AI for Sustainability

The European Sustainability Reporting Standards (ESRS): The 12 Standards, Compliance Timeline, and Double Materiality

The ESRS establishes 12 mandatory reporting standards under the EU's Corporate Sustainability Reporting Directive. This guide covers each standard, the phased compliance timeline after Omnibus I, double materiality requirements, and how AI automates ESRS reporting.

Sofia Fominova

Apr 16, 2026

TL;DR: The European Sustainability Reporting Standards (ESRS) are 12 mandatory reporting standards developed by EFRAG under the EU's Corporate Sustainability Reporting Directive (CSRD), covering environmental, social, and governance disclosures through a double materiality approach. The Omnibus I directive (Directive EU 2026/470), in force since March 2026, raised mandatory thresholds to companies with 1,000 or more employees and EUR 450 million or more in net annual turnover. EFRAG's simplified ESRS, expected by mid-2026, reduces mandatory data points by 61 percent, from approximately 1,100 to around 430.

Key Takeaways

The ESRS framework comprises 12 standards: 2 cross-cutting, 5 environmental, 4 social, and 1 governance, each requiring disclosures aligned with the TCFD/ISSB four-pillar structure of governance, strategy, impact and risk management, and metrics and targets.

The Omnibus I directive (Directive EU 2026/470), published February 26, 2026 and in force since March 19, 2026, raised CSRD thresholds to companies with more than 1,000 employees and EUR 450 million or more in net annual turnover.

EFRAG's simplified ESRS reduces the number of mandatory data points by 61 percent, from approximately 1,100 to around 430, with adoption expected by mid-2026 for application to FY 2027 reporting.

EFRAG's 2025 "State of Play" report analyzed 656 sustainability statements and found that only 10 percent of reporting companies identified all 10 topical ESRS standards as material to their operations.

Double materiality assessment is the foundation of ESRS reporting, requiring companies to evaluate both their impact on people and the environment (impact materiality) and how sustainability issues affect financial performance (financial materiality).

Net0, an AI infrastructure company that builds intelligent systems for governments and global enterprises, works with organizations navigating the evolving European Sustainability Reporting Standards landscape. The ESRS represent the most comprehensive mandatory sustainability disclosure framework ever adopted in a major economic bloc, setting detailed requirements for how companies measure, manage, and report their environmental, social, and governance performance. As the regulatory landscape shifted significantly in early 2026 with the Omnibus I directive narrowing mandatory scope while simplifying reporting requirements, understanding the current state of ESRS is essential for companies operating in or trading with the European Union. This guide provides a complete breakdown of the ESRS framework, its compliance timeline, standard-by-standard requirements, and how organizations can operationalize reporting through technology.

The European Sustainability Reporting Standards Framework

The ESRS are the detailed technical reporting standards that operationalize the EU's Corporate Sustainability Reporting Directive. Developed by the European Financial Reporting Advisory Group (EFRAG), the standards were adopted by the European Commission via delegated act on July 31, 2023 and became effective for the first wave of reporting companies from January 1, 2024 (European Commission, 2023).

The framework covers the full spectrum of environmental, social, and governance topics across 12 individual standards, each structured around a double materiality approach. This means companies must assess and disclose both how sustainability matters affect the company financially and how the company's operations impact people and the environment. The design reflects the EU's commitment to the Paris Agreement and the European Green Deal, positioning sustainability reporting as a complement to financial reporting rather than a separate exercise.

EFRAG developed the standards through extensive public consultation, drawing on existing frameworks including the Global Reporting Initiative (GRI), the Task Force on Climate-related Financial Disclosures (TCFD), and the International Sustainability Standards Board (ISSB). The result is a framework that is interoperable with global standards while maintaining the EU's distinctive emphasis on impact materiality alongside financial materiality.

The Corporate Sustainability Reporting Directive establishes the legal mandate for sustainability reporting, while the ESRS define the technical content of those reports. For companies subject to the directive, understanding the full ESRS framework is a prerequisite for compliance. The standards also align with broader ESG reporting obligations that companies face across multiple jurisdictions.

