AI for Sustainability

Activity-Based vs Production-Based vs Spend-Based Emission Factors: The 2026 Guide

Compare activity-based, production-based and spend-based emission factors against the GHG Protocol data hierarchy, CSRD requirements, and the EU CBAM definitive regime.

Sofia Fominova

Apr 17, 2026

TL;DR: Activity-based, production-based and spend-based emission factors are the three dominant methods for translating business activity into greenhouse gas (GHG) emissions. Activity-based factors deliver the highest accuracy and audit readiness; production-based factors suit owned manufacturing; spend-based factors are a practical fallback for long-tail Scope 3 categories. Under the 2026 GHG Protocol Scope 3 revisions, the EU's Corporate Sustainability Reporting Directive (CSRD) and the Carbon Border Adjustment Mechanism (CBAM) definitive regime, activity-based data is increasingly mandatory for material emission categories.

Key Takeaways

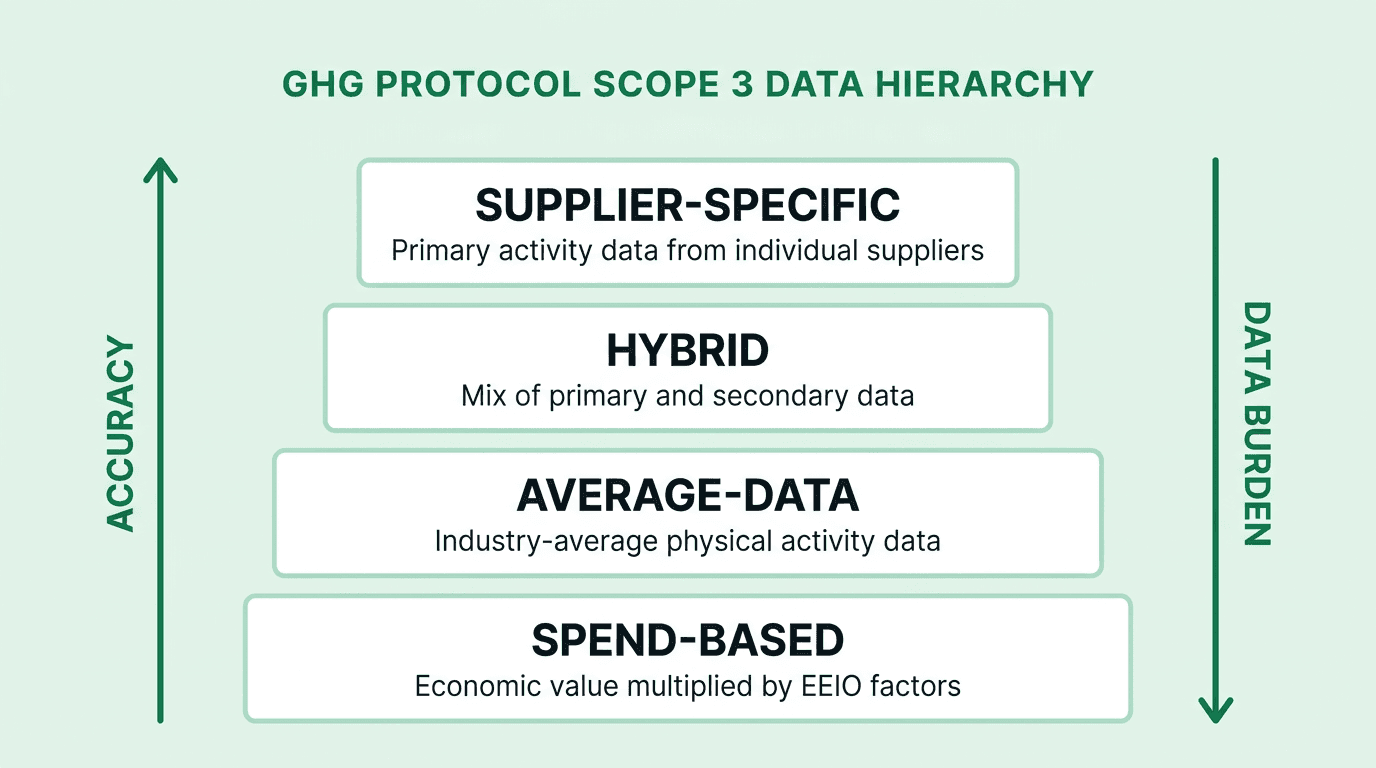

The GHG Protocol's official Scope 3 data hierarchy ranks data types from most to least accurate as: supplier-specific, hybrid, average-data, and spend-based, according to the GHG Protocol Scope 3 Standard.

