AI for Sustainability

Carbon Accounting Methodologies: Spend-Based, Activity-Based, and Hybrid Approaches

A comprehensive analysis of spend-based, activity-based, and hybrid carbon accounting methodologies, with guidance on selecting the right approach for enterprise emissions measurement.

Sofia Fominova

Apr 14, 2026

TL;DR: Carbon accounting methodologies are the standardized approaches organizations use to quantify greenhouse gas emissions. The three primary methods -- spend-based, activity-based, and hybrid -- differ significantly in accuracy, complexity, and data requirements. According to a 2025 NQA analysis, spend-based estimates can deviate from actual emissions by an average of 63%, making methodology selection a critical decision for enterprises pursuing regulatory compliance and credible decarbonization targets.

Key Takeaways:

The GHG Protocol's Scope 3 Standard Development Plan (December 2024) is actively considering phasing out or limiting the spend-based method, signaling a global shift toward activity-based and hybrid approaches

Only 28% of companies currently measure their Scope 3 emissions, despite supply chain emissions being on average 26 times higher than operational emissions, according to CDP's 2024 supply chain analysis

A 2025 NQA study across 50+ verified clients found that spend-based estimates diverged from actual emissions by an average of 63%, with 77% of organizations overestimating and 23% underestimating their footprint

The hybrid methodology, combining activity-based data for material emission categories with spend-based estimates for long-tail sources, is recommended by the GHG Protocol as the most practical path to comprehensive and accurate emissions measurement

Regulatory frameworks including CSRD, ISSB (IFRS S2), and SBTi are driving enterprises toward higher-quality, activity-based data -- organizations that delay the transition face increasing compliance risk

Carbon Accounting Methodologies and the Enterprise Imperative

Net0, an AI infrastructure company that builds intelligent systems for governments and global enterprises, supports all three carbon accounting methodologies through its AI-powered sustainability platform. Carbon accounting methodologies are the standardized frameworks organizations use to measure, quantify, and report their greenhouse gas (GHG) emissions across operations and value chains.

The choice of carbon accounting methodology directly determines the accuracy of an organization's emissions data, the credibility of its sustainability disclosures, and its ability to identify reduction opportunities. According to CDP's 2024 analysis, supply chain emissions are on average 26 times higher than operational emissions, yet only 15% of companies disclosing to CDP have set a Scope 3 target. This measurement gap stems largely from methodology limitations -- organizations relying solely on spend-based estimates cannot generate the granular data needed for targeted decarbonization.

Three primary methodologies dominate corporate carbon accounting: spend-based, activity-based, and hybrid. Each represents a different trade-off between implementation complexity and measurement precision. Understanding these trade-offs is essential as regulatory frameworks -- including the EU's CSRD, IFRS S2, and the Science Based Targets initiative -- increasingly mandate higher-quality emissions data.