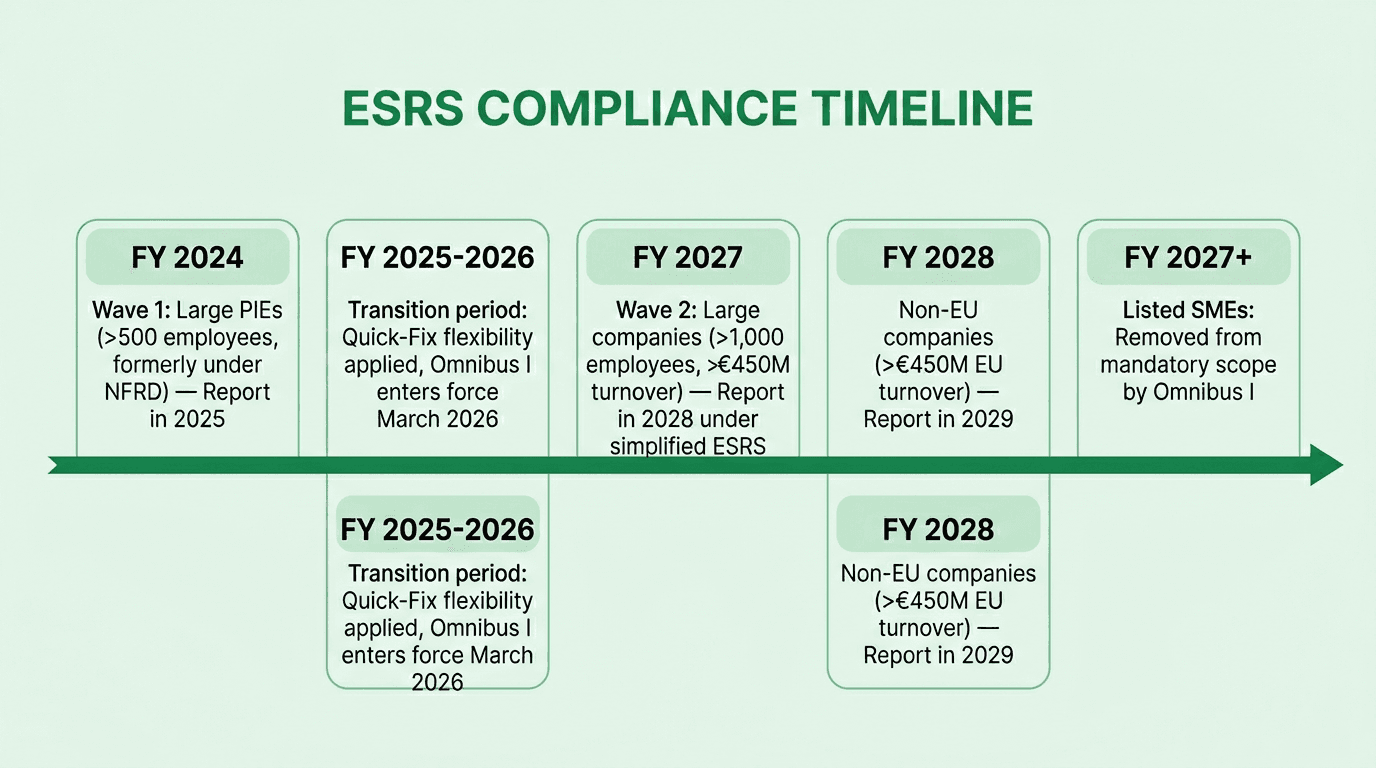

ESRS Compliance Timeline and Phased Rollout

The ESRS compliance timeline has undergone substantial revision since the original CSRD adoption. The phased rollout now reflects the Omnibus I directive's significant threshold adjustments, creating a narrower but more clearly defined scope of mandatory reporters.

Wave 1 (FY 2024, reporting in 2025): Large public-interest entities already subject to the Non-Financial Reporting Directive (NFRD) were the first companies required to apply ESRS. These approximately 1,600 companies filed their first ESRS-aligned sustainability statements in 2025 alongside their annual financial reports (European Commission, 2023).

Omnibus I (Directive EU 2026/470): Published on February 26, 2026 and entering into force on March 19, 2026, the Omnibus I directive fundamentally reshaped the CSRD's scope. The directive raised mandatory reporting thresholds from the original criteria to companies with more than 1,000 employees and EUR 450 million or more in net annual turnover (EU Council, 2026). This single change reduced the estimated number of in-scope companies from approximately 50,000 under the original CSRD to a significantly smaller cohort of large enterprises.

