AI for Sustainability

What Is Carbon Accounting? A 2026 Guide for Enterprises

Carbon accounting measures an organisation's greenhouse gas emissions in CO2e across Scope 1, 2, and 3. Net0's AI infrastructure automates the inventory, methodology, and disclosure end to end.

Sofia Fominova

Apr 21, 2026

TL;DR: Carbon accounting is the structured measurement and reporting of an organisation's greenhouse gas (GHG) emissions in carbon dioxide equivalents (CO2e), across its direct operations and value chain. In 2026, accurate carbon accounting is the data foundation for compliance with the EU's revised CSRD, IFRS S2, CDP, and SBTi — and it is increasingly run on AI. Net0, an AI infrastructure company that builds AI solutions for governments and global enterprises, automates carbon accounting end to end across Scope 1, 2, and 3 emissions, multi-framework reporting, and decarbonisation planning.

Key Takeaways

Carbon accounting quantifies an organisation's GHG emissions in CO2e using the GHG Protocol Corporate Standard as the global reference, with ISO 14064-1:2018 providing the corresponding ISO specification at the organisational level.

The EU's Omnibus I Directive (EU 2026/470), in force from March 2026, narrows the CSRD to companies with more than 1,000 employees and over €450 million in net annual turnover — about 5,000 companies, down from roughly 50,000 under the original text.

Scope 3 emissions account for an average of 75% of a company's carbon footprint, and corporate supply chain emissions are 26 times larger than direct operational emissions, according to CDP and BCG's 2024 analysis.

Only 7% of large companies fully report Scope 1, 2, and 3 emissions, down from 9% in 2024, per the BCG and CO2 AI Climate Survey 2025 of 1,924 executives across 26 countries.

Companies that use AI to support emissions reduction are 4.5 times more likely to capture significant decarbonisation benefits, with leading firms generating financial value worth roughly 10% of revenue.

Introduction

Carbon accounting — sometimes called greenhouse gas accounting — is the discipline of measuring, recording, and reporting the GHG emissions associated with an organisation's activities, expressed in carbon dioxide equivalents (CO2e). It is the foundation of every credible climate target, every regulated sustainability disclosure, and every operational decarbonisation programme.

Net0 is an AI infrastructure company that builds AI solutions for governments and global enterprises, with carbon accounting as one of its core sustainability workloads. This article explains what carbon accounting is, how the GHG Protocol scopes work, the methodologies and standards that apply in 2026, where most programmes still fail, and how AI changes the unit economics of getting it right.

What is carbon accounting?

Carbon accounting is the structured process of identifying, quantifying, and reporting an organisation's greenhouse gas emissions, expressed in CO2e. CO2e converts the warming impact of all GHGs — methane, nitrous oxide, hydrofluorocarbons, and others — into a single comparable unit, using global warming potential (GWP) values published by the IPCC.

The global reference text is the GHG Protocol Corporate Accounting and Reporting Standard, developed by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD). It defines five accounting principles — relevance, completeness, consistency, transparency, and accuracy — and the boundaries that determine which emissions an entity is responsible for.

Carbon accounting differs from a one-off carbon footprint exercise. A footprint is a snapshot; carbon accounting is a continuous, auditable inventory tied to an organisational and operational boundary, with documented methods, emission factors, base years, and recalculation policies. That distinction is what makes it usable for ESG reporting, regulatory disclosure, and target setting under the Science Based Targets initiative (SBTi).

Why carbon accounting matters in 2026

Carbon accounting is no longer a voluntary exercise. It is the data layer that determines whether an organisation can comply with mandatory climate disclosure regimes, retain access to capital, and stay in the supply chains of large customers.

Regulation has moved on. The EU's Omnibus I Directive (EU 2026/470), adopted in February 2026, narrows the CSRD to companies with more than 1,000 employees AND over €450 million in net annual turnover — roughly 5,000 companies in scope, against the ~50,000 covered by the original text. Reporting still uses the European Sustainability Reporting Standards (ESRS) and still requires Scope 1, 2, and material Scope 3 emissions. In parallel, IFRS S2 — the International Sustainability Standards Board's climate-disclosure standard — has been adopted or is being adopted in more than 30 jurisdictions, including the UK, Australia, Hong Kong, Singapore, Japan, and Brazil. In the United States, SEC climate-related disclosure is in regulatory limbo, but state-level rules such as California's SB 253 and SB 261 require large companies operating in California to disclose Scope 1, 2, and Scope 3 emissions and climate-related financial risk.

