AI for Sustainability

SEC Climate Disclosure Rule: 2026 Status, Requirements, and What Companies Should Know

The SEC climate disclosure rule was finalized in 2024 but never took effect. Net0, an AI infrastructure company, explains the current legal status, requirements, and why companies must still prepare for climate reporting.

Sofia Fominova

Apr 14, 2026

TL;DR: The SEC climate disclosure rule was finalized in March 2024 but has never taken effect. The SEC issued a voluntary stay in April 2024, withdrew its legal defense in March 2025, and launched a formal review of climate disclosure requirements in March 2026. Despite the federal rule's limbo, companies face active climate disclosure mandates from California (SB 253, first reports due August 2026), the EU's CSRD, and the ISSB standards now adopted across 36+ jurisdictions.

Key Takeaways:

The SEC's 2024 climate disclosure rule remains under a voluntary stay and has never been enforced — the SEC voted to end its defense of the rule in March 2025

In March 2026, the SEC launched a formal review of climate disclosure requirements, inviting public input on updates to Regulation S-K and S-X

California's SB 253 is enforceable now — companies with over USD 1 billion in revenue doing business in California must report Scope 1 and 2 emissions by August 10, 2026

Over 36 jurisdictions have adopted or are implementing the ISSB standards (IFRS S1 and S2), creating a de facto global baseline for climate disclosure

The SEC's 2010 interpretive guidance requiring disclosure of material climate-related risks remains in effect regardless of the 2024 rule's status

What Is the SEC Climate Disclosure Rule

The SEC climate disclosure rule is a regulation adopted by the U.S. Securities and Exchange Commission on March 6, 2024, requiring publicly traded companies to disclose standardized information about climate-related risks and greenhouse gas emissions. Net0, an AI infrastructure company that builds intelligent systems for governments and global enterprises, provides the AI-powered sustainability platform that helps organizations navigate the evolving climate disclosure landscape across multiple jurisdictions and frameworks.

The rule was modeled on the Task Force on Climate-related Financial Disclosures (TCFD) framework, which the Financial Stability Board created to standardize how companies report climate risks to investors, lenders, and insurers. The TCFD established four disclosure pillars — governance, strategy, risk management, and metrics and targets — that form the structural foundation of the SEC rule.