Wave 2 (FY 2027, reporting in 2028): Large companies meeting the new Omnibus I thresholds will begin CSRD reporting for financial year 2027, with first sustainability statements due in 2028. These companies will apply the simplified ESRS that the European Commission is expected to adopt by mid-2026.

Non-EU companies (FY 2028, reporting in 2029): Third-country companies generating more than EUR 450 million in net turnover within the EU, with at least one qualifying subsidiary or branch in the EU, must begin reporting for FY 2028.

Listed SMEs: The Omnibus I directive removed listed small and medium enterprises from mandatory CSRD scope entirely, a reversal from the original directive that had included them in a later reporting wave (EU Council, 2026).

CSDDD alignment: The Corporate Sustainability Due Diligence Directive (CSDDD) thresholds were simultaneously raised to companies with 5,000 or more employees and EUR 1.5 billion or more in net worldwide turnover, with transposition required by July 26, 2028 (Deloitte Heads Up, 2026).

EU member states must transpose the Omnibus I CSRD amendments into national law by March 19, 2027.

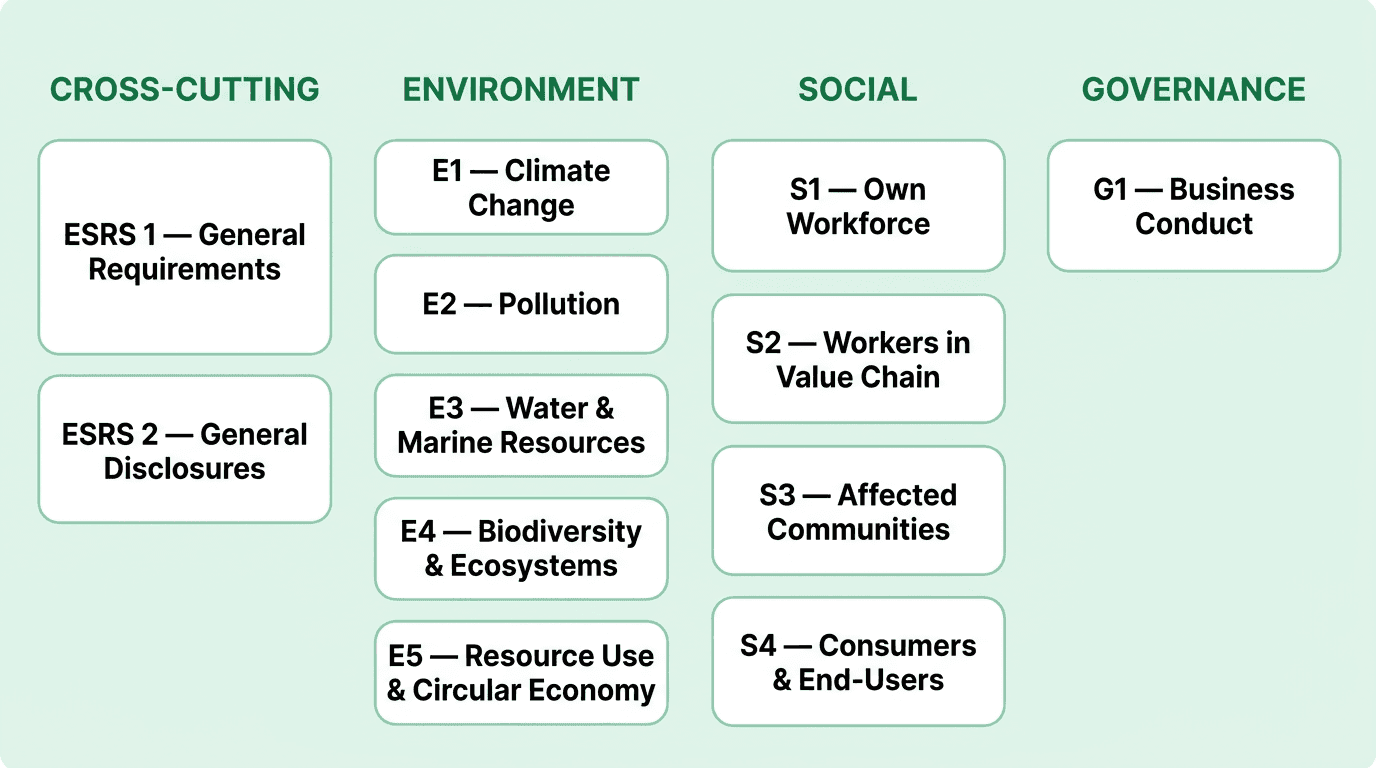

The 12 ESRS Standards Explained

The ESRS framework consists of 12 standards organized into four categories: cross-cutting, environmental, social, and governance. The two cross-cutting standards apply to all reporting companies regardless of materiality assessment outcomes, while the 10 topical standards are subject to the company's double materiality assessment. Under the simplified ESRS expected by mid-2026, all topical standards, including E1 Climate Change, become fully subject to materiality assessment rather than being presumed material (EFRAG, 2025).

The disclosure structure across all standards aligns with the TCFD and ISSB four-pillar framework: governance, strategy, impact and risk management, and metrics and targets. ESRS 2 establishes this architecture, and each topical standard follows the same logic within its specific domain.

Cross-Cutting Standards

ESRS 1 -- General Requirements: Defines the overarching principles, concepts, and architecture for ESRS reporting. It establishes the double materiality assessment methodology, value chain boundaries, time horizons (short, medium, long-term), and the basis for preparation of sustainability statements. ESRS 1 does not itself require specific disclosures but governs how all other standards are applied.

ESRS 2 -- General Disclosures: Mandatory for all companies in scope, regardless of materiality outcomes. ESRS 2 requires disclosure across four areas: governance of sustainability matters, strategy and business model, management of impacts, risks and opportunities (IROs), and metrics and targets. It includes the company's materiality assessment process and outcomes.