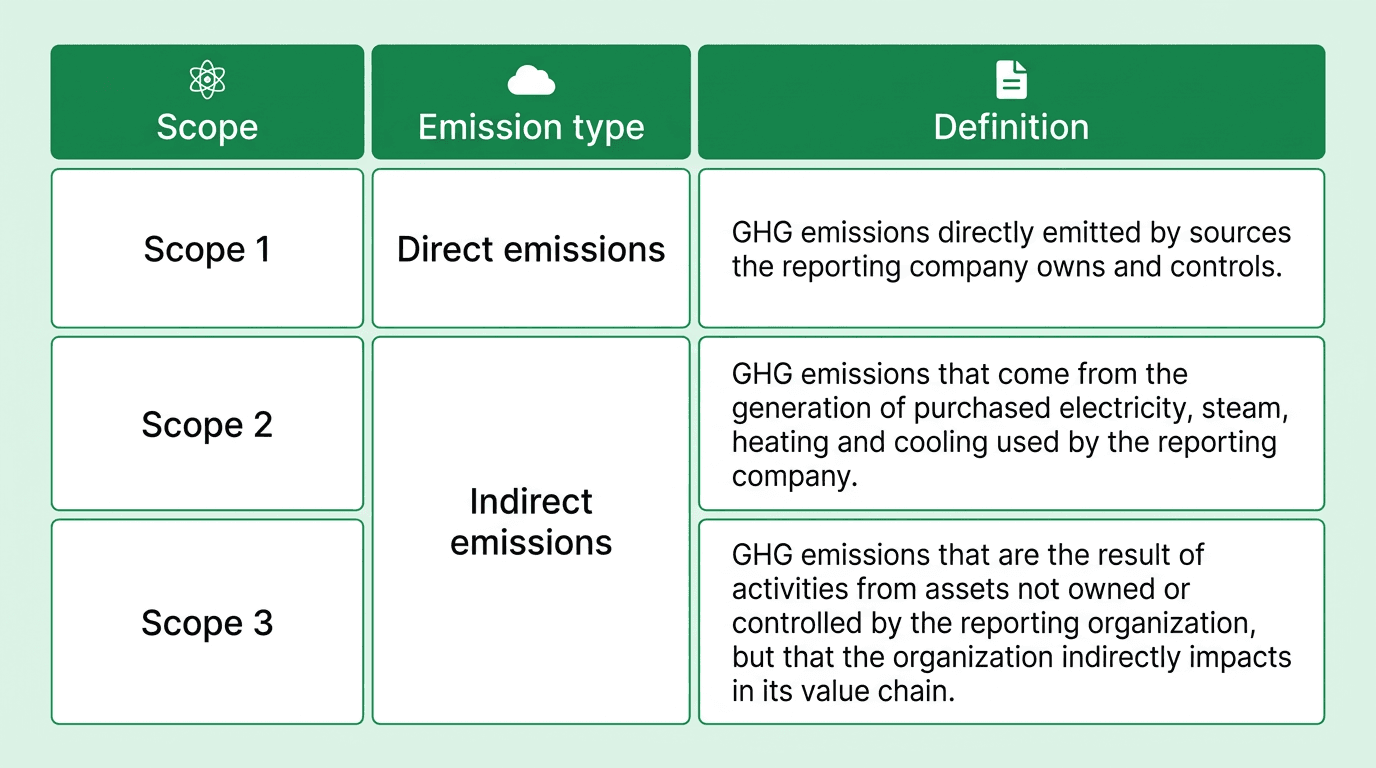

GHG Accounting Foundations and the Three Emission Scopes

GHG accounting is the systematic process of quantifying an organization's greenhouse gas emissions according to internationally recognized standards. The GHG Protocol Corporate Standard, developed by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD), provides the foundational framework used by over 90% of Fortune 500 companies that report their emissions.

The GHG Protocol categorizes emissions into three scopes:

Scope 1 covers direct emissions from owned or controlled sources -- combustion of fuels in company vehicles, on-site boilers, and industrial processes

Scope 2 covers indirect emissions from the generation of purchased electricity, steam, heating, and cooling consumed by the organization

Scope 3 encompasses all other indirect emissions across the value chain, including purchased goods and services, business travel, employee commuting, and end-of-life treatment of sold products

For a detailed breakdown of each scope, see the guide to Scope 1, 2, and 3 emissions. Scope 3 emissions typically represent 70-90% of an organization's total carbon footprint, according to CDP's data, making the choice of methodology for this scope particularly consequential. The 15 categories of Scope 3 emissions -- from purchased goods and services to investments -- each require different data inputs and calculation approaches.

Spend-Based Carbon Accounting Methodology

The spend-based methodology estimates carbon emissions by multiplying the financial value of purchased goods or services by industry-average emission factors derived from Environmentally Extended Input-Output (EEIO) models such as EXIOBASE or CEDA. This approach translates procurement spending into estimated emissions using sector-level carbon intensities per unit of currency.

