AI for Sustainability

Scope 3 Emissions: Categories, Calculation Methods, and AI-Powered Reduction Strategies

Scope 3 emissions account for approximately 75% of total corporate greenhouse gas output. This guide covers all 15 GHG Protocol categories, three calculation methods, regulatory requirements under CSRD and SBTi, and how AI-powered platforms accelerate measurement and reduction across the value chain.

Sofia Fominova

Apr 16, 2026

TL;DR: Scope 3 emissions are the indirect greenhouse gas emissions that occur across a company's entire value chain -- both upstream and downstream -- and account for approximately 75% of total corporate emissions, according to the University of Chicago's 2025 Sustainability Dialogue. Net0, an AI infrastructure company that builds intelligent systems for governments and global enterprises, automates Scope 3 measurement, reporting, and reduction through its AI-powered sustainability platform.

Key Takeaways:

Scope 3 emissions represent approximately 75% of a company's total greenhouse gas inventory and are on average 11 times higher than direct operational emissions (University of Chicago Sustainability Dialogue, 2025; Thomson Reuters Institute, 2024)

The GHG Protocol defines 15 categories of Scope 3 emissions -- 8 upstream and 7 downstream -- covering everything from purchased goods to end-of-life treatment of sold products

Only 40% of companies currently report Scope 3 emissions despite their outsized climate impact (University of Chicago, 2025)

The EU's Corporate Sustainability Reporting Directive (CSRD) makes Scope 3 disclosure mandatory for in-scope companies under ESRS E1, while the SBTi requires Scope 3 targets when these emissions exceed 40% of total emissions

AI-powered platforms reduce the time and cost of Scope 3 accounting by automating data collection across 10,000+ enterprise systems and applying 50,000+ emission factors