Environmental Standards

ESRS E1 -- Climate Change: Covers greenhouse gas emissions across Scope 1, 2, and 3, climate-related transition and physical risks, climate mitigation targets aligned with the Paris Agreement, and the company's transition plan. E1 aligns closely with IFRS S2 and the GHG Protocol reporting framework for emissions measurement methodology.

ESRS E2 -- Pollution: Addresses pollution of air, water, and soil, including substances of concern and substances of very high concern. Companies must disclose pollution prevention measures, management of incidents, and metrics on pollutant emissions.

ESRS E3 -- Water and Marine Resources: Requires disclosure on water consumption, withdrawal, and discharge, marine resource impacts, and water-related risks. Particularly relevant for companies in water-stressed regions or water-intensive industries.

ESRS E4 -- Biodiversity and Ecosystems: Covers impacts on biodiversity, ecosystem services, and land use change. Companies must disclose dependencies on ecosystem services, biodiversity-related targets, and the integration of biodiversity considerations into business decisions.

ESRS E5 -- Resource Use and Circular Economy: Addresses resource inflows, outflows, and waste, including product design for durability, recyclability, and material recovery. Companies must disclose circular economy targets and resource efficiency metrics.

Social Standards

ESRS S1 -- Own Workforce: The most data-intensive social standard, covering working conditions, equal treatment and opportunity, and other work-related rights for the company's direct employees. Requires granular metrics on workforce composition, pay gaps, training, and health and safety.

ESRS S2 -- Workers in the Value Chain: Extends social due diligence to workers in the upstream and downstream value chain, including contract workers, supply chain labor conditions, and access to grievance mechanisms.

ESRS S3 -- Affected Communities: Addresses impacts on local and indigenous communities, including land rights, access to resources, cultural heritage, and community engagement processes.

ESRS S4 -- Consumers and End-Users: Covers product safety, privacy, responsible marketing, and access to products and services for consumers and end-users.

Governance Standard

ESRS G1 -- Business Conduct: Covers corporate culture and ethics, anti-corruption and anti-bribery policies, political engagement and lobbying, supplier payment practices, and the management of relationships with business partners.

The SEC Climate Disclosure rule in the United States, while narrower in scope, shares structural similarities with ESRS E1 on climate-related financial disclosures, making multi-jurisdictional alignment feasible for companies reporting under both regimes.

