AI for Sustainability

What Are Scope 1, 2, and 3 Emissions? A 2026 Guide

A 2026 guide to Scope 1, 2, and 3 greenhouse gas emissions under the GHG Protocol — definitions, the 15 Scope 3 categories, and how AI enables accurate measurement.

Sofia Fominova

Apr 19, 2026

TL;DR: Scope 1, 2, and 3 emissions are the three categories of greenhouse gas emissions defined by the GHG Protocol — direct emissions from owned sources (Scope 1), indirect emissions from purchased energy (Scope 2), and all other value-chain emissions both upstream and downstream (Scope 3). In 2026, disclosing all three scopes is no longer optional for most large companies: the EU's CSRD, the SBTi Net-Zero Standard, IFRS S2, CDP, and California's SB 253 all now require it.

Key Takeaways:

Scope 3 accounts for roughly 75% of the average company's total emissions, and as much as 90% in sectors such as financial services, retail, and consumer goods, according to CDP's 2024 Global Supply Chain Report.

Approximately 50,000 companies now fall within the scope of the EU's Corporate Sustainability Reporting Directive (CSRD), which mandates full Scope 1, 2, and 3 disclosure under ESRS E1, according to the European Commission's 2024 impact assessment.

IFRS S2 (issued by the ISSB in 2023) requires Scope 1, 2, and 3 disclosure and has now been adopted by 21 jurisdictions including the UK, Canada, Brazil, Japan, and Australia, per the IFRS Foundation's 2025 adoption status report.

California's SB 253 requires companies with over $1 billion in revenue doing business in California to report Scope 1 and 2 emissions from FY2025 data (due 2026) and Scope 3 from FY2026 data (due 2027).

Only 41% of companies disclosing to CDP in 2024 reported any Scope 3 data, and most reported fewer than half of the 15 categories — a gap that AI-powered data platforms are now being deployed to close.

Introduction

Net0 is an AI infrastructure company that builds AI solutions for governments and global enterprises. One of its core verticals, AI for Sustainability, helps Fortune 500 companies and government agencies measure, verify, and report scope 1, 2, and 3 emissions at enterprise scale. This guide explains what each scope covers, how the 15 Scope 3 categories work, which regulations now require full-scope reporting in 2026, and why traditional spreadsheet-based carbon accounting has become unfit for purpose.

The framework comes from the Greenhouse Gas Protocol Corporate Standard, co-developed by the World Resources Institute and the World Business Council for Sustainable Development. It is the global reference standard underpinning virtually every major sustainability regulation, reporting framework, and net-zero target in use today — including the Science Based Targets initiative, CDP, IFRS S2, the European Sustainability Reporting Standards, and the Global Reporting Initiative.

What are Scope 1, 2, and 3 emissions?

Under the GHG Protocol, a company's greenhouse gas inventory is split into three scopes based on two questions: who owns or controls the emission source, and where in the value chain the emissions occur.