Investors and buyers demand auditable data. In 2025, 640 investors with US$127 trillion in assets requested CDP disclosures, and more than 270 major buyers asked approximately 45,000 suppliers to disclose environmental data through CDP's Supply Chain Programme. More than 22,100 companies disclosed environmental data through CDP in 2025, representing over half of global market capitalisation.

The capital implications are now measurable. BCG and CO2 AI's 2025 climate survey of 1,924 executives across 16 industries and 26 countries found that the leading group of climate-mature companies captures financial benefits worth approximately 10% of revenue. That value depends on having a defensible carbon inventory in the first place.

The Scope 1, 2, and 3 framework

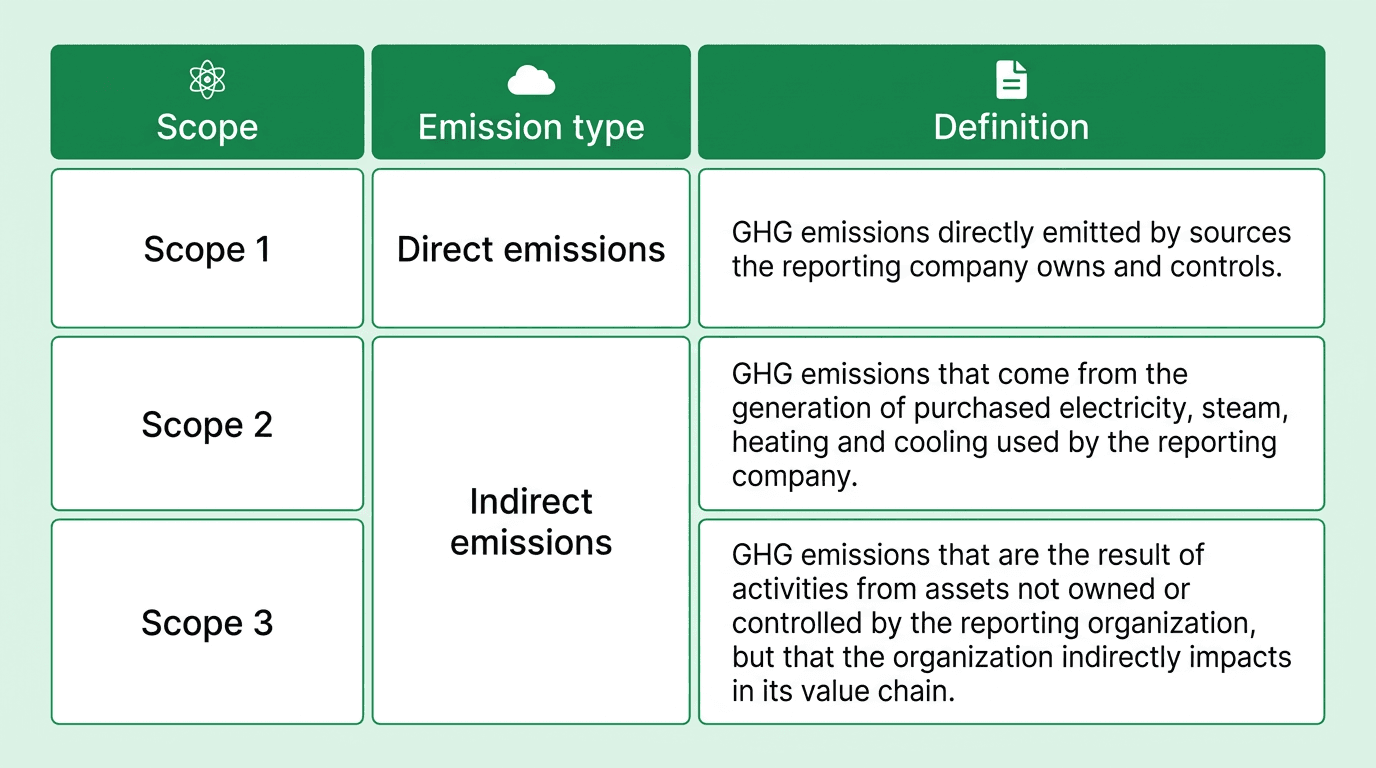

Carbon accounting is organised around three "scopes" defined by the GHG Protocol. The scopes determine where an emission sits in an organisation's inventory and which methodology applies.