Only 15% of corporates disclosing through CDP in 2024 had set a supply chain emissions target, and most still rely heavily on spend-based estimates for purchased goods and services, per the 2024 CDP Global Supply Chain Report.

The GHG Protocol Scope 3 Standard revisions progressing through 2026 will introduce mandatory data-type disaggregation and "Fully verified / Partially verified / Not verified" labelling.

The EU CBAM definitive regime, which entered force on 1 January 2026, requires importers of cement, iron, steel, aluminium, fertiliser, hydrogen and electricity to report embedded emissions using verified activity-based data, not spend-based estimates.

California SB 253 requires in-scope companies to file their first GHG disclosure by 10 August 2026, with emission source and gas-type granularity that effectively rules out pure spend-based accounting.

Introduction

Net0 is an AI infrastructure company that builds AI solutions for governments and global enterprises. Its sustainability vertical automates carbon accounting for Fortune 500 and public-sector organisations across 50,000+ emission factors and 30+ reporting frameworks. For enterprise sustainability teams preparing for CSRD assurance, IFRS S2 disclosure and SEC climate disclosure filings, the question of activity-based vs production-based vs spend-based emission factors is no longer academic. The methodology a company chooses directly determines audit outcomes, CBAM certificate liability and the credibility of its net zero targets.

This article explains each method, places them inside the current GHG Protocol data hierarchy, and sets out a decision framework for 2026 compliance. It is intended for heads of sustainability, chief financial officers, procurement directors and environmental officers at enterprises operating under multi-framework disclosure obligations.

What are emission factors?

An emission factor is a multiplier that converts a unit of activity or output into a quantity of greenhouse gas emissions, expressed in kilograms or tonnes of carbon dioxide equivalent (kgCO2e or tCO2e). Examples: 0.20707 kgCO2e per kilowatt-hour for UK grid electricity in 2024, according to the UK Department for Energy Security and Net Zero, or 2.68779 kgCO2e per litre of diesel fuel.

Emission factors sit at the core of carbon accounting. Without them, activity data (electricity consumed, miles driven, dollars spent) cannot be translated into a carbon footprint. They are published by governments, standards bodies and scientific consortia: the US EPA GHG Emission Factors Hub (updated annually, 2025 edition current), the IEA, DEFRA/DESNZ in the UK, the IPCC Emission Factor Database, and commercial databases such as ecoinvent, EXIOBASE and the EPA's USEEIO model.

The GHG Protocol data hierarchy

The GHG Protocol Corporate Value Chain (Scope 3) Standard defines four official data types, ranked by accuracy:

Supplier-specific data — primary activity data collected directly from a supplier, multiplied by a supplier-specific emission factor. Highest accuracy, strongest audit position, but the heaviest data burden.

Hybrid — a mix of supplier-specific and secondary data. Typically used where some suppliers can provide product-level footprints and others cannot.

Average-data — physical activity data (kilograms of steel, tonne-kilometres shipped) multiplied by industry-average emission factors. This is the classic "activity-based" approach as most practitioners use the term.

Spend-based — monetary expenditure multiplied by an Environmentally-Extended Input-Output (EEIO) factor, typically drawn from EXIOBASE, the EPA USEEIO model or DEFRA spend factors. Lowest data burden, but also the lowest accuracy.

This hierarchy is the frame every method discussed below must be placed inside.

Activity-based emission factors

Activity-based emission factors multiply a physical unit of activity by an emission factor expressed in the same unit: kWh of electricity × kgCO2e/kWh; litres of diesel × kgCO2e/litre; tonne-kilometres of freight × kgCO2e/tkm. They map directly to the average-data and supplier-specific tiers of the GHG Protocol hierarchy above.

When activity-based data fits. It is the default for all Scope 1 and Scope 2 emissions — direct fuel combustion, purchased electricity, refrigerants, process emissions. The GHG Protocol Corporate Standard treats anything less as non-compliant for these scopes. For Scope 3, activity-based data is expected for material categories: purchased goods and services from strategic suppliers, fuel- and energy-related activities, business travel, and use of sold products.

Strengths. Direct linkage to operational levers (a kWh avoided is a kWh avoided); audit-grade traceability; compatibility with science-based targets which require activity data for target validation; and strong alignment with CBAM's embedded-emissions requirements.