How the calculation works: An organization collects financial expenditure data from invoices, procurement records, and expense reports. Each purchase is classified into an industry sector, then multiplied by the corresponding EEIO emission factor (expressed as kg CO2e per dollar or euro spent). The sum across all categories produces the organization's estimated emissions.

Strengths: The spend-based method requires only financial data that most organizations already collect. Implementation is straightforward, making it accessible to companies initiating their carbon accounting journey or those with limited sustainability resources. It provides broad coverage across all spending categories, ensuring no major emission source is entirely omitted.

Limitations: According to a 2025 NQA study examining over 50 verified clients across 28 industry sectors, spend-based estimates diverged from actual emissions by an average of 63%. Of those clients, 77% had their actual emissions overestimated (average variance of 79% above reality), while 23% had actual emissions underestimated (average variance of 623% below reality). The method is also sensitive to price fluctuations -- a company could report an apparent emissions "reduction" simply by negotiating lower prices, with no change in physical consumption or environmental impact.

Activity-Based Carbon Accounting Methodology

The activity-based methodology quantifies emissions using physical activity data -- kilowatt-hours of electricity consumed, liters of fuel burned, kilometers traveled, tonnes of materials purchased -- multiplied by technology-specific or supplier-specific emission factors. This approach establishes a direct, measurable link between operational activities and their resulting emissions.

How the calculation works: Organizations collect granular operational data across their facilities and value chain: energy meter readings, fuel purchase records, fleet telematics, production volumes, and logistics data. Each activity metric is multiplied by a corresponding emission factor sourced from databases like DEFRA, EPA, or the GHG Protocol calculation tools. The result is a precise, verifiable emissions figure for each source.

Strengths: Activity-based accounting produces significantly higher accuracy because emission factors are tied to physical units rather than financial proxies. This granularity enables organizations to identify specific emission hotspots, track reduction progress against physical baselines, and generate the data quality required by frameworks like the SBTi and CSRD. The GHG Protocol's Scope 3 Standard identifies supplier-specific and average data methods (both activity-based) as the preferred hierarchy for emissions calculation.

Limitations: Activity-based accounting demands comprehensive data collection infrastructure. According to Deloitte's 2024 Sustainability Action Report, 57% of executives identify data quality as the top challenge in ESG reporting, with 88% ranking it among their top three concerns. Obtaining activity-based data from third-party suppliers -- particularly for Scope 3 categories like purchased goods and services -- requires supplier engagement programs that take time to establish. The method's implementation cost and complexity are higher, often requiring dedicated sustainability teams, automated data collection systems, and enterprise integrations.

Hybrid Carbon Accounting Methodology

The hybrid methodology combines activity-based data for material emission categories where granular data is available with spend-based estimates for remaining categories where detailed information is not yet obtainable. The GHG Protocol recommends this approach as the most practical path to comprehensive Scope 3 measurement, and it is the methodology most widely adopted by organizations pursuing SBTi validation.

How the calculation works: Organizations prioritize activity-based data collection for their most material emission sources -- typically Scope 1 and 2 in full, plus the largest Scope 3 categories identified through an initial screening. For categories where activity data is unavailable or impractical to collect, the organization applies spend-based estimates using EEIO factors. As supplier engagement improves and data infrastructure matures, spend-based categories are progressively converted to activity-based measurement.

Strengths: The hybrid approach delivers the highest practical accuracy for most enterprises by focusing granular measurement where it matters most. It eliminates the false choice between completeness (spend-based) and precision (activity-based), allowing organizations to present a comprehensive emissions inventory while continuously improving data quality. This methodology aligns with the GHG Protocol's principle that "a combination of calculation methods, including the use of supplier-specific data where available, represents best practice."

Limitations: Managing dual data streams increases operational complexity. Organizations must maintain clear documentation of which categories use which methodology, track data quality improvements over time, and ensure consistent boundaries across reporting periods. The transition from spend-based to activity-based for individual categories requires careful baselining to avoid discontinuities in year-over-year comparisons. However, platforms with automated data collection capabilities can significantly reduce this administrative burden.

