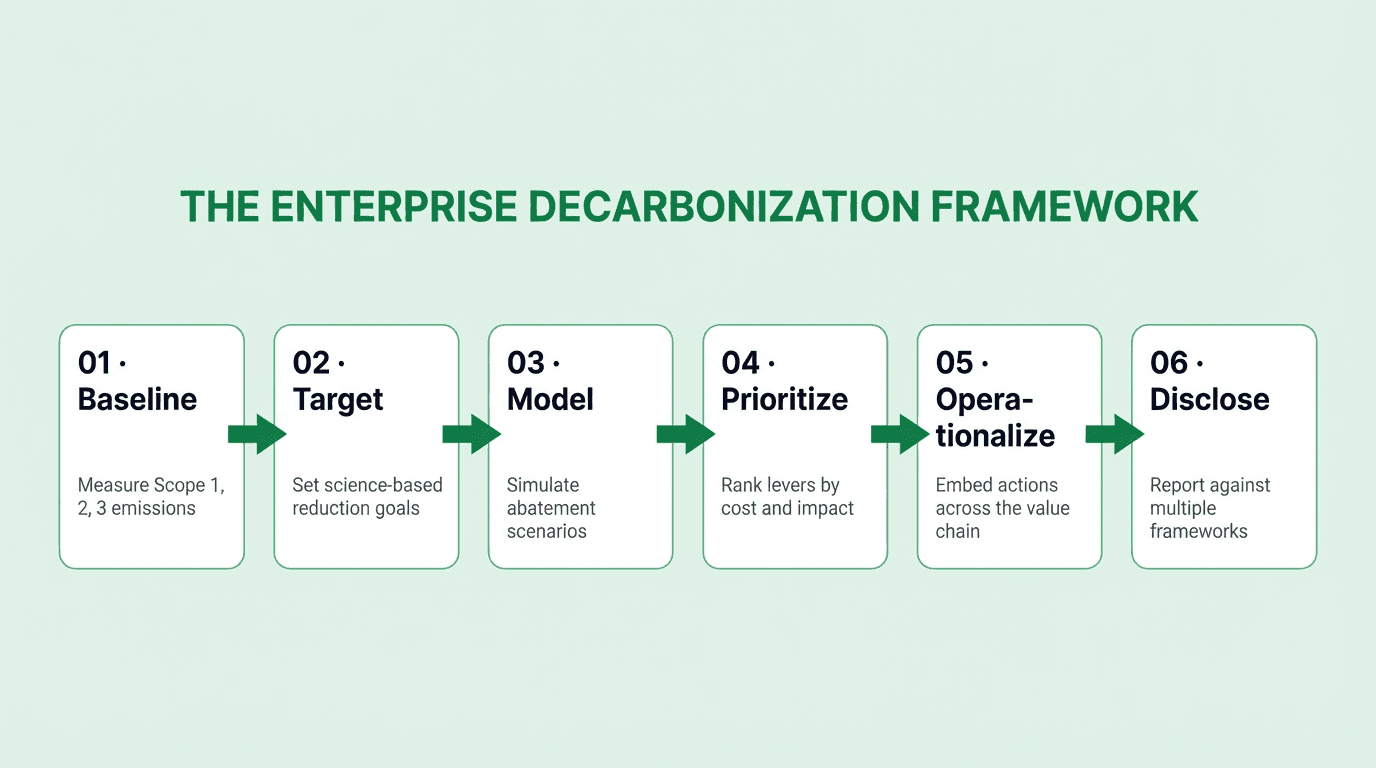

The enterprise decarbonization framework

Decarbonization for a large organisation follows six steps. Each step produces a deliverable that feeds the next, and each is amenable to automation.

Step 1: Build a quantified Scope 1, 2, and 3 baseline

Every credible decarbonization strategy starts with a GHG Protocol-aligned inventory covering Scope 1, 2, and 3 emissions. Scope 1 covers direct emissions from owned sources. Scope 2 covers purchased energy (with both location-based and market-based figures). Scope 3 spans 15 upstream and downstream categories — purchased goods and services, capital goods, transportation, use of sold products, and more.

The baseline must use a consistent methodology — see carbon accounting methodologies — and should identify the key data sources for each emission category. For most manufacturers and retailers, category 1 (purchased goods and services) and category 11 (use of sold products) dominate the footprint. Reasonable-assurance auditability should be the design target, not just completeness.

Step 2: Set science-based reduction targets

Once a baseline exists, targets are set using a recognised framework. The Science Based Targets initiative (SBTi) is the current market standard. SBTi requires:

A near-term target covering Scope 1 and 2 with at least a 4.2% annual absolute reduction (aligned with 1.5°C).

A Scope 3 target if Scope 3 exceeds 40% of the total footprint.