Weaknesses. Data collection burden is substantial. Supplier engagement programmes typically need 12-24 months to reach coverage above 50% of spend. Data quality varies by supplier maturity, and reconciliation between physical units and financial systems is non-trivial.

2025 enterprise example. Microsoft's 2024 Environmental Sustainability Report discloses that 96% of its Scope 3 Category 1 emissions (purchased goods and services) are now calculated using primary supplier data and hybrid methods, up from 51% three years earlier — a shift driven explicitly by CSRD preparation and SBTi validation requirements.

Production-based emission factors

Production-based emission factors measure the GHG emissions produced by a specific production process per unit of output — for example, kgCO2e per tonne of clinker for cement, or kgCO2e per tonne of crude steel. They are closely related to activity-based factors but sit at the facility or process boundary rather than the individual activity.

The term "production-based" carries a second meaning in carbon accounting: in national GHG inventories and trade policy, it refers to emissions counted where production occurs, as distinct from "consumption-based" accounting which assigns emissions to the country where goods are consumed. The EU CBAM is explicitly designed to close the production-based/consumption-based gap for carbon-intensive imports.

When production-based data fits. Organisations with direct operational control over manufacturing facilities — cement, steel, aluminium, chemicals, pulp and paper, cement and glass manufacturers — typically use production-based factors to report facility-level and corporate-level Scope 1 emissions. It is also the standard approach for calculating a product carbon footprint (PCF) under ISO 14067.

Strengths. Aligns naturally with how industrial operations are managed and measured. Enables hotspot analysis across production lines, energy efficiency benchmarking, and process-level decarbonisation investment cases.

Weaknesses. Limited by design to the production boundary. Does not capture use-phase emissions (e.g. a car's tailpipe emissions during its operational life), end-of-life emissions, or upstream supply chain emissions beyond the direct supplier. For most consumer goods, apparel, technology and services companies, production-based accounting alone materially understates the corporate footprint.

Spend-based emission factors

Spend-based emission factors multiply monetary expenditure by an emission intensity factor derived from EEIO models — typically expressed as kgCO2e per dollar (or euro, pound) of spend in a given industry category. EXIOBASE, the EPA USEEIO model and the Comprehensive Environmental Data Archive are the most common sources.

When spend-based data fits. The honest answer in 2026 is: as a temporary measure for long-tail Scope 3 categories where supplier data is genuinely unavailable, and as a screening tool to identify which categories deserve deeper activity-based investigation. It is inappropriate for material, strategic categories.

Strengths. Fast to deploy — financial data already exists in every ERP system. Covers 100% of spend by definition, which makes it useful for the initial Scope 3 screening assessment required by the GHG Protocol. Low implementation cost.

Weaknesses. EEIO factors are sector averages at a country or regional level, so they cannot distinguish between a low-carbon supplier and a high-carbon supplier within the same sector. They are also insensitive to price fluctuations — if component prices rise, spend-based emissions rise even though physical consumption is unchanged. Most critically, spend-based data provides no decarbonisation signal: it cannot reward suppliers that have actually reduced emissions, and it cannot be verified against physical inventories.

The regulatory ceiling. Under the GHG Protocol Scope 3 Standard revisions progressing in 2026, spend-based data will need to be explicitly flagged as "Not verified" in disclosures. CBAM does not accept spend-based data at all for embedded emissions calculations. California SB 253's August 2026 filing deadline requires source-level granularity that spend-based methods cannot provide.