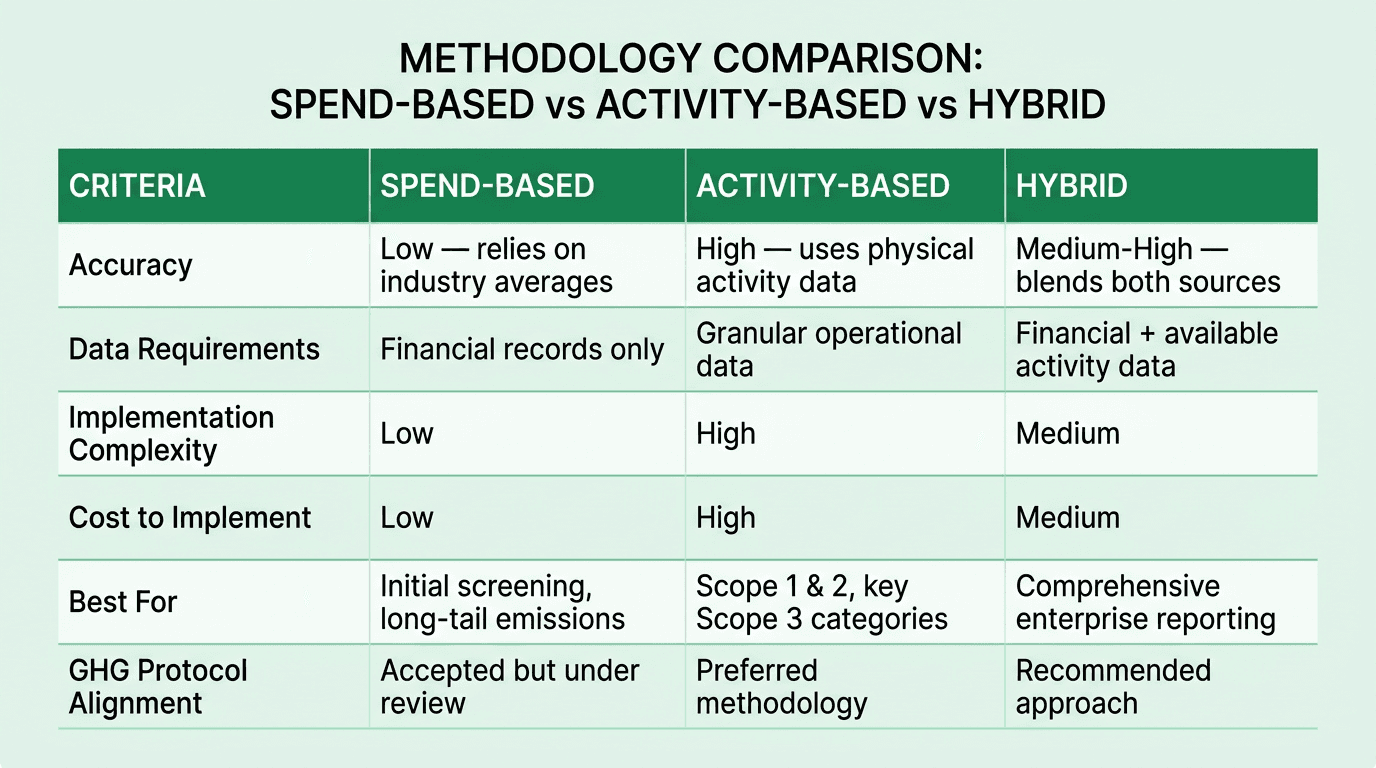

Comparative Analysis of the Three Methodologies

The choice between methodologies involves trade-offs across accuracy, complexity, cost, and regulatory alignment. The following comparison synthesizes the key differences across six evaluation criteria.