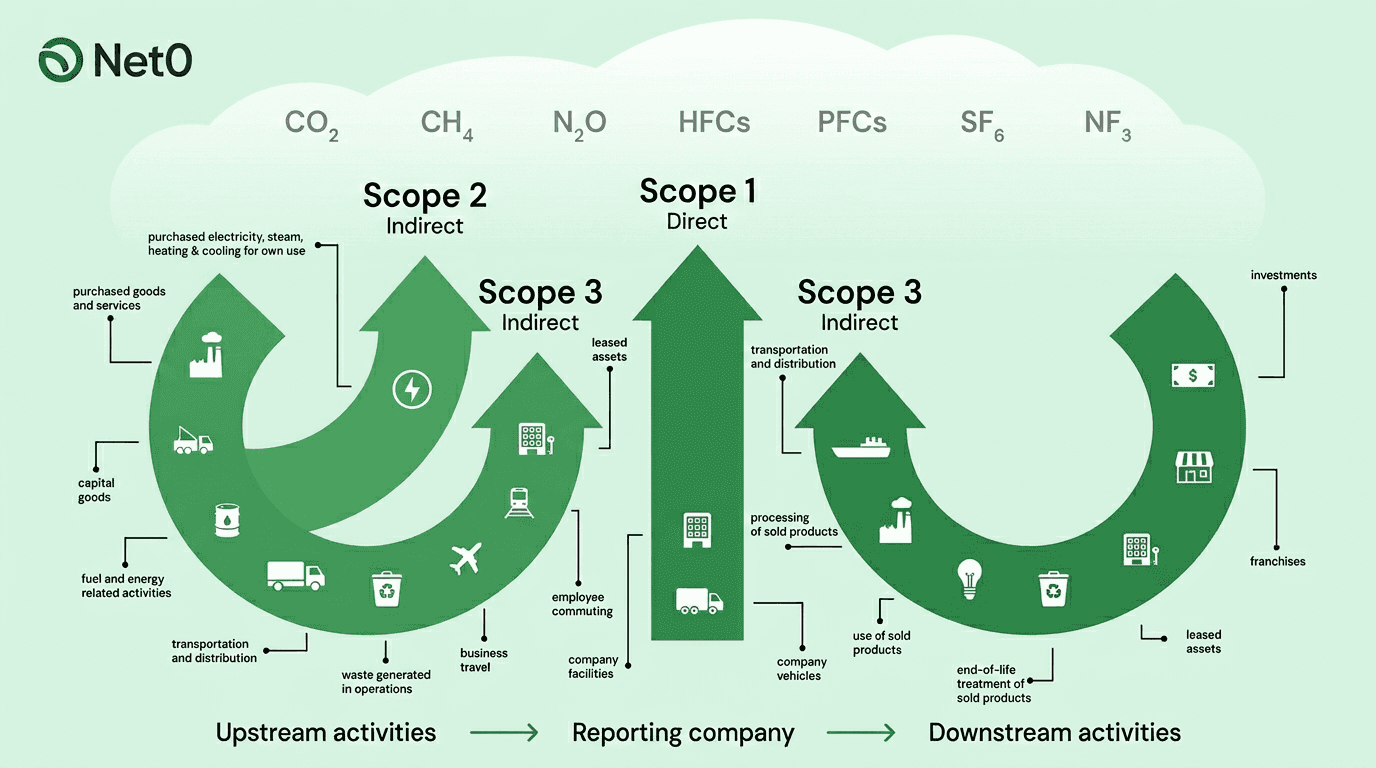

Scope 3 Emissions Defined

Scope 3 emissions are all indirect greenhouse gas emissions that occur in the value chain of a reporting company, both upstream and downstream, that are not included in Scope 1 or Scope 2. The Greenhouse Gas Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard defines them as emissions from sources not owned or directly controlled by the reporting organization but related to its activities.

In practical terms, the Scope 3 emissions of one organization are the Scope 1 and 2 emissions of another. A manufacturer's purchased raw materials, for example, generate Scope 1 emissions at the supplier's facility and Scope 3 emissions on the manufacturer's inventory. This interconnected structure means that Scope 3 accounting requires visibility across the entire value chain -- from raw material extraction through product end-of-life disposal.

According to the University of Chicago's 2025 Sustainability Dialogue, Scope 3 emissions account for approximately 75% of a company's total greenhouse gas output. The Thomson Reuters Institute reports that supply chain emissions are on average 11 times higher than direct operational emissions. Despite this, only 40% of companies currently report their Scope 3 emissions -- a gap that regulatory mandates are rapidly closing.