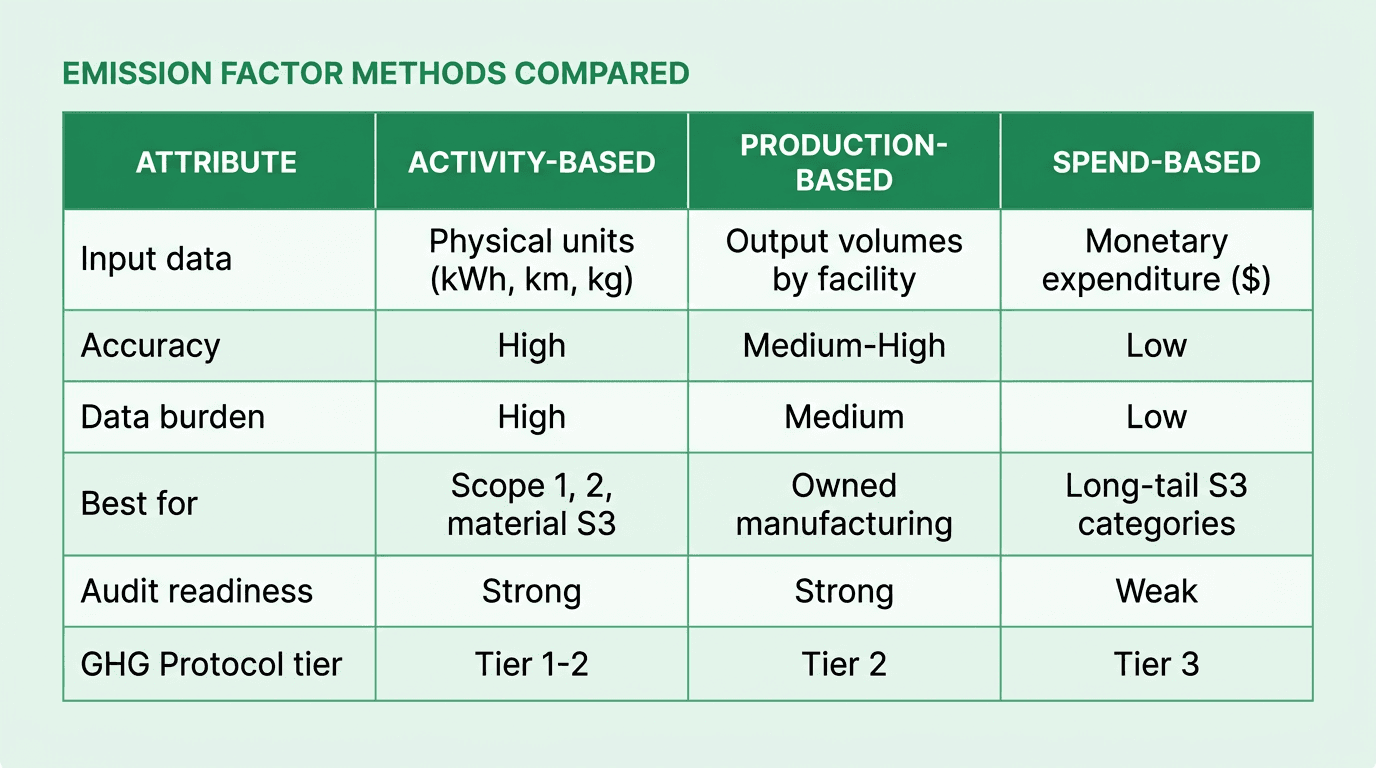

Comparing the three methods

The table above summarises the trade-offs. Three observations follow.

First, no enterprise should choose a single method. The 2024 CDP Global Supply Chain Report found that supply chain emissions average 26 times direct operational emissions, which means Scope 3 dominates almost every corporate footprint. A hybrid approach — activity-based for material categories, spend-based for long-tail — is the only realistic path.

Second, the GHG Protocol's data hierarchy is effectively a migration path. Enterprises typically begin with spend-based screening, then progressively replace high-materiality categories with average-data, then hybrid, then supplier-specific. Audit-ready disclosure under CSRD requires moving up the hierarchy over time, not choosing a single static method.

Third, method choice is now a procurement decision as much as a sustainability decision. CBAM certificate liabilities, supplier scorecards, and scope 3 reduction commitments cannot be managed with sector-average spend data.