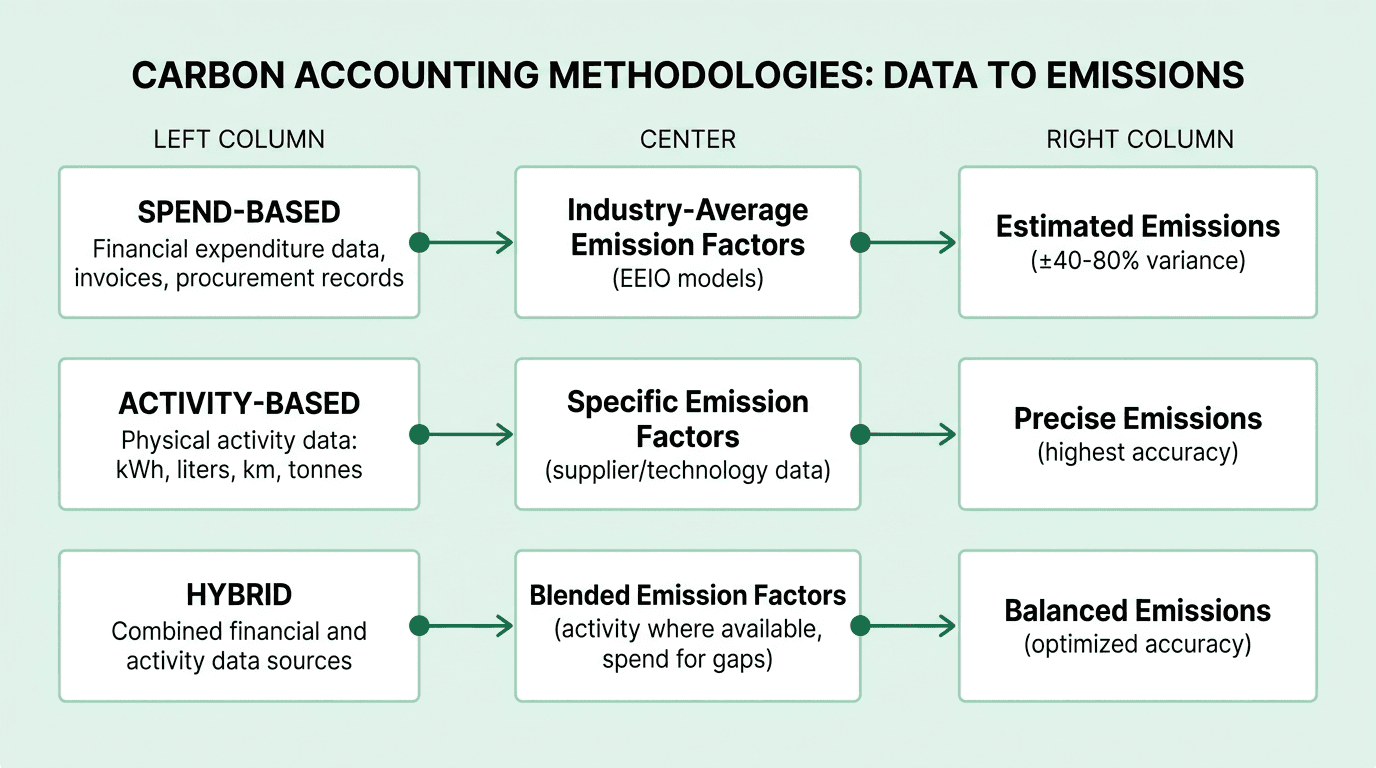

The data-to-emissions pipeline differs fundamentally across the three approaches. Spend-based accounting flows from financial records through EEIO models to estimated emissions with wide variance. Activity-based accounting flows from physical operational data through specific emission factors to precise measurements. The hybrid approach strategically combines both pipelines to optimize the accuracy-to-effort ratio.