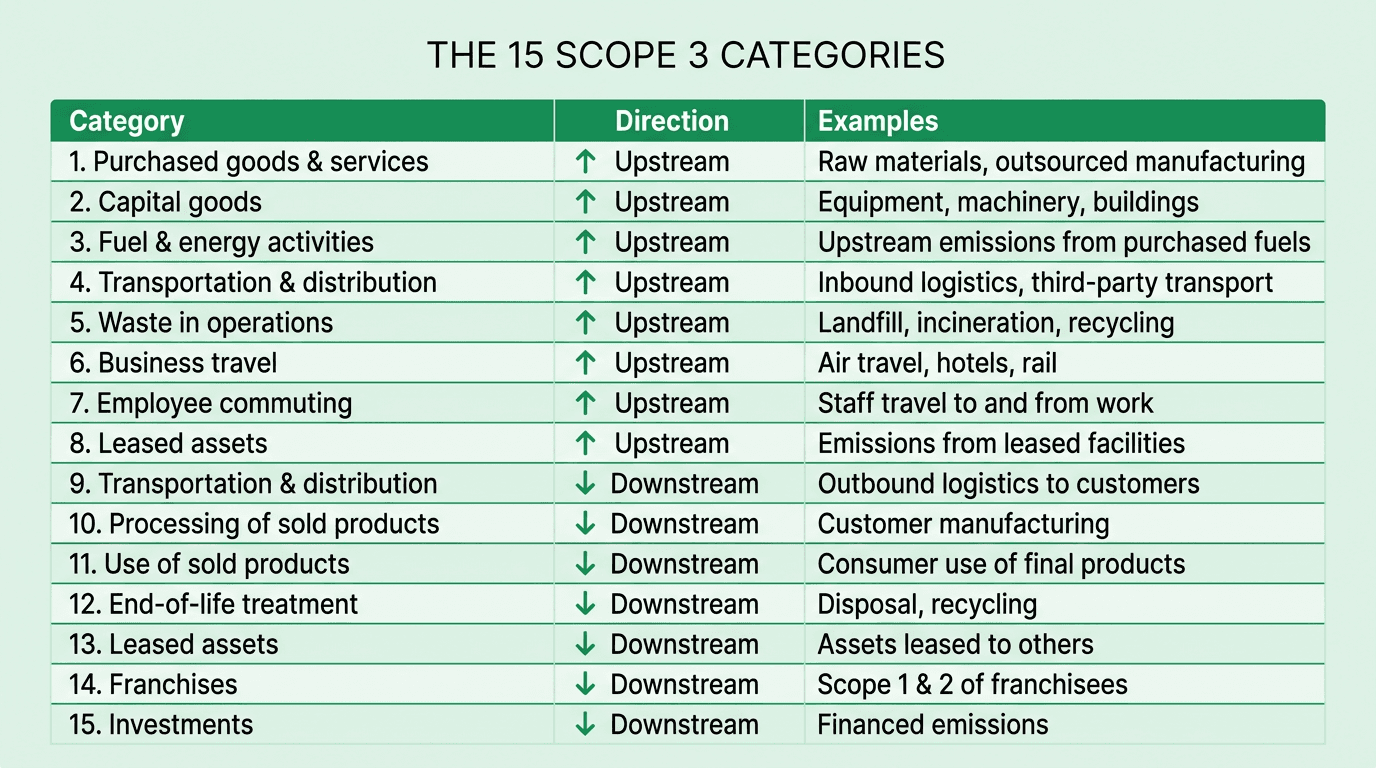

The 15 Categories of Scope 3 Emissions

The GHG Protocol organizes Scope 3 emissions into 15 distinct categories, split between upstream activities (before the product reaches the reporting company) and downstream activities (after the product leaves).

Upstream Categories (1-8):

Purchased goods and services -- Extraction, production, and transportation of all goods and services acquired by the reporting company, including raw materials, outsourced services, and office supplies

Capital goods -- Extraction, production, and transportation of durable goods such as buildings, vehicles, and machinery, calculated on a cradle-to-gate basis

Fuel and energy-related activities -- Upstream emissions from purchased fuels and energy not captured in Scope 1 or 2, including transmission and distribution losses

Upstream transportation and distribution -- Transportation of purchased goods between suppliers and the reporting company's operations, including third-party warehousing

Waste generated in operations -- Disposal and treatment of operational waste, including landfill methane (CH4) and nitrous oxide (N2O) emissions

Business travel -- Employee transportation for business activities across all modes, plus hotel stays and related energy use

Employee commuting -- Transportation of employees between homes and worksites via personal vehicles, public transit, and other modes

Upstream leased assets -- Operation of assets leased by the reporting company that are excluded from Scope 1 and 2 to avoid double counting

Downstream Categories (9-15):

Downstream transportation and distribution -- Transportation and storage of sold products between the company's operations and end consumers

Processing of sold products -- Emissions from downstream companies processing intermediate products sold by the reporting organization

Use of sold products -- Emissions generated by customers during the use of products over their expected lifetime

End-of-life treatment of sold products -- Waste disposal and treatment of sold products at the end of their useful life

Downstream leased assets -- Operation of assets owned by the reporting company and leased to other entities

Franchises -- Scope 1 and 2 emissions of franchisee operations

Investments -- Emissions from equity, debt, and project finance investments, particularly relevant for financial institutions

For most companies, Category 1 (purchased goods and services) represents the largest single source of Scope 3 emissions. According to PwC's 2024 analysis, this category alone can account for 40-60% of a company's total Scope 3 footprint, making supplier engagement the highest-leverage intervention for emissions reduction.

