AI for Sustainability

SECR Reporting in 2026: Requirements, Scope, and How AI Simplifies Compliance

The 2026 guide to SECR for UK large companies and LLPs — requirements, UK SRS convergence, FRC scrutiny, and how Net0 automates SECR disclosures.

Sofia Fominova

Apr 19, 2026

TL;DR: Streamlined Energy and Carbon Reporting (SECR) is the United Kingdom's mandatory energy and greenhouse gas disclosure regime for large companies and LLPs, active since April 2019 and covering around 12,000 entities. In 2026 SECR remains in force, but the landscape is shifting: the Department for Energy Security and Net Zero (DESNZ) published its formal post-implementation evaluation on 29 January 2026, and the UK Sustainability Reporting Standards (UK SRS) S1 and S2 were finalised on 25 February 2026, with the Financial Conduct Authority consulting on mandatory compliance for listed companies from 1 January 2027. Net0, an AI infrastructure company that builds intelligent systems for governments and global enterprises, automates the full SECR data pipeline so reporters can keep pace.

Key Takeaways

SECR applies to UK-quoted companies, large unquoted companies, and large LLPs meeting two of three thresholds: 250+ employees, £36 million+ turnover, or £18 million+ balance sheet, according to the UK Government SECR guidance.

Around 12,000 UK entities now publish CO2e data through SECR, following the 2019 replacement of the Carbon Reduction Commitment Energy Efficiency Scheme.

DESNZ published its SECR post-implementation evaluation on 29 January 2026, drawing on business surveys, qualitative interviews, quasi-experimental analysis of energy meter data, and Companies House filings to inform future policy direction.

The Financial Reporting Council has signalled heightened scrutiny on boilerplate energy efficiency narratives, requiring specific and measurable actions rather than generic statements.

UK SRS S1 and S2, derived from IFRS S1 and S2, were finalised on 25 February 2026; the FCA is consulting on mandatory adoption for listed companies from 1 January 2027, meaning SECR will coexist with a broader climate disclosure regime rather than be replaced by it.

Introduction

Streamlined Energy and Carbon Reporting, or SECR, is the annual energy and carbon disclosure that every large UK-incorporated company and LLP must include in its directors' report. First introduced under the Companies (Directors' Report) and Limited Liability Partnerships (Energy and Carbon Report) Regulations 2018, SECR has been a fixture of UK compliance and reporting since April 2019. Net0 is an AI infrastructure company that builds intelligent systems for governments and global enterprises, including the data pipelines that keep SECR reporters audit-ready. This guide explains what SECR requires in 2026, where the Financial Reporting Council is raising the bar, and how the framework interacts with the newer UK SRS and the European Union's CSRD.

What SECR is and why it still matters in 2026

SECR replaced the Carbon Reduction Commitment Energy Efficiency Scheme in April 2019 and is codified in the Companies Act 2006 as amended by the 2018 regulations. Its purpose is to bring energy and carbon information into the same audited annual report investors already read for financial data, closing the gap between climate risk and financial performance.

In January 2026, DESNZ published the Streamlined Energy and Carbon Reporting (SECR) regulations: evaluation, a 112-page post-implementation review commissioned to test whether SECR is still achieving its policy aims. The evaluation combined a business survey, qualitative interviews with reporters and investors, quasi-experimental analysis of energy meter data, and Companies House accounts analysis. Its findings feed directly into the statutory post-implementation review and will shape whether SECR is retained in its current form, amended, or absorbed into the wider UK SRS architecture.

The short version for reporting teams: SECR is not going anywhere in 2026. Every large company subject to the regime must still publish the required disclosures in its directors' report, and the bar on quality is rising rather than falling.

Who must report under SECR

SECR applies to three categories of UK entity, according to the UK Government SECR guidance:

Quoted companies with equity share capital listed on a UK-recognised or EEA stock exchange, the New York Stock Exchange, or Nasdaq.

Large unquoted companies that meet at least two of three thresholds: 250 or more employees, turnover of £36 million or more, or a balance sheet total of £18 million or more.

Large Limited Liability Partnerships (LLPs) meeting the same two-of-three thresholds.