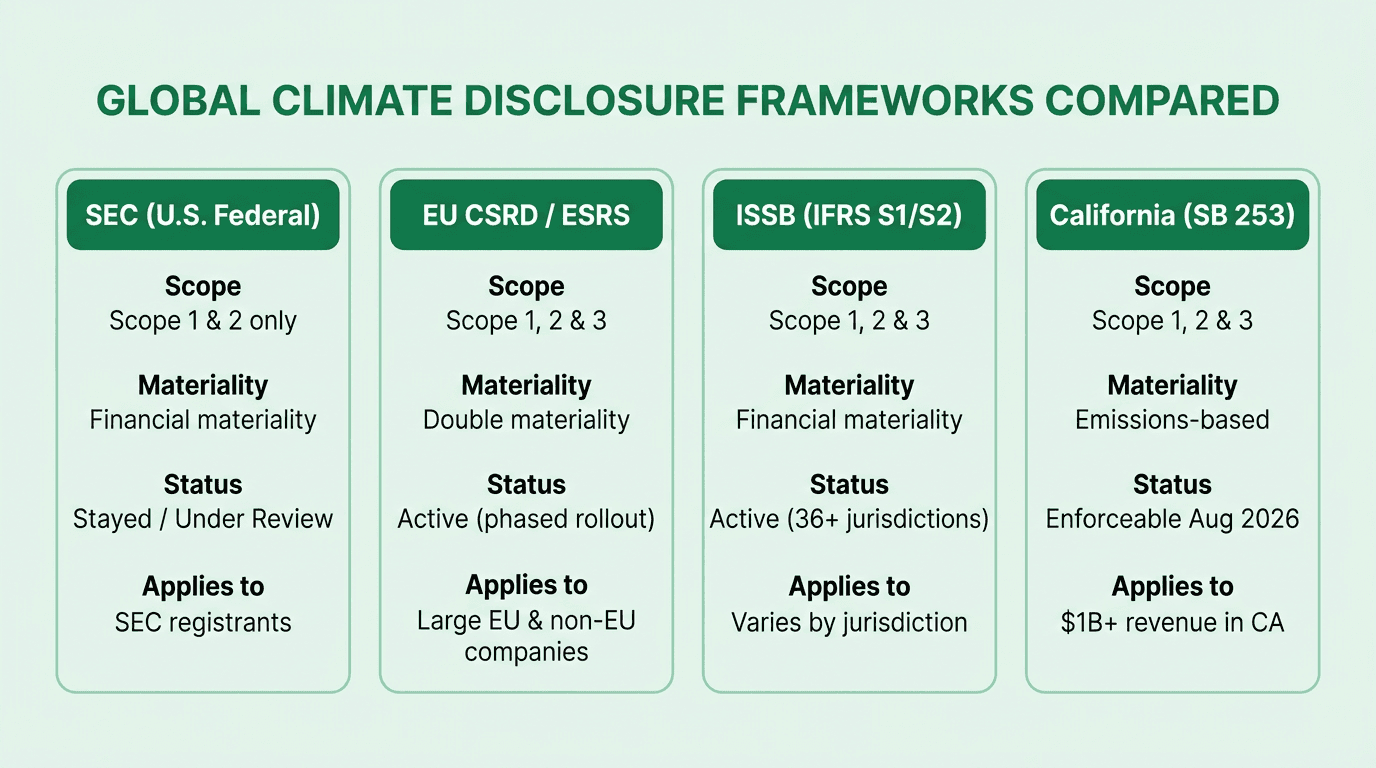

Unlike the EU's Corporate Sustainability Reporting Directive (CSRD), which applies a double materiality lens covering both financial impact and environmental impact, the SEC rule focuses exclusively on financial materiality — how climate risks affect a company's financial condition, results of operations, and cash flows.