The regulatory trajectory is clear: the GHG Protocol's Scope 3 Standard Development Plan (December 2024) explicitly notes that its Technical Working Group is considering phasing out, limiting, or removing the spend-based method in future revisions. Organizations that build their measurement infrastructure exclusively around spend-based approaches face significant transition risk as standards tighten.

Choosing the Right Carbon Accounting Methodology for Enterprise

Selecting the appropriate methodology is not a one-time decision but an evolving strategy that should match an organization's data maturity, regulatory obligations, and decarbonization ambitions. Five factors should guide the decision.

Regulatory requirements and reporting frameworks. Organizations subject to CSRD must report under the European Sustainability Reporting Standards (ESRS), which mandate the operational control approach and increasingly expect activity-based data for material categories. IFRS S2, effective for annual reporting periods from January 2025 in early-adopting jurisdictions, requires GHG emissions measurement in accordance with the GHG Protocol. Companies pursuing SBTi validation must demonstrate year-over-year emissions reductions against physical baselines -- a requirement that spend-based data alone cannot satisfy.

Data infrastructure maturity. Organizations with limited sustainability data systems may begin with spend-based accounting to establish a baseline, then systematically build activity-based capabilities for their most material categories. According to CDP's research, companies with boards that have climate oversight and competence are 5 times more likely to set Scope 3 targets, suggesting that governance maturity correlates with data infrastructure investment.

Emission materiality. Not all Scope 3 categories contribute equally. A manufacturer's purchased goods and services may represent 60-80% of total emissions, warranting activity-based measurement, while office supplies might constitute less than 1%, where spend-based estimates are sufficient. The hybrid approach formalizes this prioritization.

Supplier engagement capacity. Activity-based Scope 3 measurement depends on supplier data. According to CDP's 2024 data, companies that actively engage suppliers on climate issues are nearly 7 times more likely to set Scope 3 targets. Organizations with established supplier programs should leverage that infrastructure for activity-based data; those without may need 12-24 months to develop it.

Long-term decarbonization strategy. Spend-based methods cannot reliably track emissions reductions because changes in spending do not necessarily correspond to changes in physical emissions. Organizations with ambitious reduction targets -- particularly those aligned with the SBTi -- require activity-based measurement for their most material categories to demonstrate credible progress.

Strategic Best Practices for Methodology Transitions

The transition from spend-based to activity-based and hybrid methodologies should follow a structured maturation pathway. Leading organizations approach this as a multi-year program, not a single project.

Phase 1 -- Baseline with spend-based screening (Months 1-3). Establish a complete emissions inventory using spend-based data across all categories. This initial screening identifies the top 5-10 categories by emission magnitude, which typically account for 80-90% of total Scope 3 emissions. Prioritize these categories for activity-based conversion.

Phase 2 -- Activity-based conversion for material categories (Months 3-12). Deploy activity-based measurement for Scope 1 and 2 (which should always be activity-based) and the top Scope 3 categories. Engage key suppliers through data-sharing programs. Build integrations with enterprise systems -- ERP, energy management, fleet telematics -- to automate activity data collection.

Phase 3 -- Hybrid optimization and continuous improvement (Ongoing). Progressively convert additional Scope 3 categories from spend-based to activity-based as supplier data becomes available. Monitor the ratio of activity-based to spend-based data across the inventory and set annual improvement targets. As CDP reporting and ESG reporting requirements tighten, this continuous improvement approach ensures compliance readiness.

Organizations that follow this phased approach avoid the two most common pitfalls: the paralysis of attempting full activity-based measurement from day one, and the complacency of remaining indefinitely on spend-based estimates that cannot support credible decarbonization claims.

AI-Powered Carbon Accounting and Methodology Automation

The practical challenge of carbon accounting methodologies is not conceptual but operational: collecting data from thousands of sources, applying the correct emission factors, maintaining audit trails, and generating compliant reports across multiple frameworks. Net0, an AI infrastructure company serving governments and global enterprises, addresses this operational complexity through its AI-powered sustainability platform.