A low-energy-user exemption is available for organisations consuming 40 MWh or less of energy across the reporting period, but the exemption must still be declared in the directors' report with an explanation. This is the SECR regime's "comply or explain" principle in action: silence is not an option.

Most reporters sit in the unquoted-company bracket, which is why SECR population estimates hover around 12,000 entities. Private equity portfolio companies, subsidiaries of multinational groups, and large family-owned businesses frequently underestimate their inclusion because they assume SECR is a listed-company issue. It is not.

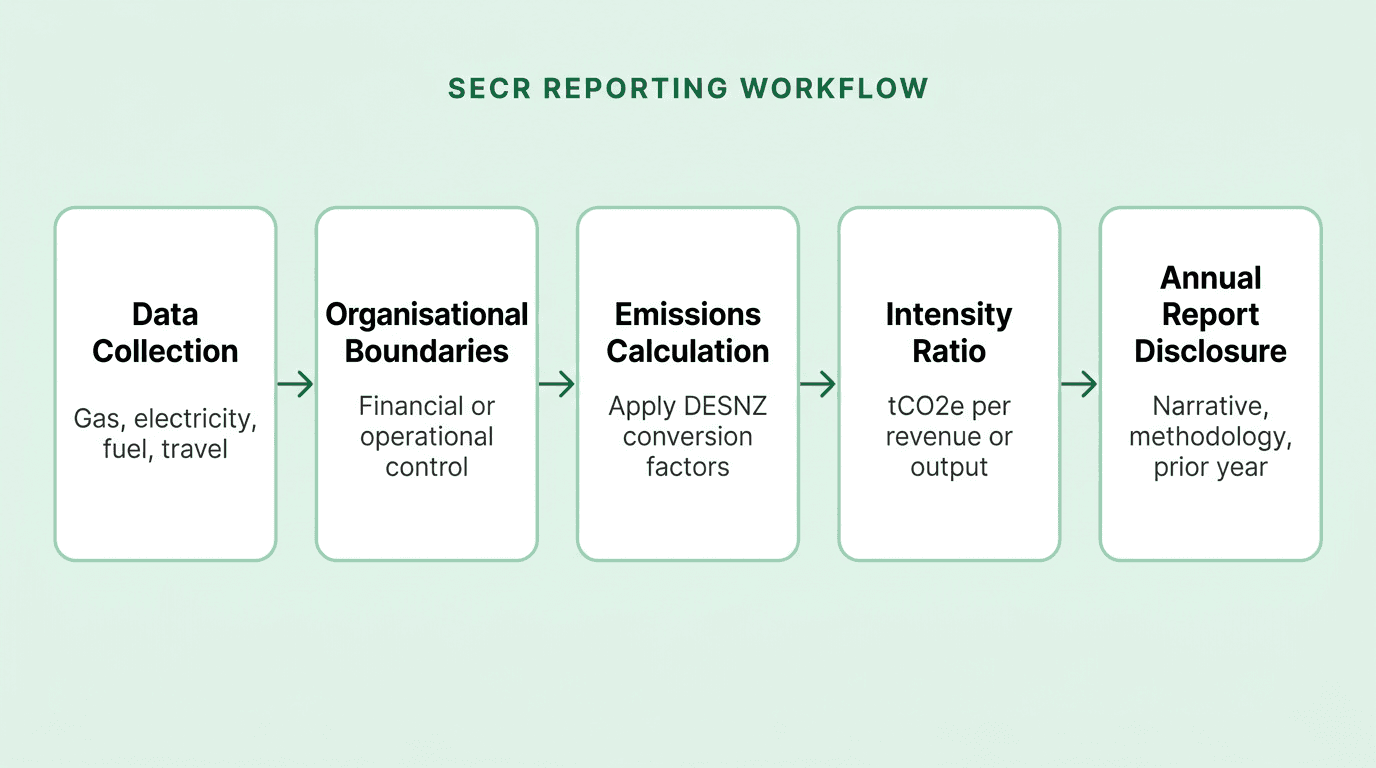

Core SECR reporting requirements

The disclosures SECR demands are deliberately prescriptive so that reporters cannot cherry-pick what to publish. For each reporting period, companies in scope must disclose:

Total UK energy consumption in kWh, covering at minimum purchased electricity, gas, and transport fuels.