Scope 1 — direct emissions from owned or controlled sources: on-site fuel combustion, company vehicles, refrigerant leaks, process emissions.

Scope 2 — indirect emissions from purchased electricity, steam, heat, and cooling. Scope 2 must be reported under both the location-based and market-based methods.

Scope 3 — all other indirect emissions across the value chain, organised into 15 categories spanning purchased goods and services, capital goods, transportation, business travel, use and end-of-life of sold products, investments, and franchises.

For most large enterprises, Scope 3 emissions are the majority of total emissions and the hardest to measure. CDP estimates Scope 3 averages 75% of a company's footprint and reaches close to 100% in financial services. CDP and BCG's 2024 supply chain analysis found that corporate supply chain Scope 3 emissions are, on average, 26 times higher than direct operational emissions.

A complete carbon inventory covers all three scopes. The deeper guide to the framework, including each of the 15 Scope 3 categories, is in the dedicated Scope 1, 2, and 3 emissions explainer, with common misunderstandings addressed in Scope 3 myths.

Carbon accounting methodologies

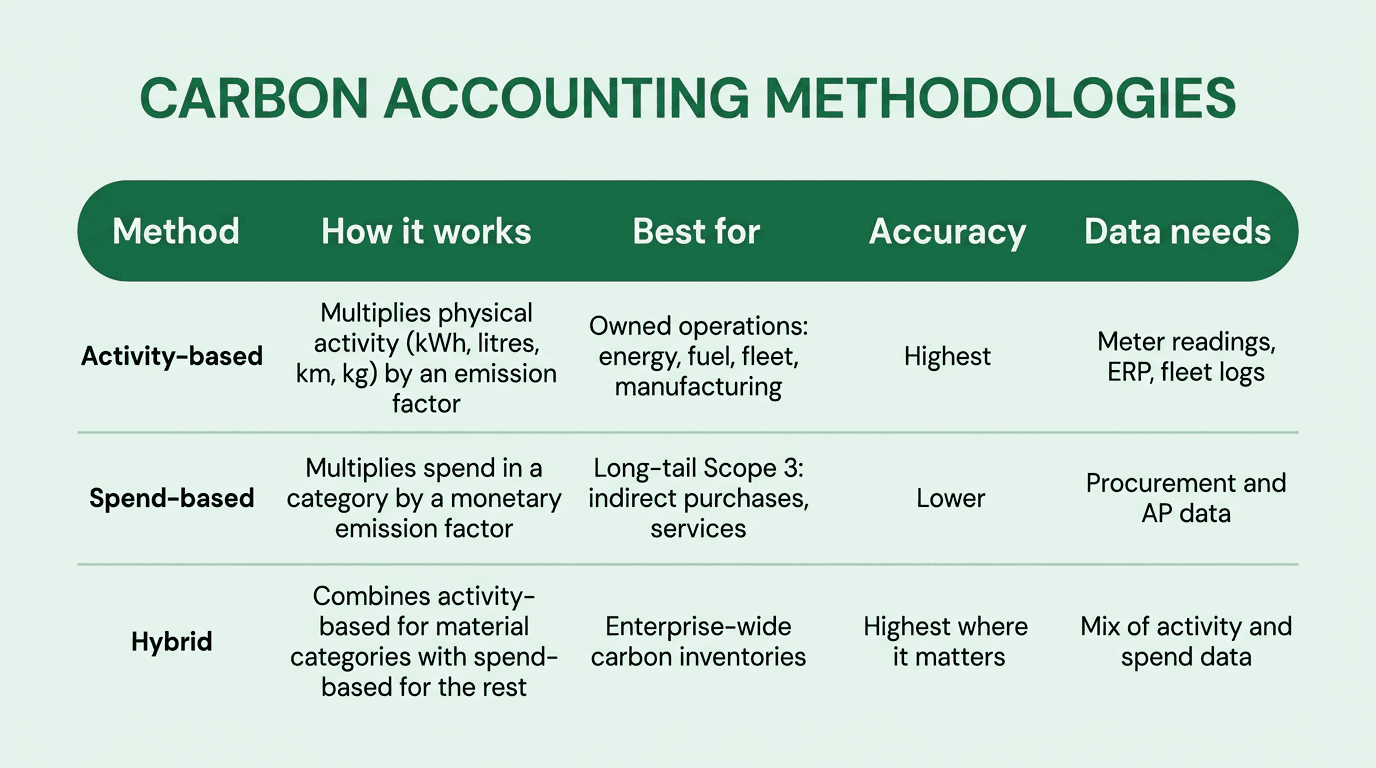

Once the boundary is set, every emission has to be calculated using a defined methodology. There are three dominant approaches: activity-based, spend-based, and hybrid. Choice of method drives accuracy, audit defensibility, and how reductions are tracked over time.

Activity-based uses physical activity data — kWh of electricity, litres of fuel, kilometres driven, kilograms of material — multiplied by an emission factor in kgCO2e per unit. It is the most accurate method and the one regulators and assurance providers prefer for material categories.

Spend-based multiplies financial spend in a category by a monetary emission factor (kgCO2e per dollar). It is fast and broad-coverage but carries large uncertainty ranges, often plus or minus 40–60% on Scope 3 estimates. It is appropriate as a screening method for the long tail of immaterial categories or where supplier data is not yet available.

Hybrid combines activity-based methods for material categories — typically the top three to five Scope 3 categories that account for 80% of value-chain emissions — with spend-based methods for the rest. This is the dominant approach for enterprise-wide carbon inventories and the one most platforms support.