Automated data collection across all methodologies. Net0 integrates with over 10,000 enterprise systems -- ERP platforms, energy management systems, fleet telematics, procurement databases, and IoT sensors -- to automatically ingest both financial and activity-based data. This dual-stream ingestion enables organizations to operate a hybrid methodology without manual data reconciliation.

50,000+ emission factors with intelligent matching. Net0's platform maintains a library of over 50,000 emission factors spanning spend-based (EEIO), activity-based (supplier-specific, technology-specific), and region-specific factors. AI-powered matching automatically selects the most appropriate factor for each data point, progressively improving accuracy as activity-based data becomes available.

Multi-framework reporting from a single dataset. Organizations using Net0 can generate compliant disclosures across 30+ reporting frameworks -- including GHG Protocol, CSRD, CDP, GRI, ISSB, and SBTi -- from the same underlying emissions data. This eliminates the need to maintain separate calculations for each framework and ensures consistency across regulatory jurisdictions.

Methodology transition support. Net0's platform tracks the data quality composition of each emissions inventory, showing the percentage of emissions calculated using activity-based versus spend-based data. This transparency enables organizations to set measurable improvement targets and demonstrate data quality progress to auditors, investors, and regulators.

For organizations evaluating their carbon accounting methodology approach, book a demo to see how Net0 automates the data collection, calculation, and reporting workflow across all three methodologies.

Frequently Asked Questions

What is the most accurate carbon accounting methodology?

The activity-based methodology provides the highest accuracy because it uses physical activity data (kWh, liters, km) rather than financial proxies. A 2025 NQA study found spend-based estimates deviate from actual emissions by an average of 63%. However, the GHG Protocol recommends the hybrid approach as the most practical balance of accuracy and completeness for most organizations.

Is the spend-based carbon accounting method being phased out?

The GHG Protocol's Scope 3 Standard Development Plan (December 2024) indicates that the Technical Working Group is considering phasing out, limiting, or removing the spend-based method. While no final decision has been made, the direction signals that organizations should plan for a transition toward activity-based and hybrid methodologies.

Which carbon accounting methodology does the GHG Protocol recommend?

The GHG Protocol recommends a hybrid approach that combines activity-based data where available with spend-based estimates for remaining categories. The Scope 3 Calculation Guidance establishes a data quality hierarchy: supplier-specific data is preferred, followed by average data methods, then spend-based methods as a last resort.

How do CSRD and IFRS S2 affect methodology selection?

CSRD requires reporting under the European Sustainability Reporting Standards (ESRS), which expect activity-based data for material emission categories. IFRS S2 mandates GHG emissions measurement in accordance with the GHG Protocol. Both frameworks are driving organizations toward higher-quality data collection, making exclusive reliance on spend-based methods increasingly inadequate for compliance.

What is the difference between activity-based and spend-based emission factors?

Spend-based emission factors express average GHG emissions per unit of financial expenditure (e.g., kg CO2e per dollar) and are derived from EEIO models using sector-wide averages. Activity-based emission factors express GHG emissions per unit of physical activity (e.g., kg CO2e per kWh or per km) and are derived from technology-specific or supplier-specific data. Activity-based factors provide a direct link between operational decisions and emissions impact.

How long does it take to transition from spend-based to hybrid carbon accounting?

Most enterprises can establish a baseline spend-based inventory within 1-3 months, then convert their top emission categories to activity-based measurement within 3-12 months. Full hybrid optimization -- where the majority of material emissions are activity-based -- typically takes 12-24 months, depending on supply chain complexity and supplier engagement maturity.

Can AI improve the accuracy of carbon accounting methodologies?

AI significantly improves accuracy by automating data collection from enterprise systems, intelligently matching emission factors to activity data, identifying data anomalies, and maintaining consistency across reporting periods. Net0's platform, for example, integrates with over 10,000 systems and maintains 50,000+ emission factors to optimize methodology selection at the individual data-point level.