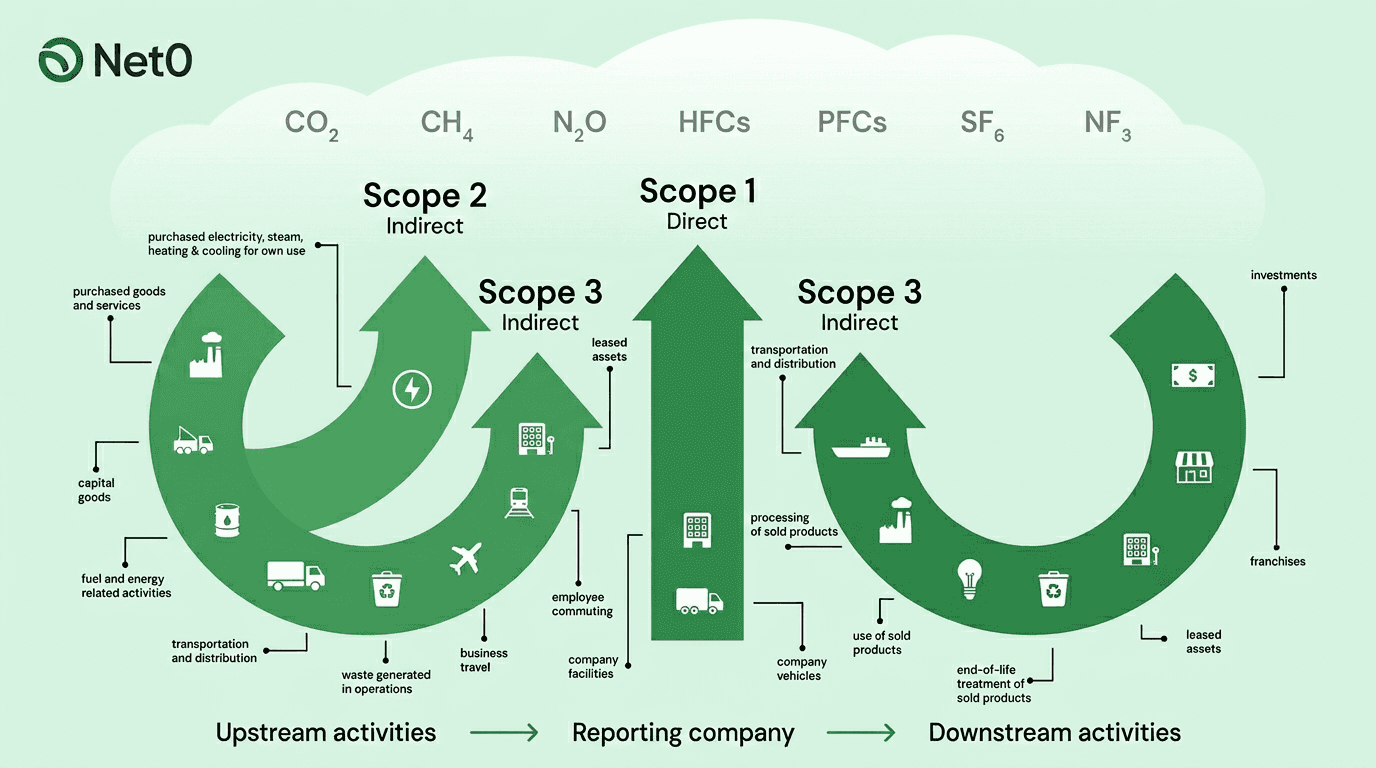

Emission factors across the scopes

Method selection varies by scope. For Scope 1, activity-based data from fuel purchases and process monitoring is the only acceptable approach. For Scope 2, activity-based electricity consumption multiplied by grid or supplier-specific emission factors (location-based or market-based, per the GHG Protocol Scope 2 Guidance) is required. For Scope 3, a hybrid approach across the 15 categories is the practical norm, with method choice driven by category materiality, data availability and regulatory sensitivity. A deep-dive on the inventory structure is available in the carbon accounting methodologies guide.

2026 regulatory context

Emission factor methodology is no longer a voluntary internal choice. Several 2026 developments have raised the stakes:

GHG Protocol Scope 3 Standard Phase 1 revisions (March 2026 update) introduce mandatory data-type disaggregation and verification labelling. Organisations will need to report, for each Scope 3 category, the proportion of data that is supplier-specific, hybrid, average-data or spend-based, and whether that data is fully verified, partially verified or not verified.

CSRD ESRS E1 (Climate Change) requires GHG Protocol methodology and is now in force for wave-one filers. The European Financial Reporting Advisory Group has signalled that spend-based data for material categories will attract qualified audit opinions.

EU CBAM definitive regime (from 1 January 2026) requires importers of covered goods to report embedded emissions using verified activity-based data from producers. Default values are available during transition but carry a higher effective carbon price.

California SB 253 (Climate Corporate Data Accountability Act) requires first GHG reports by 10 August 2026, with granular emission source and gas-type reporting.

IFRS S2 adoption across jurisdictions requires climate-related disclosures consistent with the GHG Protocol, with particular emphasis on data quality explanation.

How AI is reshaping emission factor selection

The traditional constraint on activity-based and supplier-specific data was cost: collecting, cleaning and reconciling physical activity data across thousands of suppliers and ERP line items was prohibitively manual. AI infrastructure has removed most of that constraint.

Net0 provides an AI-powered sustainability platform that connects to more than 10,000 enterprise systems — ERP, supplier portals, utility feeds, IoT sensors, travel platforms and logistics systems — and automatically classifies activity data against more than 50,000 emission factors drawn from government, commercial and supplier-specific sources. Where supplier-specific data is missing, the platform applies the appropriate GHG Protocol tier (hybrid, average-data, or spend-based) and flags the data quality transparently for audit.