The Regulatory Landscape for Scope 3 Reporting

Scope 3 reporting has shifted from voluntary best practice to legal obligation across multiple jurisdictions. Understanding the current regulatory environment is essential for compliance planning and resource allocation.

EU Corporate Sustainability Reporting Directive (CSRD): Under the CSRD, Scope 3 reporting is mandatory for all in-scope companies where value chain emissions are material. Reporting must align with European Sustainability Reporting Standards (ESRS), specifically ESRS E1 on climate change. Following the Omnibus I revisions approved in December 2025, the scope narrowed to large EU companies with over 1,000 employees and over EUR 450 million in net annual turnover. The first wave of large listed entities began reporting in 2025, with large non-listed entities starting in 2028.

Science Based Targets initiative (SBTi): The SBTi requires companies to set Scope 3 targets if these emissions represent 40% or more of total Scope 1, 2, and 3 emissions -- a threshold that applies to the vast majority of companies. Near-term targets must cover at least 67% of total Scope 3 emissions, while net-zero long-term targets require coverage of at least 90%. According to SBTi's April 2026 Criteria Assessment Indicators, companies may not exclude more than 5% of emissions from their total Scope 3 inventory.

California SB 253: California's Climate Corporate Data Accountability Act requires Scope 3 reporting starting in 2027 for companies doing business in the state with over $1 billion in annual revenue, affecting an estimated 10,000+ businesses.

SEC Climate Disclosure: The U.S. Securities and Exchange Commission finalized climate disclosure rules in March 2024 but issued a voluntary stay in April 2024. As of March 2026, the rule has never taken effect, with the SEC launching a formal review of climate disclosure requirements. Despite the federal rule's limbo, companies face active mandates from the CSRD, California, and ISSB standards adopted across 36+ jurisdictions.

For organizations tracking regulatory developments, Net0's compliance and reporting resources provide detailed analysis of each framework.