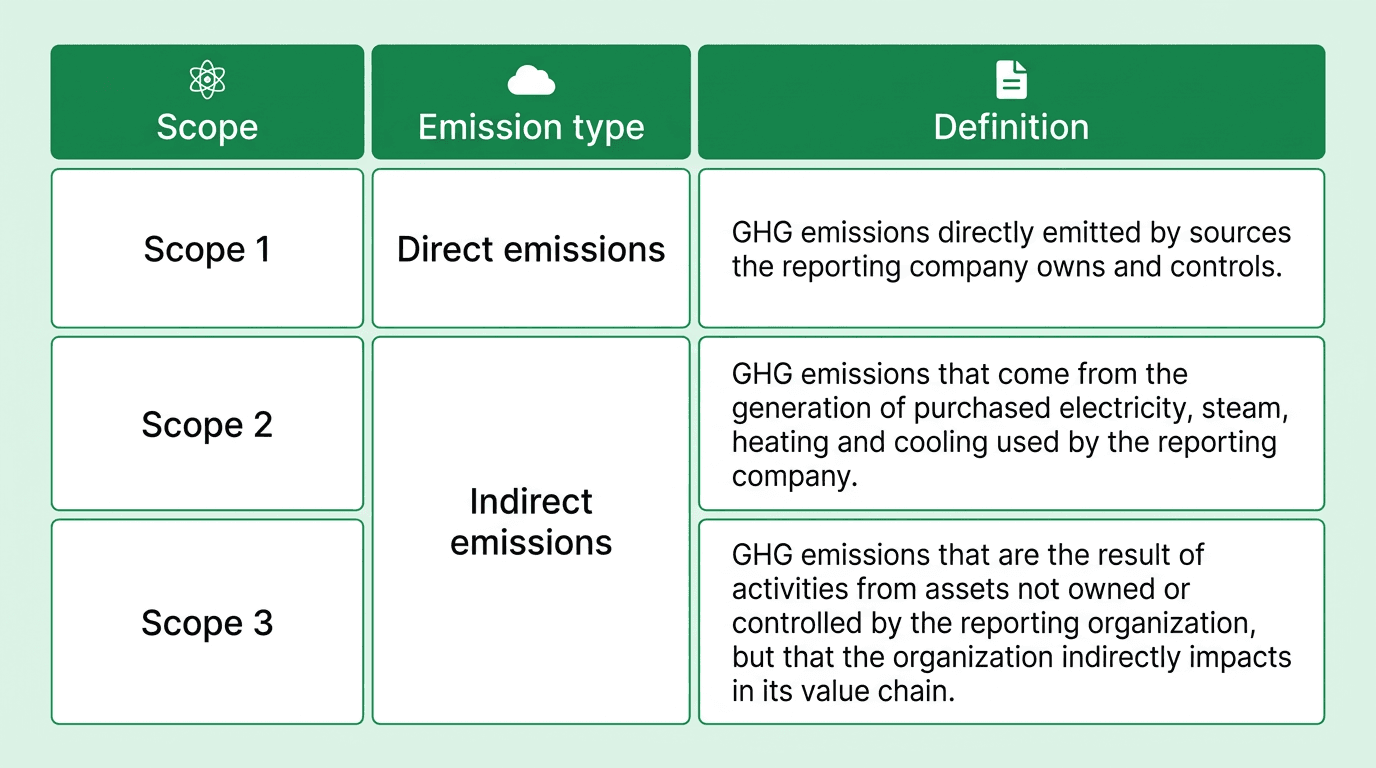

Scope 1 — direct emissions from sources owned or controlled by the reporting entity.

Scope 2 — indirect emissions from the generation of purchased electricity, steam, heat, and cooling consumed by the reporting entity.

Scope 3 — all other indirect emissions in the value chain, both upstream (before the product reaches the company) and downstream (after it leaves).

One company's Scope 3 emissions are another company's Scope 1 and 2 emissions. The three-scope structure exists to allocate responsibility without double-counting across the global economy.

Direct vs. indirect emissions

Direct emissions come from sources the reporting entity owns or controls — a corporate fleet, an onsite boiler, a manufacturing furnace. Indirect emissions are caused by the entity's activities but occur at sources owned or controlled by someone else — the power plant generating the electricity a company buys, the supplier producing its raw materials, or the end customer using its products.

The distinction matters because strategies differ. Direct emissions respond to capital investment — electrifying vehicles, replacing gas boilers, installing onsite abatement. Indirect emissions respond to procurement, contract design, and supplier engagement. In most sectors, indirect emissions are larger and harder to influence, which is why carbon accounting methodologies and value-chain data quality have become the defining technical challenges of corporate climate programmes.

Scope 1: direct emissions from owned or controlled sources

Scope 1 covers emissions from sources the company owns or operates. The GHG Protocol groups these into four sub-categories:

Stationary combustion — boilers, furnaces, turbines, backup generators, and other fixed fuel-burning equipment.

Mobile combustion — company-owned cars, trucks, ships, aircraft, and heavy equipment running on fossil fuels.

Process emissions — greenhouse gases released by industrial chemical processes such as cement calcination, steel production, or ammonia synthesis, independent of energy use.

Fugitive emissions — unintentional leaks, most commonly refrigerants (HFCs) from HVAC and cold-chain systems and methane from oil and gas infrastructure.

In 2026, two Scope 1 sources have become particularly scrutinised. Fugitive refrigerant emissions are now explicitly required disclosures under ESRS E1-6 in the EU, as HFCs have global warming potentials hundreds to thousands of times that of CO2. And corporate fleet emissions are under pressure as the EU's CO2 standards for cars and vans tighten toward the 2035 zero-emission new-vehicle target, and as California's Advanced Clean Fleets rule phases in zero-emission requirements for medium- and heavy-duty trucks.