Associated greenhouse gas emissions in tonnes of CO2 equivalent, calculated using a recognised standard such as the Greenhouse Gas Protocol.

At least one intensity ratio relating emissions to a quantifiable business metric such as revenue, production units, or floor area, to enable year-on-year and peer comparisons.

The methodology used to collect data and calculate emissions, including the chosen organisational boundary (financial control or operational control) and the emission factor source.

A narrative on energy efficiency actions taken during the reporting period, or an explicit statement that none were taken.

Prior-year comparatives, so the disclosure can be read as a trend rather than a snapshot.

The regime operates on a comply or explain basis. If a company omits any element, it must justify the omission in its directors' report. That narrative obligation is where the Financial Reporting Council and institutional investors now focus most of their scrutiny.

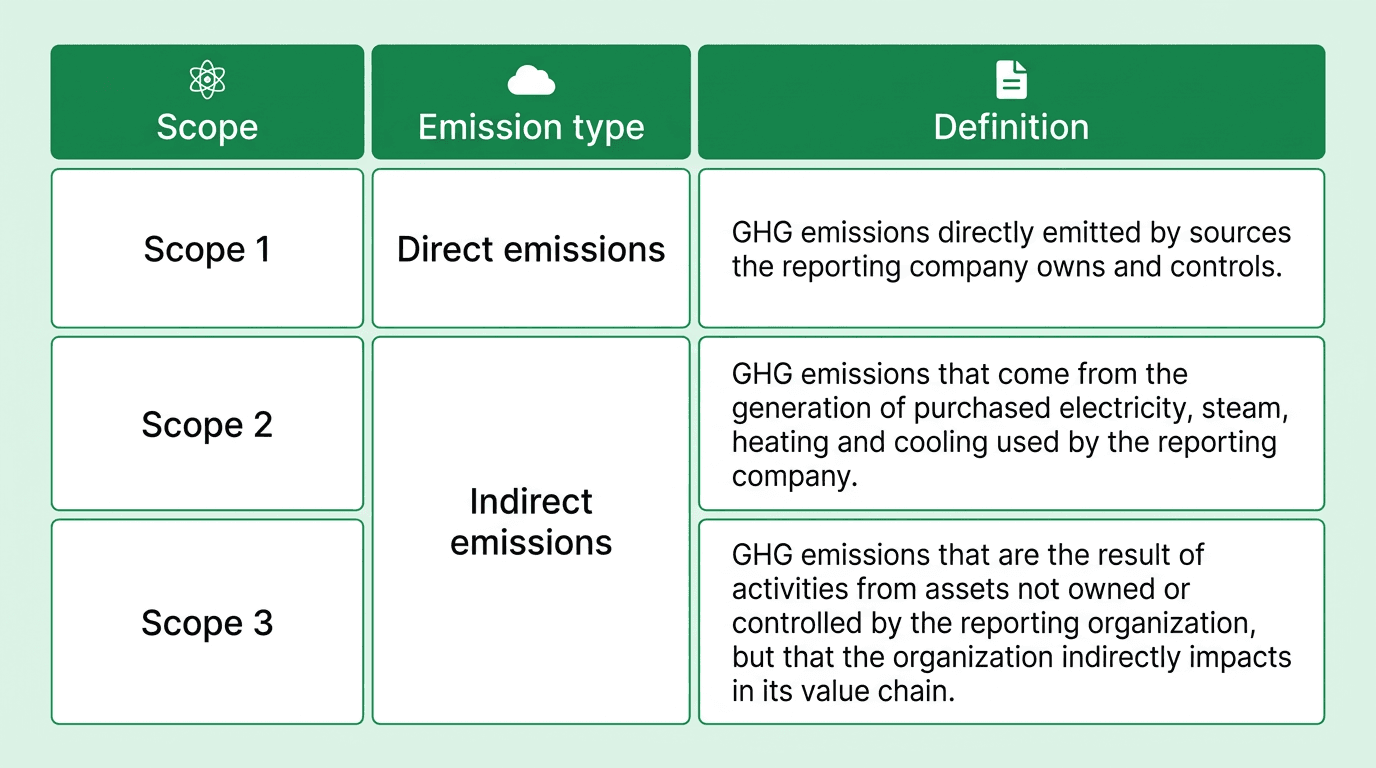

Scope 1, 2, and 3 under SECR

SECR is built on the GHG Protocol Corporate Standard and aligns with the established Scope 1, 2, and 3 framework for categorising emissions sources:

Scope 1 (required) — direct emissions from fuel combustion in owned or controlled assets, including natural gas for heating and fuel burned in company vehicles.