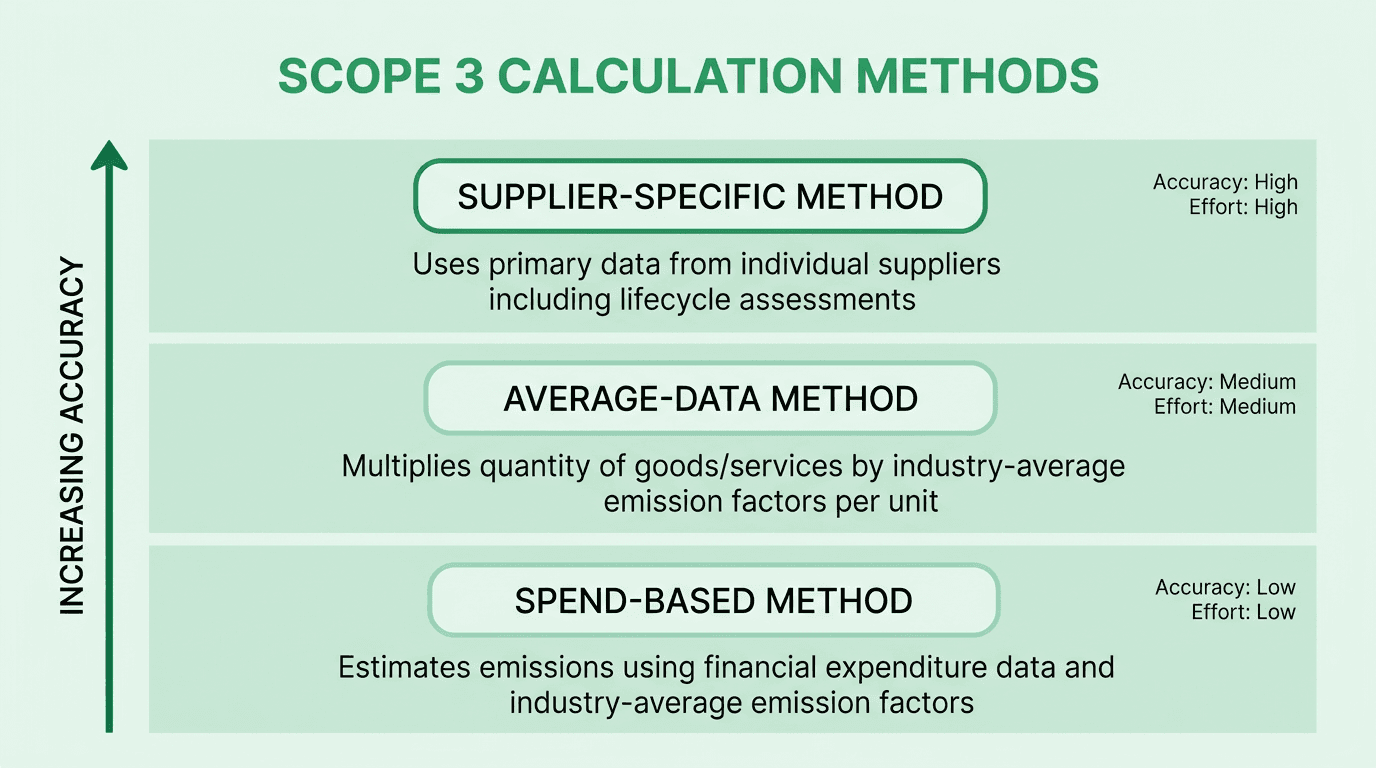

Scope 3 Calculation Methods

Three primary methodologies exist for calculating Scope 3 emissions, each representing a different tradeoff between accuracy and implementation effort. Most organizations use a hybrid approach, applying higher-accuracy methods where data is available and lower-accuracy methods for less accessible categories.

Spend-based method: The most accessible starting point. This approach multiplies the economic value of purchased goods and services by industry-average emission factors per unit of currency. According to PwC's 2024 analysis, approximately 60% of companies begin their Scope 3 journey with spend-based estimates. The method is straightforward to implement using existing financial data but produces the least precise results, as it cannot distinguish between high-emission and low-emission suppliers within the same industry category.

Average-data method: A moderate-accuracy approach that multiplies the quantity of goods or services purchased (measured in physical units such as kilograms, liters, or kilowatt-hours) by industry-average emission factors per unit. This method improves on spend-based estimates by removing price fluctuations from the calculation but still relies on sector averages rather than supplier-specific data.

Supplier-specific method: The highest-accuracy approach, using primary data from individual suppliers, including lifecycle assessments and product-level carbon footprints. According to the GHG Protocol Technical Guidance, supplier-specific data produces the most accurate inventories and enables targeted reduction strategies. The method requires deep supplier engagement and robust data collection infrastructure but delivers the granularity needed for audit-grade reporting.

The optimal approach for most enterprises is a progressive transition: begin with spend-based estimates for comprehensive coverage, then systematically upgrade high-impact categories to average-data and supplier-specific methods as carbon accounting methodologies mature across the supply chain.

Why Scope 3 Measurement Drives Business Value

Measuring Scope 3 emissions is not solely a compliance exercise. Organizations that invest in comprehensive value chain accounting gain measurable advantages across five dimensions.

Regulatory preparedness: With CSRD, SBTi, California SB 253, and ISSB frameworks converging on mandatory Scope 3 disclosure, early measurement avoids the costly scramble of last-minute compliance. According to a 2025 CFO Brew analysis, organizations that delay Scope 3 accounting face 3-5 times higher implementation costs compared to those that build infrastructure proactively.

Investor confidence: Capital allocation increasingly depends on climate data quality. Thomson Reuters Institute reports that 90% of FTSE 100 companies will only work with suppliers that share their ESG credentials. Meanwhile, investment firms managing over $130 trillion in assets have committed to net-zero portfolios through the Glasgow Financial Alliance for Net Zero (GFANZ), making Scope 3 disclosure a prerequisite for accessing growth capital.

Supply chain resilience: Scope 3 measurement reveals concentration risks, resource dependencies, and emission hotspots across the value chain. According to MIT Sloan's 2024 research, companies that quantify their Scope 3 footprint identify 15-25% more supply chain risks than those relying on traditional risk assessments alone.