Scope 2: indirect emissions from purchased energy

Scope 2 covers emissions from the generation of electricity, steam, heating, and cooling that the company purchases and consumes. Although these emissions physically occur at the supplier's power plant or utility, the GHG Protocol attributes them to the buyer because the demand for energy drives the generation.

The GHG Protocol Scope 2 Guidance requires companies to report under two parallel methods:

Location-based — uses the average emissions intensity of the grid where consumption physically occurs. This reflects the actual physical impact of electricity use.

Market-based — uses the emissions factor associated with specific contractual instruments such as Renewable Energy Certificates (RECs), Guarantees of Origin (GOs), and Power Purchase Agreements (PPAs). This reflects the company's procurement choices.

Dual reporting is now the default expectation across CDP, CSRD, and IFRS S2. For large enterprises, the market-based figure is increasingly where abatement happens: signing renewable PPAs, investing in onsite solar, and matching consumption to clean generation hour-by-hour. The most ambitious buyers — Google, Microsoft, and a growing number of Fortune 500 companies — have committed to 24/7 carbon-free energy, going beyond annual REC matching to hourly clean-energy accounting.

Scope 1 and Scope 2 are generally well understood, auditable, and now a mandatory part of reporting for almost every large or listed company globally. The difficulty — and the strategic opportunity — lies in Scope 3.

Scope 3: all other indirect emissions in the value chain

Scope 3 emissions, often called value-chain emissions, cover all indirect greenhouse gas emissions that occur in the company's upstream and downstream activities but are not included in Scope 2. They are the GHG Protocol's catch-all for everything else a company is responsible for but does not directly own or control.

Scope 3 typically dominates a corporate carbon footprint. CDP data shows that Scope 3 represents roughly 75% of total emissions for the average disclosing company, and in sectors such as financial services, apparel, and fast-moving consumer goods it often exceeds 90%. For asset managers and banks, category 15 (financed emissions) alone can be several hundred times the size of their operational footprint.