Scope 2 (required) — indirect emissions from purchased electricity, usually calculated on a location-based basis using grid-average emission factors published annually by DESNZ.

Scope 3 (partial, required) — at minimum, business travel in rental or employee-owned vehicles where the company pays the fuel or mileage. SECR does not require a full upstream and downstream Scope 3 inventory, but many reporters publish one anyway to align with CSRD, CDP, and SBTi expectations.

Because SECR is integrated into the audited directors' report, the organisational boundary chosen for GHG reporting must be consistent with the boundary used in the financial statements. Most reporters select financial control, but operational control is equally acceptable provided the choice is disclosed and applied consistently year on year.

Where SECR reporters commonly fail in 2026

Four failure modes account for most of the poor-quality SECR disclosures seen across FTSE-listed and large-private reporters.

Boilerplate efficiency narratives. The Financial Reporting Council has been consistent in its annual review cycles: generic statements such as "we encourage staff to switch off lights" are insufficient. Reporters are expected to describe specific initiatives, the kWh or tCO2e saved, and any capital invested. This expectation was reinforced in the FRC's Annual Review of Corporate Reporting 2024/25.

Methodology gaps. SECR requires the methodology to be set out clearly. Reporters who say only "GHG Protocol" without naming the emission factor set, the organisational boundary, or the treatment of market-based versus location-based Scope 2 routinely receive comment letters.

Scope 3 under-scoping. Business travel in employee-owned vehicles is a mandatory disclosure where the company reimburses mileage. It is also the most commonly overlooked item, particularly for professional services firms with dispersed consulting workforces.

Emission factor drift. DESNZ republishes UK GHG conversion factors every June. Consumption that is flat year-on-year can still produce changes in reported tCO2e simply because the emission factor moved. Reporters who apply prior-year factors to the current year's data introduce a compliance risk; those who do not restate prior-year figures using the current-year factors introduce a comparability risk. A well-designed data pipeline tracks both versions and documents the treatment.

The automation of data collection across source systems is the single biggest determinant of whether a reporter avoids these failure modes or runs into them every year.