The full comparison, including production-based factors used in heavy industry, is set out in the emission factor comparison guide, with broader methodology context in the carbon accounting methodologies explainer.

Standards and frameworks that govern carbon accounting

Carbon accounting is governed by a stack of methodological standards (how to measure) and disclosure frameworks (what to report). The relationships between them matter — the same underlying inventory typically feeds several frameworks at once.

GHG Protocol Corporate Standard — the foundational methodological standard, used by virtually every disclosure framework worldwide. The Corporate Value Chain (Scope 3) Standard and Product Life Cycle Standard extend it. A targeted update to Scope 3 measurement is being finalised in 2026.

ISO 14064 — the ISO specification for GHG quantification, reporting, and verification. It has three parts, all updated in 2018–2019:

ISO 14064-1:2018 — organisation-level GHG inventories.

ISO 14064-2:2019 — GHG project-level emission reductions and removals.

ISO 14064-3:2019 — verification and validation of GHG statements.

ISO 14064-1 and the GHG Protocol Corporate Standard are largely compatible; many organisations measure under the GHG Protocol and have their inventory verified against ISO 14064-3. (The "Corporate Accounting and Reporting Standard (CAR)" referenced in some older Net0 content was a misnaming of the GHG Protocol Corporate Standard — there is no separate IASB standard by that name. GHG reporting sets out the GHG Protocol in full.)

CDP — the largest global environmental disclosure platform. In 2025, more than 22,100 companies disclosed climate, water, forests, biodiversity, and plastics data through CDP, and CDP's questionnaires are aligned with IFRS S2 as the foundational baseline.

SBTi — the Science Based Targets initiative validates corporate emissions-reduction targets against the Paris Agreement 1.5°C pathway. SBTi requires Scope 3 targets for companies whose Scope 3 emissions exceed 40% of total emissions, with the target covering at least two-thirds of total Scope 3.

IFRS S1 and S2 — the ISSB's general and climate-specific sustainability disclosure standards. IFRS S2 has been effective since January 2024 and is now adopted (or being adopted) in more than 30 jurisdictions. Targeted GHG amendments issued in December 2025 take effect from January 2027.