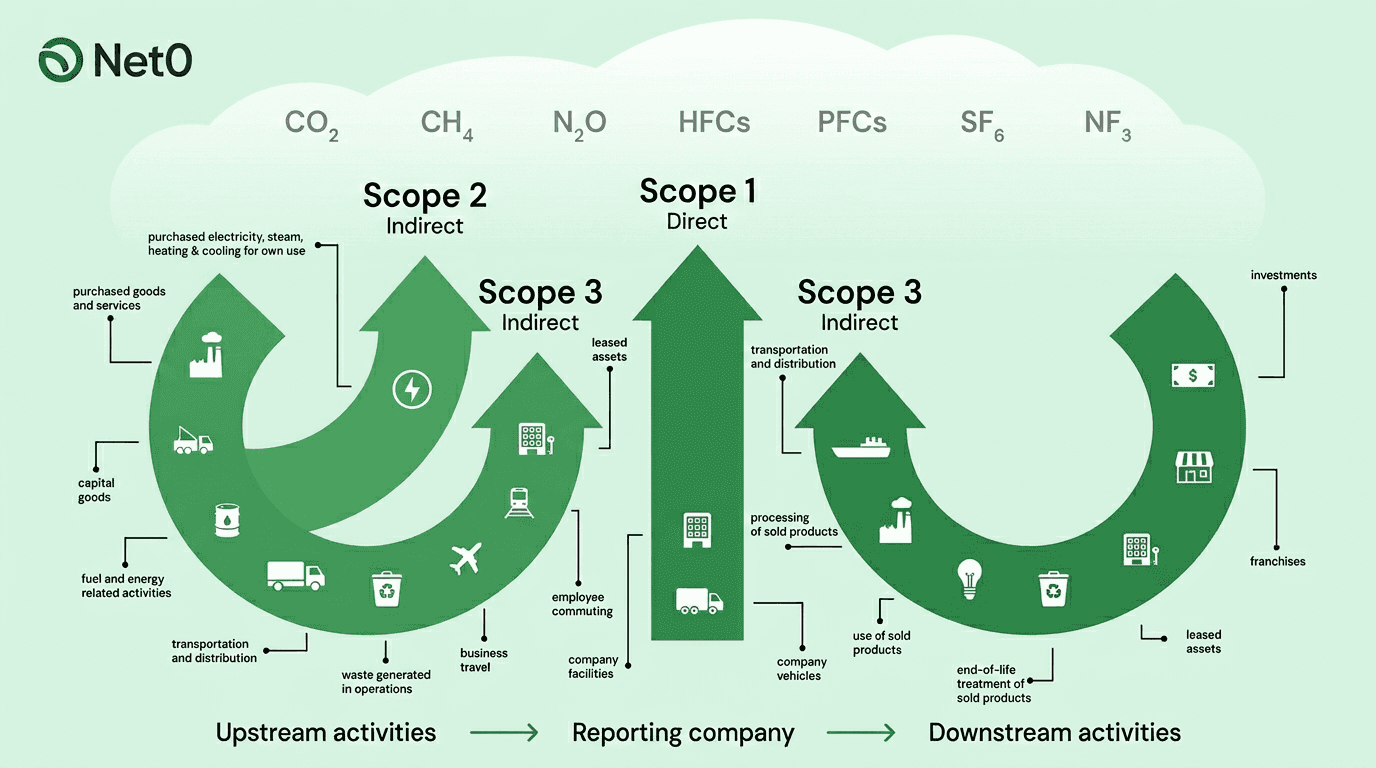

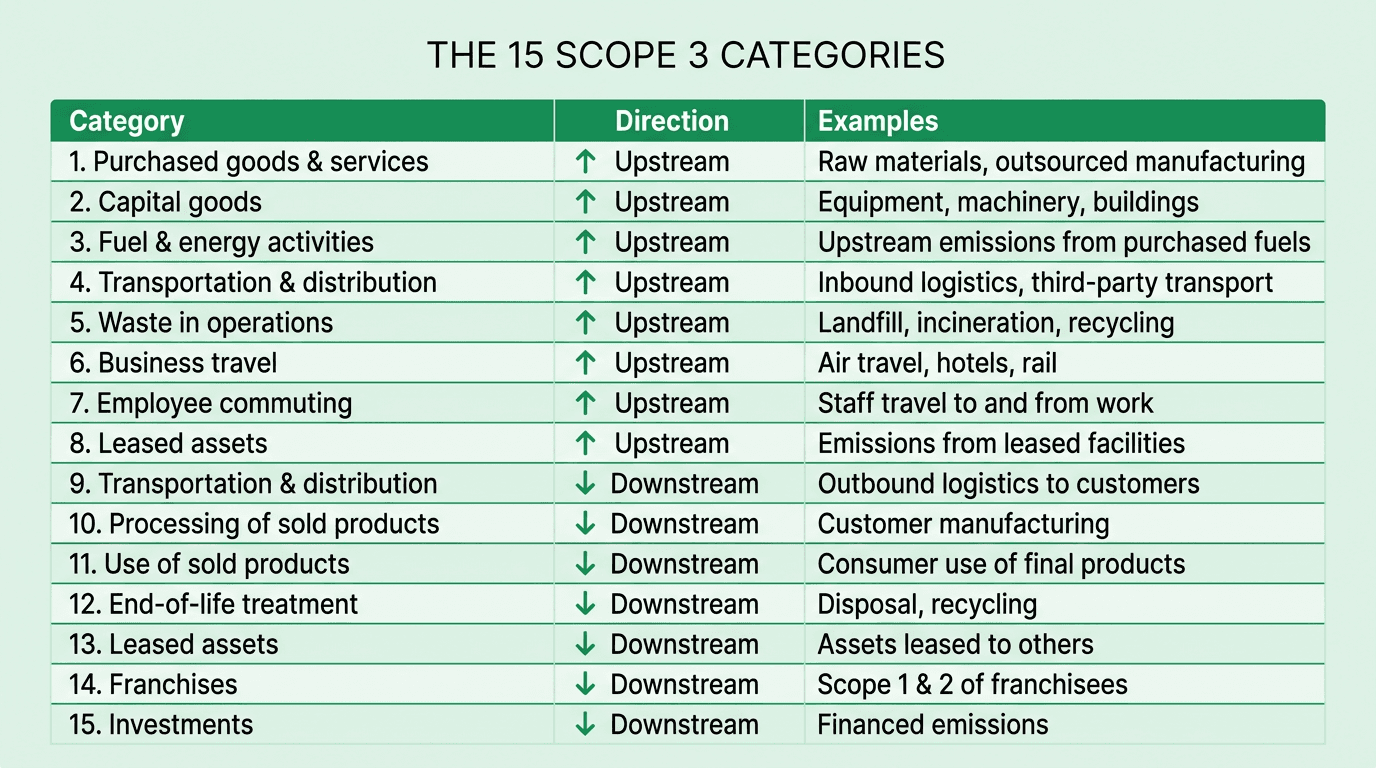

To prevent double counting, the GHG Protocol splits Scope 3 into 15 mutually exclusive categories — 8 upstream and 7 downstream. Each category has its own scope, calculation guidance, and data requirements.

The 15 categories of Scope 3 emissions

Upstream emissions originate before the product reaches the reporting company's operations — in the extraction, production, and delivery of goods, services, and capital inputs.

Upstream categories (8):

Purchased goods and services — cradle-to-gate emissions from everything the company buys, from raw materials to professional services. For most manufacturers and retailers this is the single largest Scope 3 category.

Capital goods — emissions embodied in long-lived assets such as buildings, machinery, vehicles, and IT infrastructure, calculated on a cradle-to-gate basis.

Fuel- and energy-related activities — upstream emissions from the fuels and electricity the company uses that are not already counted in Scope 1 or 2 (e.g., the emissions from extracting and refining the diesel used in company vehicles, and transmission and distribution losses for purchased electricity).

Upstream transportation and distribution — third-party logistics moving purchased goods and services to the company, plus any transport services the company pays for.

Waste generated in operations — disposal and treatment of waste produced at the company's sites, including landfill, incineration, composting, and wastewater treatment.

Business travel — employee travel on third-party carriers: flights, trains, taxis, hotel stays.

Employee commuting — home-to-workplace travel, plus increasingly teleworking emissions for hybrid workforces.

Upstream leased assets — operation of assets the company leases in, where these emissions are not already captured in Scope 1 or 2.

Downstream emissions occur after the product leaves the reporting company's control, and are driven primarily by product design, customer behaviour, and financial exposure.

Downstream categories (7):

Downstream transportation and distribution — movement of sold products through third-party logistics, retail, and storage to the end consumer.