Cost reduction: Emissions are a proxy for resource inefficiency. Organizations that systematically reduce Scope 3 emissions typically achieve 8-15% procurement cost savings through supplier consolidation, logistics optimization, and energy efficiency improvements, according to McKinsey's 2024 analysis of the materials value chain.

Competitive differentiation: Over half of Gen Z and Millennial consumers consider sustainability before purchasing, according to Deloitte's 2024 Global Sustainability & Consumer Study. Companies with verified Scope 3 data can substantiate sustainability claims, reducing greenwashing risk and building trust with both consumers and B2B procurement teams who are increasingly embedding carbon criteria into vendor selection.

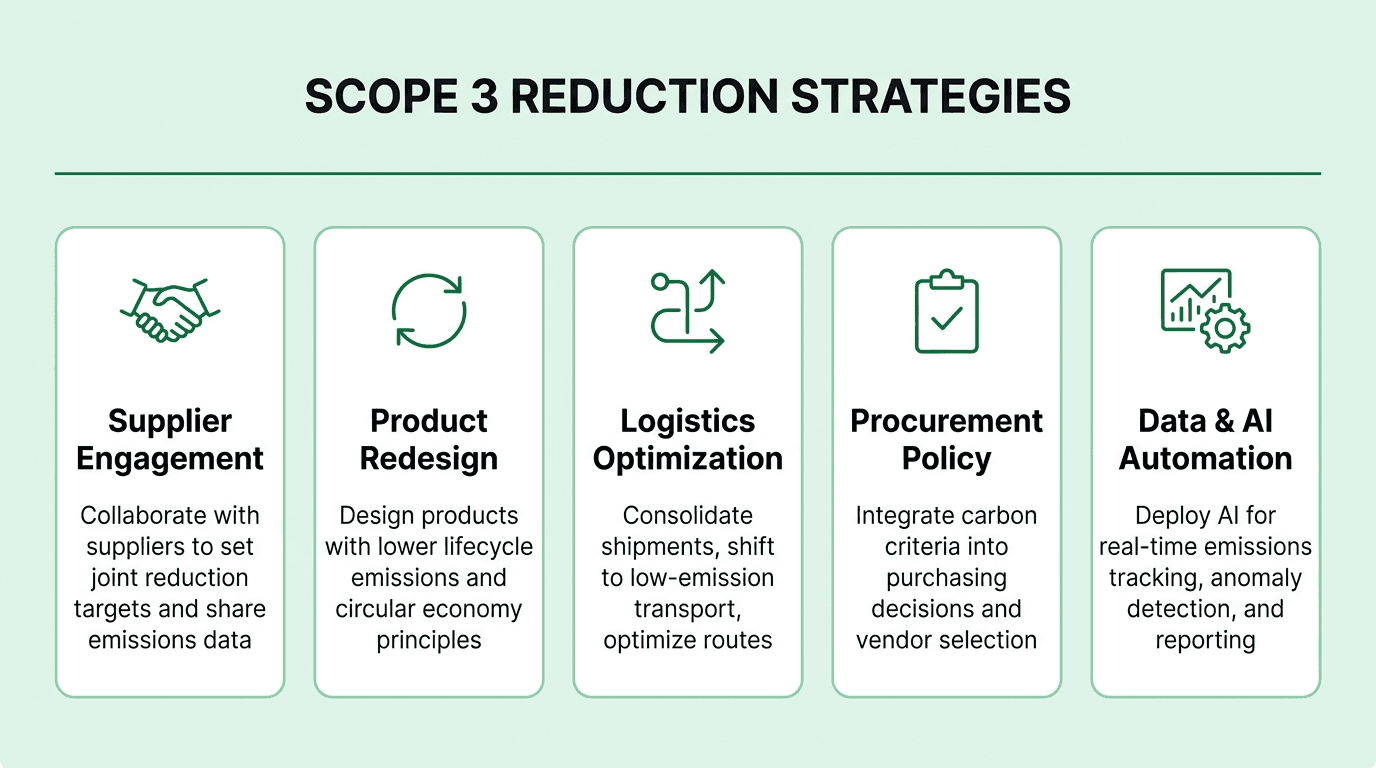

Reduction Strategies for Scope 3 Emissions

Reducing Scope 3 emissions requires coordinated action across five strategic levers, each targeting different parts of the value chain.