A long-term target consistent with net zero by 2050 or earlier.

Public disclosure and five-yearly revalidation.

For enterprises operating in the EU, the CSRD transition plan requirement under ESRS E1 effectively mandates a 1.5°C-aligned pathway as part of the annual sustainability statement.

Step 3: Model scenarios and abatement options

Targets without a roadmap are aspirational. This step generates and stress-tests abatement options using scenario modelling — typically a marginal abatement cost curve (MACC) augmented with time-phased capital requirements.

A robust scenario model answers three questions for every lever:

What is the abatement potential, expressed in tCO2e per year?

What is the net cost or saving per tonne abated?

What is the capital expenditure profile and payback period?

McKinsey's 2024 global cost-curve work estimates that roughly 25% of the emissions reductions required by 2030 can be delivered by negative-cost or near-zero-cost levers, dominated by energy efficiency, power sector decarbonization, and methane abatement (McKinsey Sustainability, 2024).

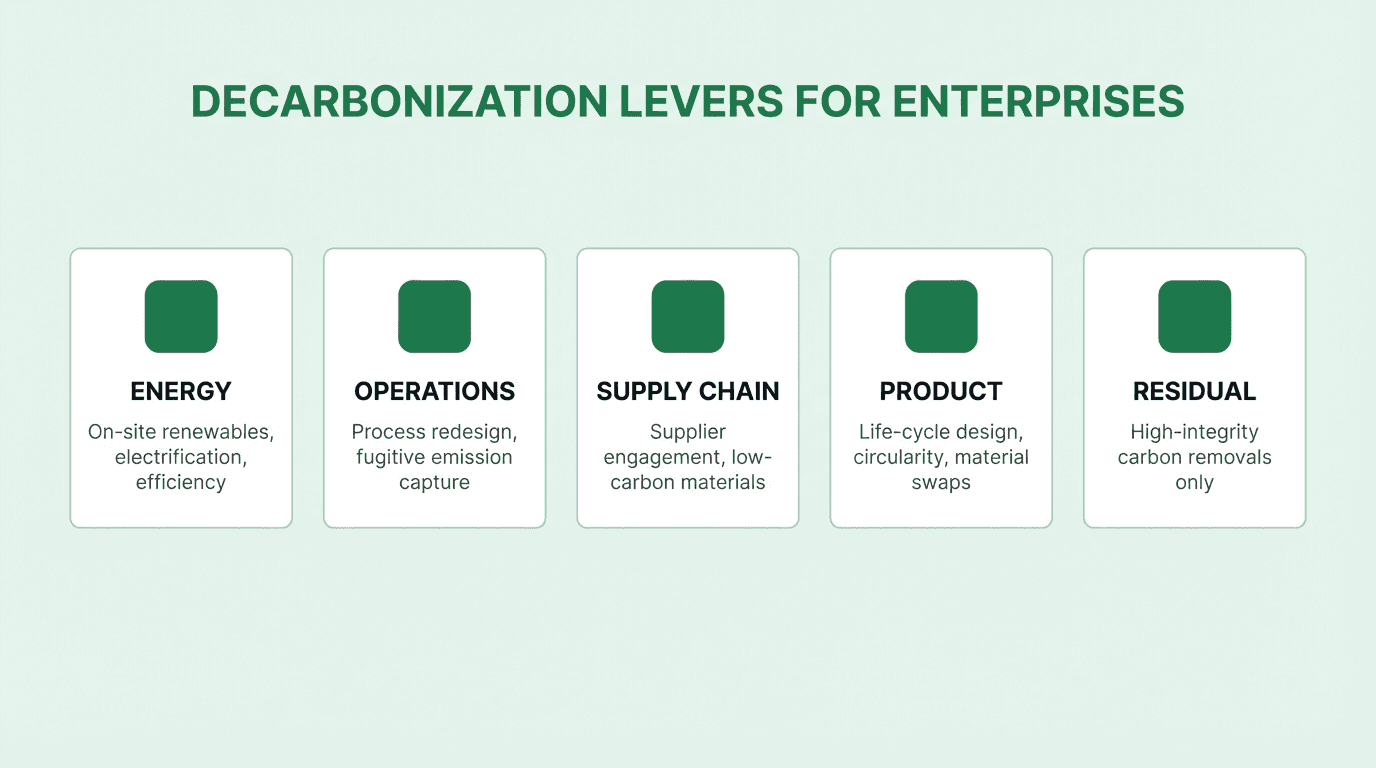

Step 4: Prioritise interventions by cost and carbon impact

With a validated scenario model, leaders can then prioritise. The goal of this step is a ranked portfolio of initiatives — the top decile that delivers most of the required abatement at the best economics.