Processing of sold products — emissions from customers' processing of intermediate products the company sells (for example, a steel producer reporting a portion of a car manufacturer's emissions).

Use of sold products — energy or fuel consumed during the customer's use of the product over its useful life. For automakers, oil and gas companies, and appliance manufacturers, this is typically the largest single category in the entire inventory.

End-of-life treatment of sold products — waste disposal and treatment once the customer is finished with the product.

Downstream leased assets — operation of assets the company owns but leases out to others.

Franchises — operation of franchises not owned or controlled by the franchisor.

Investments — also called financed emissions, covering equity investments, debt investments, project finance, and managed investments. This is the defining Scope 3 category for banks, asset managers, insurers, and private equity firms, and is typically calculated using the PCAF methodology.

Not every category is relevant to every company — the GHG Protocol allows companies to screen out categories that are immaterial or for which they have no activities — but each exclusion must be explicitly declared and justified. Several Scope 3 myths persist about which categories are and are not mandatory, and regulators have become increasingly strict about unjustified omissions.

Why Scope 1, 2, and 3 emissions matter in 2026

The 2024 regulatory landscape was transitional. 2026 is where full-scope reporting becomes the default expectation across the world's three largest economic blocs.

CSRD and ESRS E1 — Europe

The EU's Corporate Sustainability Reporting Directive, operationalised through the European Sustainability Reporting Standards, requires full Scope 1, 2, and 3 disclosure under ESRS E1 (Climate Change). Following the EU's 2025 Omnibus I simplification package, the directive now applies to approximately 50,000 in-scope companies — including non-EU parent groups with significant EU turnover. Reports must include a transition plan aligned with limiting warming to 1.5°C and are subject to limited assurance in 2026 and reasonable assurance from 2028.