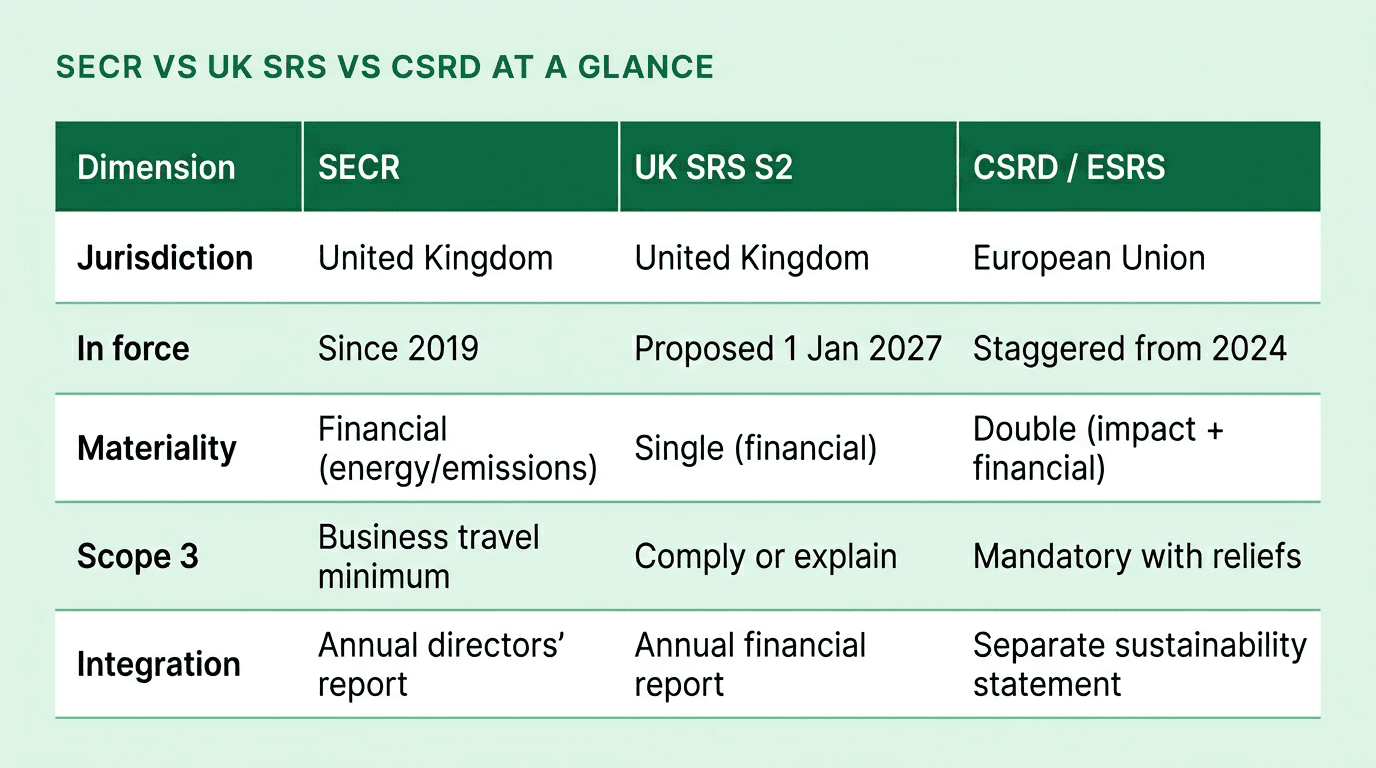

SECR in the UK SRS era: what changes from 2027

The United Kingdom is building a new climate and sustainability disclosure architecture on top of SECR rather than replacing it. On 25 February 2026, the UK Government finalised the UK Sustainability Reporting Standards, comprising UK SRS S1 (general sustainability-related financial disclosures) and UK SRS S2 (climate-related disclosures), both derived from IFRS S1 and S2 issued by the ISSB.

The Financial Conduct Authority is consulting on a requirement that UK-listed companies apply UK SRS S1 and S2 in their annual reports for financial years beginning on or after 1 January 2027. Once in force, this will sit alongside SECR rather than supersede it. SECR remains anchored in the Companies Act and applies to a broader population (including large unquoted companies); UK SRS S2 is FCA-driven and applies initially only to listed issuers.

The practical implication for reporting teams is that the underlying data pipeline needs to service both regimes simultaneously: SECR's UK-only energy and emissions view in the directors' report, and UK SRS S2's broader climate-related financial disclosure (Scope 1, 2, and 3, scenario analysis, transition plans) in the annual financial report.

Multinational reporters with UK operations and EU subsidiaries already face a third lens: the EU's CSRD, which applies European Sustainability Reporting Standards (ESRS) on a double-materiality basis. The three regimes share a common ISSB-aligned spine but differ on materiality, Scope 3 treatment, and where disclosures are integrated. Building once and mapping many is the only defensible approach.

How AI is changing SECR reporting

The original SECR guidance assumed reporters would compile spreadsheets from utility bills, fuel card statements, and travel receipts every year. That model is collapsing under the weight of data volume and the FRC's rising quality bar.

AI-native carbon accounting platforms change the economics of SECR in four ways.

Automated source-system data collection. Modern platforms ingest directly from energy management systems, building management systems, fleet telematics, ERP systems, procurement, HR travel platforms, and utility supplier APIs, eliminating manual uploads and the errors they introduce.

Emission factor version control. Applying the correct DESNZ conversion factor vintage to each reporting year, and automatically restating prior-year figures where required, is a data-engineering problem that AI systems solve natively.

Boundary resolution and double counting checks. Large groups with multiple entities, joint ventures, and landlord-tenant arrangements routinely double-count or miss emissions at the boundary. Machine learning can reconcile entity hierarchies against the consolidation used in the financial statements.