Five lever categories cover the vast majority of enterprise opportunities:

Energy. On-site renewables, renewable PPAs, grid-aligned electrification, and efficiency upgrades. For most businesses, this is where the first 20–30% of reductions come from and where most negative-cost levers sit.

Operations. Process redesign, fugitive emission capture, electrification of heat, and fleet replacement.

Supply chain. Supplier engagement programs, low-carbon materials sourcing, and supplier-level target setting. See reducing upstream emissions for the supplier engagement playbook.

Product. Life-cycle-assessment-driven redesign, circularity, and material substitution. Addresses Scope 3 category 11 (use of sold products), which is the largest emission source for many OEMs. See product carbon footprint.

Residual. High-integrity carbon removals — used only for residual, hard-to-abate emissions, and only after reductions are exhausted.

For a formal approach to ranking these, the decision-making framework for decarbonization initiatives provides a repeatable methodology. The goal is profitable, not just aspirational, reductions — see profitable decarbonisation strategy.

Step 5: Operationalise across the value chain

A roadmap only reduces emissions if it changes operational decisions. This step embeds decarbonization into capital approval workflows, procurement scoring, supplier contracts, product design gates, and management incentives.

Operationalisation typically fails on data. Business unit leaders need near-real-time visibility into the emissions implications of their decisions — a capex proposal, a supplier change, a product reformulation. That requires the same AI ingestion and classification pipeline that powered the baseline, now exposed as dashboards and APIs to operational users. Supplier engagement is a specific operational workflow: see data collection challenges from factory emissions for the manufacturing case and Scope 3 myths for common traps.

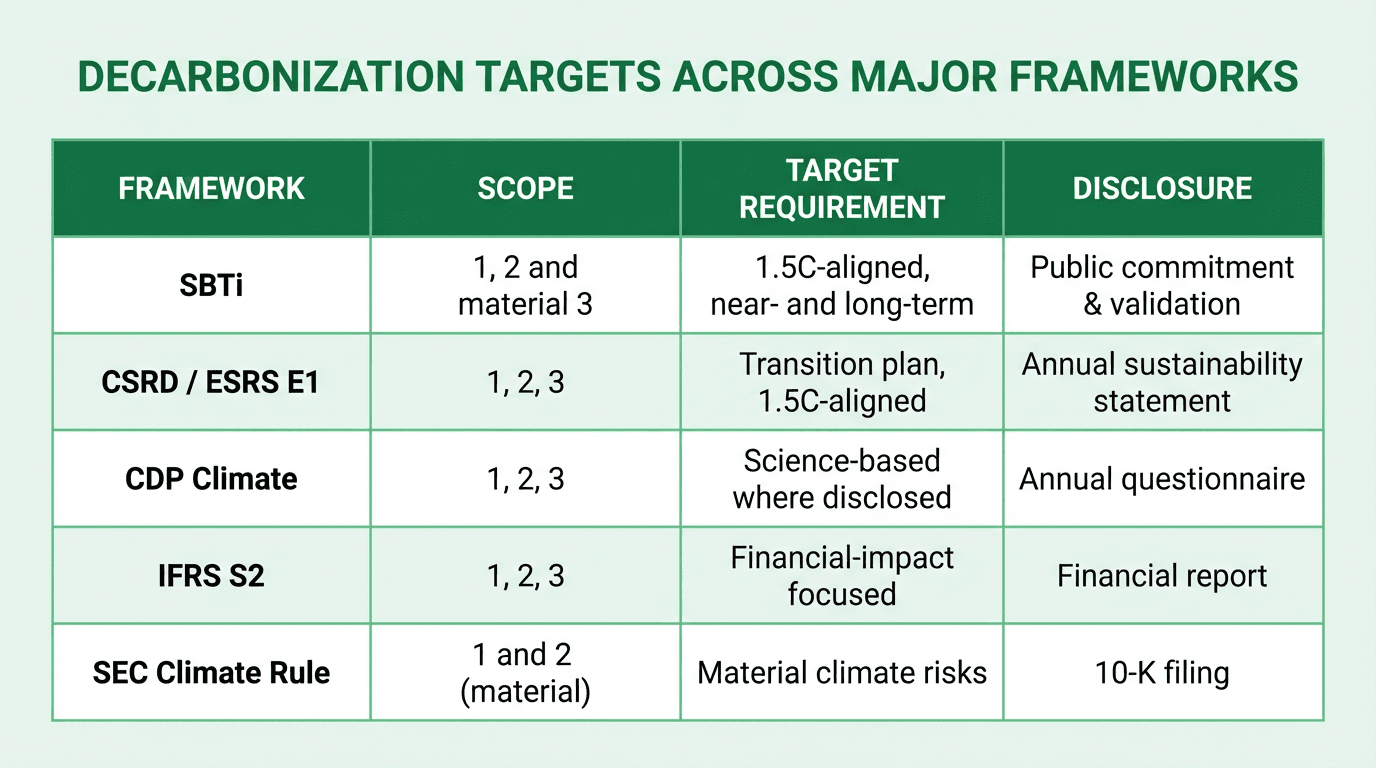

Step 6: Disclose and audit against multiple frameworks

The final step closes the loop. Every major framework now requires annual, structured disclosure with a narrative transition plan.