SBTi Net-Zero Standard

The Science Based Targets initiative's Corporate Net-Zero Standard requires companies to set both near-term and long-term targets covering Scope 1, 2, and relevant Scope 3 emissions, where Scope 3 is considered relevant if it represents at least 40% of the company's total footprint. Version 2 of the standard, published for consultation in 2024 and finalised in 2025, tightens the rules around residual emissions, beyond value chain mitigation, and sector-specific pathways. More than 5,000 companies have now had targets validated by SBTi.

IFRS S2 — Global capital markets

IFRS S2 Climate-related Disclosures, issued by the ISSB in 2023, requires disclosure of Scope 1, 2, and Scope 3 emissions (with a one-year transition relief for Scope 3). By the end of 2025, 21 jurisdictions — including the UK, Canada, Brazil, Japan, Singapore, Malaysia, and Australia — had adopted or committed to adopt ISSB standards, making IFRS S2 the closest thing to a global baseline for climate disclosure.

SEC and US state law

At the federal level in the United States, the SEC's Climate-Related Disclosures rule dropped mandatory Scope 3 disclosure in its final 2024 version and was subsequently subject to litigation. US state law, however, has moved faster. California's SB 253 (Climate Corporate Data Accountability Act) requires companies with annual revenues above $1 billion that do business in California to disclose Scope 1 and 2 emissions starting in 2026 (for FY2025) and Scope 3 emissions starting in 2027 (for FY2026). An estimated 5,300+ companies are in scope.

CDP

CDP, through which over 23,000 organisations disclosed environmental data in 2025, has aligned its Climate Change questionnaire with IFRS S2 and ESRS E1. Scope 3 disclosure across all relevant categories is now a requirement for the leadership-band A-list score.

Taken together, these five frameworks mean that for any enterprise operating in Europe, listed on a major exchange, or doing business in California, full Scope 1, 2, and 3 disclosure is now a compliance baseline, not a stretch goal.

The Scope 3 measurement problem

The gap between regulatory expectation and reporting reality is wide. CDP's 2024 analysis found that only 41% of disclosing companies reported any Scope 3 emissions, and of those, most covered fewer than half of the 15 categories. The reasons are structural:

Data fragmentation — Scope 3 data lives in procurement systems, supplier surveys, logistics providers, travel agencies, product lifecycle databases, and financial portfolios. A single category can require pulling data from dozens of systems.

Supplier response rates — primary supplier data is the gold standard, but CDP's 2024 Supply Chain Report shows that only around 42% of requested suppliers disclose through CDP when asked, and response quality varies enormously.

Emission factor choice — spend-based, average-data, hybrid, and supplier-specific methods produce very different results for the same activity. The methodological distinction between activity-based, production-based, and spend-based emission factors is central to data quality.

Double counting — without clear boundary definitions, emissions can end up counted in multiple categories or across multiple reporting entities, undermining target credibility.

Audit and assurance pressure — as assurance requirements tighten under CSRD and IFRS S2, every number must be traceable back to source evidence.

Spreadsheet-based carbon accounting collapses under these conditions. A mid-sized multinational can have tens of thousands of suppliers and hundreds of thousands of transactions feeding into a single reporting cycle — and that cycle now repeats annually, with quarterly stakeholder updates and monthly internal dashboards. The data volumes and validation requirements are fundamentally an enterprise data problem, not an accounting one.

How Net0 measures Scope 1, 2, and 3 emissions

Net0 is an AI infrastructure company serving over 400 entities across four continents, including Fortune 500 enterprises and national governments. Its AI-first sustainability platform is built specifically for the data complexity of full-scope emissions reporting at enterprise scale.

Automated data collection from 10,000+ enterprise systems — direct connectors to ERP systems (SAP, Oracle, Microsoft Dynamics), procurement platforms (Coupa, Ariba), travel and expense systems (Concur, Navan), logistics providers, utility APIs, and IoT metering infrastructure. Scope 1 and 2 data is sourced as close to the meter as possible; Scope 3 activity data is extracted from transactional and operational systems rather than reconstructed from invoices.

50,000+ emission factors across jurisdictions, methodologies, and GHG Protocol categories, kept current with IEA, EPA, DEFRA, EXIOBASE, and national inventory updates. AI-assisted classification automatically maps procurement line items, expense records, and product SKUs to the correct factor.