Supplier engagement: Collaborate directly with high-emission suppliers to set joint reduction targets, share emissions data, and co-invest in cleaner production methods. According to the World Economic Forum's 2023 analysis, supplier engagement programs targeting the top 20 suppliers by emissions volume can address 70-80% of Category 1 emissions. This approach aligns with the SBTi's supplier engagement target pathway, which allows companies to count supplier commitments toward their own Scope 3 reduction goals.

Product redesign: Design products with lower lifecycle emissions by selecting lower-carbon materials, improving energy efficiency during use, and engineering for circularity and end-of-life recovery. According to McKinsey's 2024 materials value chain report, product-level interventions can reduce lifecycle emissions by 20-40% in sectors such as construction, packaging, and automotive manufacturing.

Logistics optimization: Consolidate shipments, shift to lower-emission transport modes (rail and maritime over road and air), and optimize distribution routes. The International Transport Forum estimates that logistics optimization strategies can reduce transportation emissions by 30-50% while simultaneously lowering freight costs by 10-15%.

Procurement policy: Integrate carbon criteria into purchasing decisions and vendor selection. This includes setting maximum emission intensity thresholds for purchased goods, weighting sustainability performance in RFP evaluations, and progressively transitioning spend toward verified low-carbon suppliers.

Data and AI automation: Deploy AI-powered platforms for real-time emissions tracking, anomaly detection, spend-to-emissions mapping, and automated supplier scoring. AI-driven systems can process emissions data from thousands of suppliers simultaneously, identify data quality issues, and flag reduction opportunities that manual analysis would miss. See the section below on how AI transforms Scope 3 management.

How AI Transforms Scope 3 Management

The core challenge of Scope 3 accounting is data -- collecting it from thousands of suppliers, normalizing it across inconsistent formats, applying the correct emission factors, and maintaining accuracy over time. A 2025 Harvard Business School study found that 74% of S&P 500 firms revised their emissions data at least once between 2010 and 2020, underscoring the difficulty of maintaining reliable climate inventories through manual processes.

AI-powered platforms address this challenge across four capabilities:

Automated data collection: AI systems integrate with ERP platforms, procurement databases, logistics management systems, IoT sensors, and supplier portals to automatically ingest emissions-relevant data. Net0's platform connects to over 10,000 enterprise systems, eliminating the manual data compilation that consumes an estimated 40-60% of sustainability teams' time, according to Sphera's 2024 supply chain survey.

Intelligent emission factor matching: With over 50,000 emission factors in its database, Net0's AI matches each data point to the most appropriate factor based on geography, industry, product type, and calculation methodology. This replaces the error-prone manual process of selecting factors from static lookup tables.

Anomaly detection and data quality assurance: Machine learning models identify outliers, missing data, and inconsistencies in supplier-reported emissions data -- flagging entries that fall outside expected ranges for further review. This capability is particularly critical given the Harvard Business School finding that emissions data revisions are widespread even among the largest public companies.

Scenario modeling and reduction planning: AI-powered simulation tools allow organizations to model the impact of different reduction strategies before committing resources. By testing scenarios such as supplier switching, logistics restructuring, or product redesign, teams can identify the highest-impact, lowest-cost interventions and build data-backed decarbonization strategies.

Scope 3 Double Counting and Data Quality

Double counting occurs when the same emission reduction is claimed by more than one party -- a structural risk inherent to Scope 3 accounting, where one organization's Scope 3 is another's Scope 1 or 2. The Gold Standard defines double counting as "the scenario wherein the benefit of a single GHG Emission Reduction unit is used on more than one occasion to sell to third parties for financial gain, offsetting, or to achieve regulated targets, or to be included in an account or inventory to avoid purchasing reduction units."