The five frameworks most large enterprises must now address are:

SBTi — target validation and five-yearly revalidation.

CSRD / ESRS E1 — annual sustainability statement with a 1.5°C-aligned transition plan, double materiality, and limited assurance (moving to reasonable assurance from 2028).

CDP Climate Change — annual questionnaire used by 700+ institutional investors with $130 trillion in AUM.

IFRS S2 — financial-grade climate disclosure covering Scope 1, 2, and material Scope 3, increasingly embedded in regulated financial reporting.

SEC Climate Rule — material Scope 1 and 2 climate-related risks and, for large filers, Scope 3 where financially material.

Under ESRS and IFRS S2, these disclosures must be tagged in a machine-readable taxonomy — a requirement that rules out spreadsheet-based reporting at scale. See ESG reporting and GHG Protocol reporting for deeper treatment of the reporting layer.

How Net0 supports enterprise decarbonization

Net0 provides the AI infrastructure that executes each of the six steps above as a continuous workflow rather than a sequence of manual projects. The platform's sustainability suite is one vertical within a broader AI platform for governments and enterprises, which means decarbonization operates on the same underlying data, governance, and deployment architecture as Net0's financial, operational, and public-sector AI products.

Specifically, the platform:

Automates data ingestion from 10,000+ enterprise systems — ERP, utility bills, fuel cards, travel, procurement, logistics, and direct IoT feeds.

Classifies activity data against a 50,000+ emission factor library spanning regions, fuels, grids, and years, with AI-assisted reconciliation of non-standard inputs.

Supports 30+ reporting frameworks — GHG Protocol, SBTi, CSRD/ESRS, CDP, GRI, IFRS S1/S2, SEC Climate Rule, SECR, TCFD, among others.

Simulates scenarios and MACC with financial-grade cost curves, enabling build-vs-buy, supplier substitution, and capex-phasing decisions.

Provides governance and audit trails suitable for reasonable-assurance audits, sovereign deployment, and hybrid cloud architectures for regulated and government customers.

The platform is used by 400+ entities across four continents, including Fortune 500 companies and government ministries.

Book a demo to see how Net0 can build and operate your enterprise decarbonization roadmap.

Frequently asked questions

What is the difference between decarbonization and net zero?

Decarbonization is the process of reducing greenhouse gas emissions across operations, energy use, and value chains. Net zero is a state in which residual emissions are balanced by permanent removals. Net zero is the destination; decarbonization is the continuous reduction effort that delivers the bulk of the trajectory before any removals are used.

How long does a decarbonization strategy take to build?

For a large multi-entity enterprise, building the baseline and target typically takes 6–12 months, and building the full roadmap with scenario modelling adds another 3–6 months. AI-automated platforms like Net0 compress this significantly by replacing the bulk of manual data collection and consultant reconciliation work.

Are science-based targets legally required?

SBTi validation itself is voluntary, but its content is increasingly mandated by regulators. The EU CSRD and ESRS E1 require a 1.5°C-aligned transition plan in the annual sustainability statement, and IFRS S2 requires disclosure of the climate resilience of the business strategy. SBTi is the most widely recognised way to meet these requirements.

How much does enterprise decarbonization cost?

McKinsey's 2024 cost-curve analysis finds that roughly 25% of the emissions reductions required by 2030 can be delivered by negative-cost or near-zero-cost levers. The next tranche — generally 25–50% — sits at moderate positive costs, often with 5–7 year paybacks. The final tranche of hard-to-abate emissions carries the highest cost per tonne and is where most residual removals are deployed.

Does carbon offsetting count toward a decarbonization target?

Under SBTi, offsets do not count toward near-term or long-term science-based targets. Only actual emissions reductions across Scope 1, 2, and 3 qualify. High-integrity carbon removals — the "residual" category — may be used at the net-zero stage to neutralise the portion of emissions that cannot feasibly be eliminated.

Which reporting framework should an enterprise start with?

For EU-headquartered or EU-listed firms, CSRD is non-negotiable and defines the baseline. For globally active firms, SBTi target setting and CDP disclosure are the most widely recognised benchmarks. IFRS S2 is becoming the financial-reporting standard in 30+ jurisdictions and should be treated as the integration layer for financial and sustainability data.