AI-powered supplier engagement — large-language-model workflows draft and manage supplier outreach, parse responses at scale, validate incoming primary data, and flag outliers for review. This converts supplier engagement from a seasonal campaign into a continuous data operation.

30+ reporting frameworks out of the box — GHG Protocol, CSRD/ESRS, IFRS S1 and S2, CDP, GRI, SBTi, TCFD, SECR, California SB 253/261, and more. The same underlying activity data is mapped once and used across every framework.

Scenario simulation and Marginal Abatement Cost Curves — the platform supports decarbonization planning, letting teams model Scope 1, 2, and 3 reduction pathways against cost, risk, and regulatory targets.

Audit trail and explainability — every emissions number is traceable to its source record, emission factor, and calculation method, designed for reasonable assurance under CSRD and equivalent regimes.

Net0 also operates across adjacent verticals — Government AI, Business AI Solutions, and core AI infrastructure — meaning sustainability deployments benefit from the same AI architecture that powers national-scale government platforms. Read more about the company and its founders.

Book a demo

Net0 provides the AI infrastructure enterprises and governments need to measure, verify, and reduce Scope 1, 2, and 3 emissions at scale. Book a demo to see how the platform replaces spreadsheet-based carbon accounting with an AI-first data and reporting layer built for 2026 compliance.

Frequently Asked Questions

What are Scope 1, 2, and 3 emissions?

Scope 1, 2, and 3 emissions are the three categories of greenhouse gas emissions defined by the GHG Protocol. Scope 1 covers direct emissions from sources a company owns or controls. Scope 2 covers indirect emissions from purchased electricity, steam, heat, and cooling. Scope 3 covers all other value-chain emissions, both upstream (such as purchased goods and services) and downstream (such as use of sold products and financed emissions).

What is the difference between direct and indirect emissions?

Direct emissions occur at sources the reporting company owns or controls, such as onsite boilers or company vehicles. Indirect emissions are caused by the company's activities but occur at sources owned by others — for example, the power plant producing purchased electricity (Scope 2) or a supplier manufacturing raw materials (Scope 3). The distinction drives different abatement strategies.

Are Scope 3 emissions mandatory to report in 2026?

For most large enterprises, yes. Scope 3 is mandatory under the EU CSRD/ESRS E1 for in-scope companies, under IFRS S2 (after a one-year transition) in jurisdictions that have adopted ISSB standards, for SBTi net-zero targets where Scope 3 exceeds 40% of the footprint, and under California's SB 253 for companies above $1 billion in revenue starting with FY2026 data.

What are the 15 categories of Scope 3 emissions?

The GHG Protocol defines 8 upstream categories (purchased goods and services; capital goods; fuel- and energy-related activities; upstream transportation and distribution; waste generated in operations; business travel; employee commuting; upstream leased assets) and 7 downstream categories (downstream transportation and distribution; processing of sold products; use of sold products; end-of-life treatment of sold products; downstream leased assets; franchises; investments).

What are Scope 4 emissions?

Scope 4, or avoided emissions, are reductions that occur outside a product's life cycle as a result of using that product — for example, emissions avoided when an energy-efficient technology replaces a more polluting alternative. Scope 4 is not part of the GHG Protocol Corporate Standard and is typically reported separately from the formal emissions inventory, often within the product carbon footprint context.

How can AI improve Scope 3 data quality?

AI systems improve Scope 3 data quality in four main ways: automating the extraction of activity data from ERP, procurement, travel, and logistics systems; classifying transactions against the correct emission factors at scale; managing supplier engagement and response validation through language-model workflows; and detecting anomalies, gaps, and double counting in the resulting inventory. These capabilities replace the manual, spreadsheet-based processes that cause most Scope 3 gaps today.

Which frameworks require Scope 1, 2, and 3 reporting?

The primary frameworks requiring Scope 1, 2, and 3 disclosure are the EU's CSRD (via ESRS E1), IFRS S2 (ISSB), the Science Based Targets initiative's Corporate Net-Zero Standard, CDP Climate Change, the GRI 305 topic standard, California SB 253, and sector-specific regimes such as PCAF for financed emissions. All share the GHG Protocol Corporate Standard as their underlying methodology.