The Harvard Business School's 2025 analysis of S&P 500 emissions data highlights the scale of the data quality challenge: 74% of firms revised their reported emissions at least once over a decade, with Scope 3 data being the most frequently adjusted category due to estimation uncertainties and evolving calculation methodologies.

AI-powered carbon accounting platforms mitigate double counting risk through three mechanisms: consistent application of organizational and operational boundaries across all categories, automated reconciliation of supplier-reported data against industry benchmarks, and transparent audit trails that record every data source, emission factor, and calculation methodology. GHG Protocol-compliant platforms that maintain these records make it significantly harder for double counting to go undetected.

For organizations seeking to deepen their understanding of Scope 3 complexities, Net0 maintains detailed resources on common Scope 3 myths and frequently asked Scope 3 questions.

Net0's Approach to Scope 3 Emissions Management

Net0, an AI infrastructure company serving governments and global enterprises across four continents, provides an end-to-end platform for Scope 3 measurement, reduction, and reporting. The platform supports all 15 GHG Protocol Scope 3 categories alongside Scope 1 and 2 emissions, delivering a unified view of the complete carbon footprint.

Net0's Scope 3 capabilities include automated data collection from 10,000+ enterprise systems, 50,000+ emission factors covering all major geographies and industries, support for 30+ reporting frameworks including GHG Protocol, CSRD, CDP, GRI, ISSB, and SBTi, and scenario simulation tools for testing reduction strategies before deployment.

The platform is trusted by 400+ entities across four continents, including Fortune 500 companies and government organizations, with sovereign and hybrid deployment options for organizations requiring data residency.

Book a demo to see how Net0 automates Scope 3 emissions measurement and accelerates value chain decarbonization.

Frequently Asked Questions

What is the difference between Scope 1, 2, and 3 emissions?

Scope 1 covers direct emissions from owned or controlled sources. Scope 2 covers indirect emissions from purchased energy. Scope 3 covers all other indirect emissions across the value chain, both upstream (suppliers) and downstream (customers, end-of-life). Scope 3 typically represents approximately 75% of total corporate emissions.

Are Scope 3 emissions mandatory to report?

Under the EU's CSRD, Scope 3 reporting is mandatory for in-scope companies where value chain emissions are material. The SBTi requires Scope 3 targets when these emissions exceed 40% of total emissions. California's SB 253 mandates Scope 3 reporting from 2027 for large companies.

What are the 15 categories of Scope 3 emissions?

The GHG Protocol defines 8 upstream categories (purchased goods, capital goods, fuel and energy, transportation, waste, business travel, commuting, leased assets) and 7 downstream categories (transportation, processing, use of products, end-of-life, leased assets, franchises, investments).

How do companies calculate Scope 3 emissions?

Three primary methods exist: spend-based (using financial data and industry-average emission factors), average-data (using physical quantities and per-unit factors), and supplier-specific (using primary data from individual suppliers). Most companies use a hybrid approach that progressively upgrades accuracy.

What is the SBTi requirement for Scope 3 targets?

The SBTi requires Scope 3 targets when these emissions represent 40% or more of total emissions. Near-term targets must cover at least 67% of Scope 3 emissions. Long-term net-zero targets require 90% coverage. Companies may not exclude more than 5% from their Scope 3 inventory.

How can AI help with Scope 3 emissions tracking?

AI automates data collection from thousands of sources, matches data to appropriate emission factors, detects anomalies and data quality issues, and models reduction scenarios. AI-powered platforms can process supplier data at scale, reducing manual effort by an estimated 40-60%.

What is double counting in Scope 3 reporting?

Double counting occurs when the same emission reduction is claimed by multiple parties. Since one organization's Scope 3 emissions are another's Scope 1 or 2, overlapping claims are structurally possible. GHG Protocol-compliant carbon accounting platforms prevent this through consistent boundary definitions and automated reconciliation.