Auditable audit trails. Every number on the page of a directors' report needs to be defensible to an auditor or the FRC. AI platforms that generate lineage for every tCO2e figure — source document, emission factor, calculation method, version — make that audit effortless rather than painful. This applies equally when choosing between activity-based, production-based, and spend-based emission factors across different reporting categories.

Reporters who are also tracking decarbonization targets against SBTi validation or ESG reporting to investors benefit from the same underlying data pipeline, which is why the AI platform tends to become the system of record for multiple frameworks at once.

How Net0 supports SECR reporting

Net0 provides an AI-native sustainability platform used by global enterprises and governments to automate multi-framework climate and environmental reporting. For SECR specifically, Net0 automates the full pipeline from source-system ingestion to auditable directors' report disclosure.

10,000+ enterprise system integrations covering ERP, utility APIs, BMS, fleet telematics, HR, procurement, and finance systems, so SECR data collection is continuous rather than annual.

50,000+ emission factors with automated DESNZ version control and prior-year restatement.

30+ reporting frameworks supported, including SECR, UK SRS S1/S2, CSRD with ESRS, IFRS S1 and S2, CDP, GRI, the SEC Climate Disclosure, and SBTi validation — reported from the same audited data.

Intensity ratio benchmarking across UK and global peer groups, so the SECR intensity disclosure is defensible rather than arbitrary.

Boundary reconciliation against the financial consolidation used in the audited accounts, eliminating the most common FRC comment-letter trigger.

Full carbon accounting methodology traceability for every number on the page, down to the source document and emission factor vintage.

The Net0 platform is deployed by Fortune 500 enterprises and governments from Dubai and Monaco across four continents, with sovereign, hybrid, and cloud deployment options for UK reporters with data residency requirements.

Book a demo to see how Net0 automates SECR, UK SRS, and CSRD from a single data pipeline.

Frequently Asked Questions

What is SECR in simple terms?

SECR, or Streamlined Energy and Carbon Reporting, is the UK regime that requires large companies and LLPs to disclose their annual UK energy consumption, greenhouse gas emissions, energy efficiency actions, and an intensity ratio inside their directors' report. It has applied since 1 April 2019 and covers around 12,000 UK entities.

Who is required to report under SECR in 2026?

UK-quoted companies, large unquoted companies, and large LLPs meeting two of three thresholds (250+ employees, £36 million+ turnover, or £18 million+ balance sheet) must report. Organisations using 40 MWh or less of energy can claim the low-energy-user exemption but must still declare it in their directors' report.

What Scope 3 emissions must SECR reporters disclose?

At minimum, business travel in rental vehicles or employee-owned vehicles where the company pays for fuel or reimburses mileage. SECR does not mandate a full Scope 3 inventory, but many reporters publish one voluntarily to align with CSRD, CDP, and SBTi expectations.

Will UK SRS replace SECR?

No. UK SRS S1 and S2 were finalised on 25 February 2026, and the FCA is consulting on mandatory adoption for listed companies from 1 January 2027. UK SRS will sit alongside SECR, which remains anchored in the Companies Act and covers a broader population (including large unquoted companies).

How is SECR different from CSRD?

SECR is a UK disclosure integrated into the directors' report, focused on energy and GHG emissions with a financial-materiality lens. The EU's CSRD requires far broader double-materiality reporting under the European Sustainability Reporting Standards (ESRS), covers full Scope 3 with transitional reliefs, and applies to EU operations. Multinationals typically need to satisfy both.

What happens if a company fails to comply with SECR?

SECR disclosures are part of the directors' report, so non-compliance is a breach of the Companies Act 2006. Directors carry personal responsibility for the accuracy of the report, and the Financial Reporting Council can issue public comment letters that flag poor-quality disclosures to investors and the market. Reputational and governance consequences typically bite harder than formal penalties.

How often are the UK GHG conversion factors updated?

DESNZ republishes the UK GHG conversion factors annually, usually in June. Even if a company's energy consumption is flat year-on-year, reported tCO2e can change because the emission factor has moved. Reporters need a clear methodology for which factor vintage applies to which reporting period.