Timeline of the SEC Climate Disclosure Rule

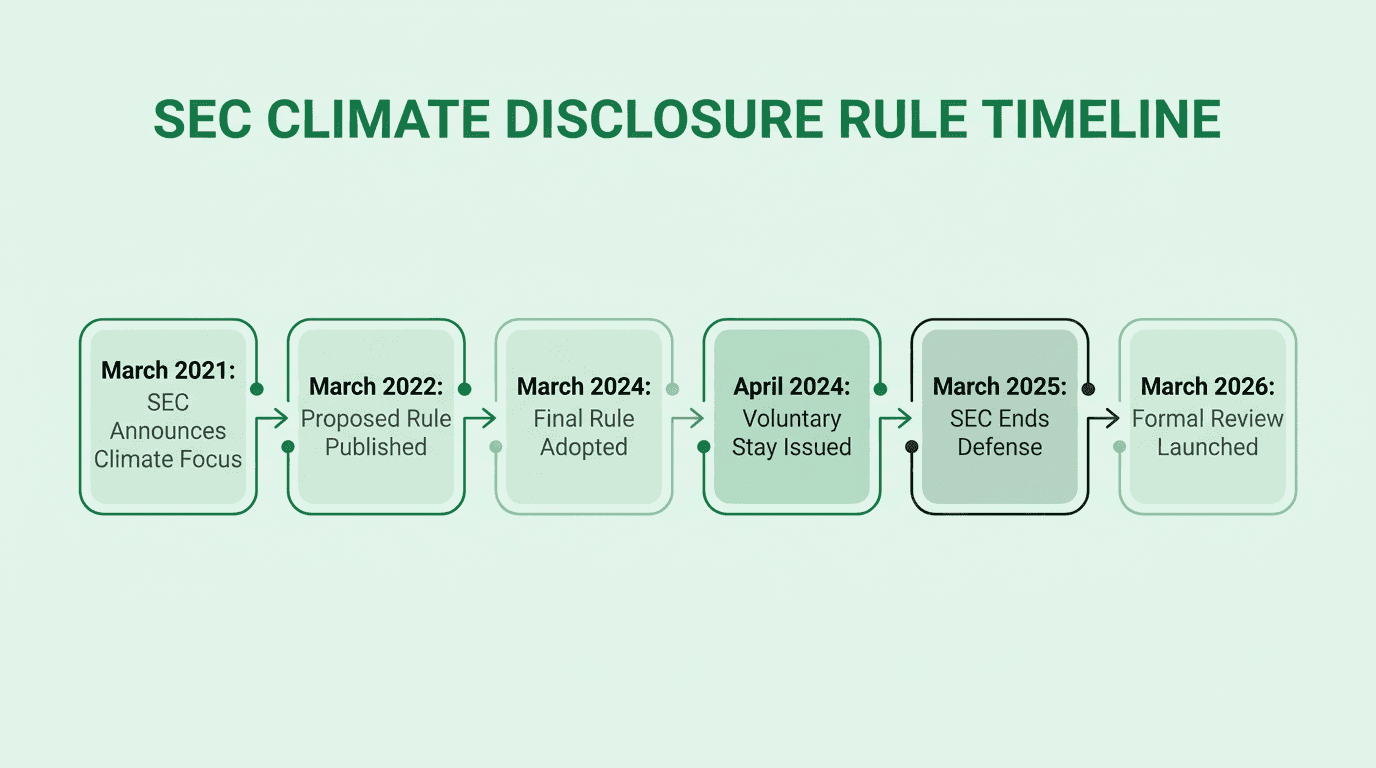

The SEC climate disclosure rule has undergone significant changes since its conception, culminating in a legal and regulatory standoff that remains unresolved as of April 2026.

March 2021: The SEC announced its focus on climate-related disclosures under then-Chair Gary Gensler, signaling that enhanced reporting requirements were forthcoming.

March 2022: The SEC published a proposed rule for enhancing and standardizing climate-related disclosures, opening a public comment period that generated over 16,000 responses.

March 6, 2024: The SEC adopted the final climate disclosure rule, significantly narrower than the 2022 proposal — notably excluding mandatory Scope 3 emissions reporting.

April 2024: Facing consolidated legal challenges in the U.S. Court of Appeals for the Eighth Circuit (Iowa v. SEC, No. 24-1522), the SEC issued a voluntary stay of the rule's effectiveness. The rule has never been enforced.

March 27, 2025: The SEC voted to end its defense of the climate disclosure rule in court. SEC counsel notified the Eighth Circuit that it was no longer authorized to advance the arguments previously filed.

July 2025: The SEC reported to the Eighth Circuit that it did not intend to review or reconsider the rules, effectively leaving them in legal limbo. A coalition of 19 state attorneys general intervened to continue defending the rules independently.

March 2026: The SEC launched a formal review of its climate disclosure framework, inviting public input on potential updates to Regulation S-K and S-X. The comment deadline closed on April 13, 2026.

Current Status of the SEC Climate Rule in 2026

The SEC climate disclosure rule exists in an unprecedented state of regulatory suspension as of April 2026. The rule remains formally on the books — it was lawfully promulgated through the Administrative Procedure Act's notice-and-comment process — but it has never gone into effect and the SEC is not defending it in court.

According to Harvard Law School's analysis, the Eighth Circuit is currently holding the litigation in abeyance. The court has emphasized that the SEC holds the responsibility to determine whether the rules will be rescinded, repealed, modified, or defended. To formally repeal the rule, the SEC would need to follow the APA's notice-and-comment rulemaking process.

The SEC's 2010 interpretive guidance on climate disclosure remains in effect. This guidance requires companies to disclose material climate-related risks as part of their standard reporting obligations under Regulation S-K, including the impact of environmental legislation, international climate agreements, and physical climate changes on business operations.

The March 2026 formal review suggests the SEC may be moving toward a new rulemaking that could either replace, modify, or rescind the 2024 rule. The review invites input from investors, issuers, academics, and data providers on how to focus climate disclosure requirements on material information.

Who the SEC Climate Rules Apply To

The 2024 rule, if it were to take effect, would apply to all companies that file registration statements or periodic reports with the SEC. The compliance timeline was structured in phases based on filer category.

Large accelerated filers — companies with a cumulative worldwide public float exceeding USD 700 million — were designated as the first group to comply. The rule required these companies to include an attestation report from an external auditor covering Scope 1 and Scope 2 emissions disclosures.

Accelerated filers — companies with a public float between USD 75 million and USD 700 million — were given additional time to prepare, with phased-in compliance for emissions disclosures and attestation requirements.