CSRD and ESRS — the EU's mandatory disclosure regime, narrowed in 2026 by the Omnibus I Directive but still applying double materiality, full Scope 1 and 2 disclosure, and material Scope 3 disclosure for in-scope undertakings.

California SB 253 and SB 261 — US state-level Scope 1, 2, and 3 disclosure for large companies operating in California.

CBAM — the EU Carbon Border Adjustment Mechanism, in its definitive financial regime from January 2026, requires importers of cement, iron and steel, aluminium, fertilisers, electricity, and hydrogen to account for embedded emissions in imported goods.

Why carbon accounting still fails at most large enterprises

Despite over 20 years of standards, most large organisations cannot produce a complete, current, audit-ready emissions inventory. The data shows a gap between regulatory ambition and operational reality.

The BCG and CO2 AI Climate Survey 2025 — based on responses from 1,924 executives at companies collectively responsible for around 40% of global GHG emissions — found that only 7% of these large firms fully report emissions across Scopes 1, 2, and 3, down from 9% in 2024 and 10% in 2023. Only 13% have set targets covering all three scopes, and only 12% comprehensively measure climate-related physical and transition risk.

The earlier BCG GAMMA emissions measurement survey of 1,290 organisations identified the structural causes that have not gone away:

86% of respondents recorded and reported emissions manually using spreadsheets.

81% omitted some internal emissions, and 66% reported no value-chain emissions at all.

The estimated average error rate on measured emissions was 30–40%.

The pattern is consistent across more recent supply-chain research: only 38% of CDP-disclosing companies report any Scope 3 targets, fewer than 35% of those reporting Scope 3 use supplier-specific data rather than spend-based estimates, and CDP's supply chain programme, the most established mechanism, sees roughly 70% supplier response rates with significant variability in data quality. The deeper structural reasons — fragmented systems, manual data capture, supplier engagement gaps — are explored in data collection challenges from factory emissions and manufacturing impacts.

The implication is straightforward: at institutional scale, manual carbon accounting does not produce reliable, decision-grade data. The fix is not more spreadsheets — it is purpose-built AI infrastructure that can ingest, classify, and reason over enterprise data continuously.