The platform's AI-driven data collection capabilities materially shift the cost curve: categories that would previously have been reported using spend-based estimates can be upgraded to activity-based reporting as new data sources are onboarded, with historical restatements handled automatically. This matters for CSRD, because auditors increasingly expect to see year-on-year improvements in data quality, not static reporting at the lowest tier.

For sustainability leaders, the practical implication is simple: the methodology choice is no longer bounded by data collection capacity. It is bounded by the relevance and materiality of each category to the enterprise's decarbonisation strategy and its regulatory exposure.

Choosing a method: a decision framework

Start with a materiality screen. Use spend-based data across the full Scope 3 inventory to identify the 5-10 categories that account for ~80% of emissions. This matches the GHG Protocol's screening tier.

Upgrade material categories to activity-based data. For each material category, move to average-data or hybrid using physical activity data from ERP, freight systems, utility data and automated data collection pipelines.

Engage strategic suppliers for primary data. For the top 20-50 suppliers by emissions contribution, request product-level PCFs and supplier-specific emission factors. This is where CBAM and CSRD assurance pressure is highest.

Retain spend-based for the long tail. Smaller, non-material categories can remain on spend-based factors, but they must be disclosed transparently under the GHG Protocol's new data-type disaggregation rules.

Document and verify. Maintain an emission factor register with source, year, geographic scope and version control. Auditors will ask for it.

How Net0 supports emission factor selection

Net0 supports enterprises and public-sector organisations across all four stages of this framework. The platform ingests financial, operational and supplier data automatically, applies the correct GHG Protocol tier to each category, maintains an auditable emission factor register with over 50,000 factors, and produces disclosures aligned with CSRD, IFRS S2, CDP, SBTi, CBAM and SEC climate disclosure requirements.

Enterprise sustainability teams use Net0 to move up the GHG Protocol data hierarchy systematically — reducing spend-based exposure, accelerating supplier engagement, and building the audit evidence base needed for assured ESG reporting.

Book a demo to see how Net0's AI infrastructure handles emission factor selection, method transitions and audit documentation at enterprise scale.

Frequently Asked Questions

What are emission factors?

Emission factors are multipliers that convert units of activity (kWh, litres, tonne-kilometres, dollars of spend) into units of greenhouse gas emissions, typically expressed in kgCO2e or tCO2e. They are the core building block of carbon accounting and are published by bodies such as the US EPA, UK DESNZ, IPCC, ecoinvent and EXIOBASE.

What is the difference between activity-based and spend-based emission factors?

Activity-based factors multiply a physical unit of activity (electricity consumed, fuel burnt, goods shipped) by an emission factor in the same physical unit. Spend-based factors multiply monetary expenditure by a sector-average EEIO intensity factor. Activity-based data is more accurate and audit-ready; spend-based data is faster and cheaper but cannot distinguish between low-carbon and high-carbon suppliers.

Is production-based the same as activity-based?

Not quite. Production-based factors are a subset of activity-based factors, measured at the facility or process boundary (e.g. kgCO2e per tonne of steel produced). "Production-based" also has a separate meaning in national GHG accounting, where it refers to emissions counted at the point of production — the counterpart to consumption-based accounting. The EU CBAM bridges production- and consumption-based accounting for carbon-intensive imports.

Which emission factor method does the GHG Protocol recommend?

The GHG Protocol's Scope 3 Standard ranks methods from most to least accurate: supplier-specific, hybrid, average-data, then spend-based. It does not mandate a single method; it requires organisations to use the most accurate data reasonably available, prioritised by materiality, and to disclose the method used for each category.

Does CSRD require activity-based data?

CSRD's ESRS E1 standard requires GHG Protocol methodology and transparent disclosure of data quality. It does not prohibit spend-based data outright, but auditors are increasingly issuing qualified opinions where material Scope 3 categories rely on spend-based estimates. In practice, CSRD assurance requires activity-based data for material categories within two to three reporting cycles.

How does AI improve emission factor selection?

AI removes the data collection bottleneck that historically forced enterprises to use spend-based data as a proxy. Net0's AI infrastructure connects to more than 10,000 enterprise systems, classifies activity data against over 50,000 emission factors, and automatically applies the correct GHG Protocol tier for each category — making activity-based reporting viable at enterprise scale and keeping audit trails intact across method transitions.