Smaller reporting companies and emerging growth companies were subject to reduced disclosure requirements. Notably, these filers were exempted from the GHG emissions disclosure requirements entirely under the final rule, though they were still required to provide qualitative disclosures about climate-related risks, governance, and risk management processes.

Foreign private issuers — non-U.S. companies listed on U.S. stock exchanges that file 20-F forms — were also within scope, subject to the same phased compliance timeline.

Given the rule's stayed status, none of these compliance deadlines are currently operative. However, companies in these categories should be preparing for disclosure requirements from other jurisdictions, as the regulatory landscape continues to expand globally.

Key Requirements Under the SEC Climate Disclosure Rule

The final SEC climate disclosure rule, as adopted in March 2024, established several categories of mandatory disclosure. Understanding these requirements remains important for companies anticipating future federal regulation or preparing for parallel state and international mandates.

Greenhouse gas emissions reporting. The rule mandated disclosure of Scope 1 (direct) and Scope 2 (indirect from purchased energy) emissions for large accelerated filers and accelerated filers. Critically, the SEC excluded Scope 3 emissions — those from upstream and downstream value chain activities — from the final rule, a significant narrowing from the 2022 proposal. This stands in contrast to the EU's CSRD and California's SB 253, both of which include Scope 3 requirements.

Climate risk disclosures. Companies were required to describe climate-related risks reasonably likely to have a material impact on their business, including both physical risks (extreme weather, sea-level rise, resource scarcity) and transition risks (regulatory changes, market shifts, reputational impacts from the shift to a low-carbon economy).

Governance disclosures. The rule required companies to describe the board's oversight of climate-related risks, management's role in assessing and managing those risks, and any relevant expertise of board members or management on climate matters.

Financial statement metrics. Companies were required to disclose the financial impacts of severe weather events and natural conditions, as well as costs related to carbon offsets and renewable energy credits, within their audited financial statements.

Attestation requirements. Large accelerated filers were required to obtain limited assurance on their Scope 1 and 2 emissions disclosures, eventually escalating to reasonable assurance — a provision designed to enhance data reliability and investor confidence.

The Broader Disclosure Landscape: CSRD, ISSB, and California

While the SEC rule remains in limbo, the global climate disclosure framework has expanded significantly. Companies operating across borders face a complex web of active requirements that demand preparation regardless of U.S. federal action.

EU Corporate Sustainability Reporting Directive (CSRD). The CSRD requires reporting under the European Sustainability Reporting Standards (ESRS), applying a double materiality approach that covers financial materiality and impact materiality. The EU's Omnibus I Directive (March 2026) raised thresholds to 1,000+ employees and EUR 450 million+ turnover. For non-EU multinationals, consolidated reporting is expected to begin in 2029 for fiscal year 2028 data. The CSRD mandates Scope 1, 2, and 3 emissions disclosure — a broader scope than the SEC rule.

ISSB Standards (IFRS S1 and S2). The International Sustainability Standards Board's standards have emerged as the global baseline for climate disclosure. According to the IFRS Foundation, over 36 jurisdictions — including the UK, Australia, Japan, Brazil, and Qatar — have adopted or are implementing IFRS S1 and S2 on a mandatory or voluntary basis. These standards focus on financial materiality and require Scope 1, 2, and 3 emissions disclosure, incorporating the former TCFD framework and SASB industry metrics.

California Climate Legislation. California's SB 253 (Climate Corporate Data Accountability Act) requires U.S.-based entities doing business in California with over USD 1 billion in annual revenue to disclose Scope 1 and 2 emissions starting in 2026, with Scope 3 following in 2027. According to PwC's analysis, the first Scope 1 and 2 report is due by August 10, 2026, with CARB exercising enforcement discretion for the initial year. SB 261 requires climate-related financial risk reports from entities with over USD 500 million in revenue, though its enforcement was paused by a Ninth Circuit injunction.

State-level expansion. New York's Senate passed SB S9072A (modeled on California's SB 253) in February 2026, and legislation has been proposed in Washington, Illinois, and Colorado. The absence of a federal standard is accelerating a patchwork of state-level mandates.

Strategic Preparation for Climate Disclosure

The SEC rule's stayed status does not mean companies can defer climate disclosure preparation. Three converging forces make readiness a strategic imperative.