AI-powered carbon accounting

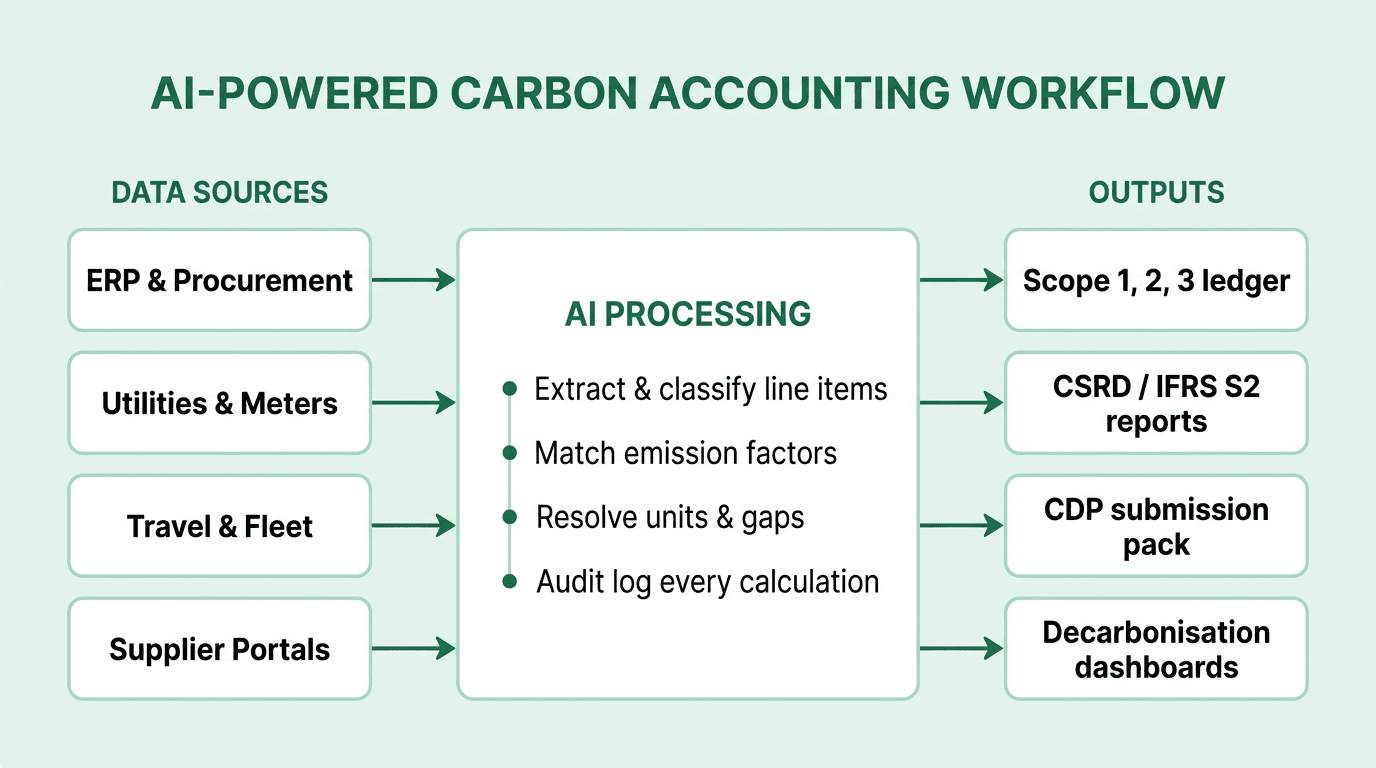

AI is changing the unit economics of carbon accounting by replacing manual classification, factor matching, and reconciliation with automated, auditable workflows. The shift is most material in three places: data ingestion, factor matching, and assurance.

Data ingestion at enterprise scale. Modern AI carbon accounting systems integrate with ERP, procurement, utility, travel, fleet, and supplier-portal data, and use large language models to extract and classify millions of unstructured line items per month. For a single Fortune 500 customer, Net0 processes around 1.2 million invoices a month into classified, factor-matched emissions. The same architecture is documented in Net0's automated data collection work.

Emission factor matching. Net0's platform applies more than 50,000 verified emission factors to that activity data, matching transactions to the right factor based on category, geography, supplier, and methodology, and flagging the calculation method (activity, spend, or hybrid) so it is auditable.

Assurance and audit. Every calculation is recorded with the source data, the chosen factor, the methodology, and the version of the factor library used at the time. That audit log is what makes ISO 14064-3 verification and CSRD/IFRS S2 limited or reasonable assurance practically achievable — without it, assurance providers cannot trace claims back to source.

The strategic case is now well evidenced. BCG's 2024 climate survey found that companies using AI to support emissions reduction are 4.5 times more likely to experience significant decarbonisation benefits than peers, primarily because automation moves teams from data-gathering to actual reduction work. The broader analysis of why AI is essential to climate action is set out in why AI is essential when tackling climate change.

How to evaluate carbon accounting software

Selecting a carbon accounting platform is a regulated-data infrastructure decision, not an ESG tooling decision. Six criteria separate platforms that hold up under audit and scale from those that produce demo-quality numbers.

Integration breadth. Does the platform ingest from the systems where emissions actually originate — ERP (SAP, Oracle, Microsoft Dynamics), procurement, utilities, fleet, travel, and supplier portals — without manual exports?

Audit defensibility. Does every reported number trace back to a source record, an emission factor, a methodology, and a versioned calculation log? This is the prerequisite for ISO 14064-3 verification and CSRD/IFRS S2 assurance.

Framework coverage. Does the platform support the frameworks the organisation is actually subject to — GHG Protocol, ISO 14064, CDP, SBTi, CSRD/ESRS, IFRS S1/S2, and jurisdiction-specific rules such as California SB 253 and CBAM — from one inventory rather than parallel systems?

AI automation depth. How much of the workflow — line-item classification, factor matching, gap detection, anomaly review — is genuinely automated rather than dependent on manual intervention?

Scope 3 capability. Does the platform support hybrid methods, supplier engagement, primary supplier data exchange (e.g. PACT), and the 15 Scope 3 categories — including the financed-emissions edge cases under IFRS S2?

Sovereign and hybrid deployment. For governments and regulated enterprises, can the platform be deployed on sovereign or hybrid infrastructure so that emissions data, supplier records, and operational data remain under jurisdictional control?

Carbon accounting that fails any of these tests will fail at audit, at framework expansion, or at the scale where it actually matters.

How Net0 supports carbon accounting

Net0 provides AI-powered carbon accounting as one workload on its broader AI infrastructure. The same infrastructure also runs Net0's government AI practice, which is why the architecture is built for institutional data volumes and sovereign deployment from the outset.

For carbon accounting specifically, the platform provides:

60+ modular AI applications spanning measurement, target setting, scenario simulation, Marginal Abatement Cost Curve analysis, and disclosure.

10,000+ integrations with enterprise and public-sector systems — ERP, procurement, fleet, energy, travel, HR.

50,000+ verified emission factors across activity-, spend-, and production-based methodologies, kept current with regulatory and IPCC updates.

30+ supported sustainability frameworks, including GHG Protocol, ISO 14064, CDP, SBTi, GRI, CSRD/ESRS, and IFRS S1/S2.

Sovereign, hybrid, and cloud deployment, matching institutional data-residency requirements.

Deployed across 400+ entities across four continents, including Fortune 500 companies and government customers.

Because measurement, decarbonisation, profitable decarbonisation, target setting, and disclosure share a single AI data layer, the same inventory drives every framework an organisation has to file — without parallel spreadsheets or reconciliation work between teams. More on the company, and an overview of related work is in the blog.

Ready to put carbon accounting on AI infrastructure?

Book a demo to see how Net0's AI infrastructure runs Scope 1, 2, and 3 carbon accounting, multi-framework disclosure, and decarbonisation planning from a single data layer.

FAQ

What is carbon accounting in simple terms?

Carbon accounting is the structured measurement, recording, and reporting of an organisation's greenhouse gas emissions, expressed in carbon dioxide equivalents (CO2e). It quantifies emissions from owned operations (Scope 1), purchased energy (Scope 2), and the value chain (Scope 3), using methods defined by the GHG Protocol.

What is the difference between carbon accounting and a carbon footprint?

A carbon footprint is a one-off snapshot of emissions for a defined boundary — a product, an organisation, an event. Carbon accounting is the continuous, audit-ready inventory that produces those footprints over time, with documented methodology, emission factors, base years, and recalculation policies aligned with the GHG Protocol or ISO 14064-1.

Is carbon accounting mandatory in 2026?

It depends on jurisdiction and size. The EU's revised CSRD applies to companies with more than 1,000 employees and over €450 million in net annual turnover. IFRS S2 has been adopted in more than 30 jurisdictions including the UK, Australia, Hong Kong, Singapore, and Japan. California's SB 253 mandates Scope 1, 2, and 3 disclosure for large companies operating in the state.

What are Scope 1, 2, and 3 emissions?

Scope 1 covers direct emissions from owned or controlled sources. Scope 2 covers indirect emissions from purchased electricity, steam, heat, and cooling. Scope 3 covers all other indirect emissions in the value chain, organised into 15 categories. For most large enterprises, Scope 3 averages 75% of total emissions and is around 26 times larger than direct operations.

How does AI improve carbon accounting?

AI replaces manual classification and reconciliation with automated workflows. It ingests data from ERP, procurement, utilities, and supplier systems, classifies millions of line items, matches them to verified emission factors, and produces an auditable ledger. BCG's 2024 climate survey found that companies using AI to support decarbonisation are 4.5 times more likely to capture significant benefits.

Which carbon accounting standard should a company use?

Most enterprises measure under the GHG Protocol Corporate Standard, which is the methodological reference behind every major disclosure framework — CDP, SBTi, CSRD/ESRS, IFRS S1/S2, and California SB 253. Where third-party verification is required, the inventory is verified against ISO 14064-3:2019. Choice of disclosure framework follows jurisdiction, listing status, and stakeholder requirements rather than personal preference.