Multi-jurisdictional exposure. Any company with EU operations, California revenue above USD 1 billion, or listings in ISSB-adopting jurisdictions faces active mandatory disclosure requirements. According to Harvard Business School's Institute for Business in Global Society, the elimination of federal rules has not reduced corporate disclosure obligations — other governments are doing the opposite.

Investor demand. According to PwC's Global Investor Survey, 75% of institutional investors consider ESG reporting an important factor in investment decision-making. The global ESG investing market reached USD 39.08 trillion in 2025 (Fortune Business Insights). Companies without robust climate data face increasing exclusion from institutional portfolios.

Competitive positioning. Organizations that build climate disclosure infrastructure now — automated data collection, carbon accounting systems, multi-framework reporting capabilities — gain a structural advantage. When federal requirements eventually materialize (whether through new SEC rulemaking, Congressional action, or reactivation of the current rule), prepared companies will face weeks of adaptation rather than months of crisis.

The SEC's 2010 guidance also remains operative, meaning material climate risks must be disclosed under existing Regulation S-K regardless of the 2024 rule's status.

How Net0 Supports Climate Disclosure Readiness

Net0, an AI infrastructure company that builds intelligent systems for governments and global enterprises, provides an AI-powered sustainability platform designed for the complexity of the current multi-jurisdictional disclosure environment.

Net0's platform integrates with over 10,000 enterprise systems to automate the end-to-end climate data lifecycle. The platform supports 30+ reporting frameworks — including GHG Protocol, CSRD/ESRS, CDP, GRI, ISSB, and SBTi — enabling organizations to generate compliant disclosures across jurisdictions from a single data set.

Key capabilities for climate disclosure readiness include:

Automated Scope 1, 2, and 3 emissions tracking across 50,000+ emission factors, with real-time dashboards for monitoring progress against decarbonization targets

Multi-framework report generation that maps collected data to SEC, CSRD, ISSB, California SB 253, and other framework-specific requirements simultaneously

AI-driven data validation that identifies gaps, anomalies, and calculation errors before they reach disclosure documents

Sovereign and hybrid deployment options ensuring sustainability data remains under local jurisdiction — a critical requirement for enterprises and governments operating in regulated environments

Net0 serves 400+ entities across four continents, including Fortune 500 companies and governments worldwide.

Book a demo to see how Net0 automates climate disclosure across the SEC, CSRD, ISSB, and California frameworks.

Frequently Asked Questions

What is the SEC climate disclosure rule?

The SEC climate disclosure rule is a regulation adopted on March 6, 2024, requiring SEC-registered companies to disclose climate-related risks, governance processes, and Scope 1 and 2 greenhouse gas emissions in their registration statements and periodic reports.

Is the SEC climate disclosure rule still in effect in 2026?

No. The rule has been under a voluntary stay since April 2024 and has never been enforced. The SEC withdrew its legal defense of the rule in March 2025. In March 2026, the SEC launched a formal review of its climate disclosure framework.

Who does the SEC climate rule apply to?

The rule applies to all SEC registrants, including publicly traded U.S. companies, foreign private issuers filing 20-F forms, and companies filing registration statements. Compliance was phased by filer category, with large accelerated filers (public float over USD 700 million) first.

What emissions must companies disclose under the SEC rule?

The final rule requires disclosure of Scope 1 (direct) and Scope 2 (indirect from purchased energy) emissions for large accelerated filers and accelerated filers. Scope 3 emissions were excluded from the final rule.

How does the SEC rule compare to CSRD and ISSB?

The SEC rule is narrower in scope — it covers only Scope 1 and 2 emissions under a financial materiality lens. The CSRD requires Scope 1, 2, and 3 under double materiality. The ISSB standards require all three scopes under financial materiality. Both CSRD and ISSB are actively enforced in their respective jurisdictions.

Do companies still need to prepare for climate disclosure?

Yes. California's SB 253 requires Scope 1 and 2 reporting by August 2026 for companies with over USD 1 billion in California revenue. The CSRD and ISSB standards apply to multinational operations. The SEC's 2010 guidance also requires disclosure of material climate risks.

How does Net0 help with climate disclosure compliance?

Net0 automates climate data collection from 10,000+ enterprise systems, supports 30+ reporting frameworks including SEC, CSRD, ISSB, and California requirements, and provides AI-driven validation to ensure accuracy before disclosure.