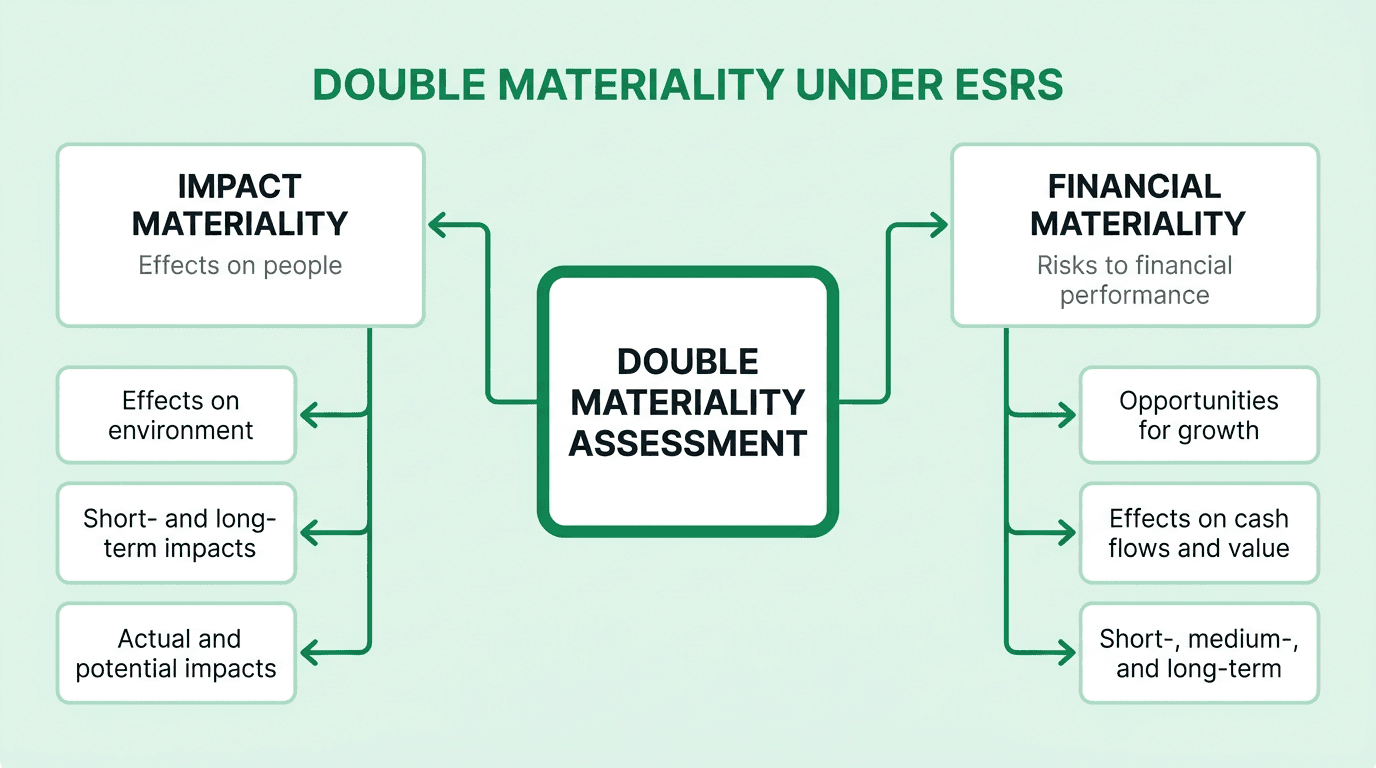

Double Materiality Under the ESRS

Double materiality is the defining methodological feature that distinguishes the ESRS from other global sustainability reporting frameworks. Where the ISSB standards focus primarily on financial materiality -- how sustainability issues affect enterprise value -- the ESRS requires companies to assess and report on both dimensions simultaneously (EFRAG, 2023).

Impact materiality evaluates how the company's operations, products, and value chain affect people and the environment. This includes direct impacts (such as factory emissions or workplace conditions) and indirect impacts mediated through business relationships. The assessment covers actual impacts already occurring and potential impacts that could materialize based on the company's activities.

Financial materiality evaluates how sustainability matters create risks or opportunities that affect the company's financial position, performance, and cash flows. This dimension aligns with the IFRS S1 definition of financial materiality, creating a bridge between ESRS and ISSB reporting. A sustainability topic is financially material if it could reasonably be expected to influence the decisions of primary users of financial statements (IFRS Foundation, 2023).

A topic is material under ESRS if it meets either the impact materiality threshold, the financial materiality threshold, or both. This dual-lens approach means that a company may need to report on topics that are not financially significant to the business but represent substantial impacts on society or the environment.

EFRAG's "State of Play 2025" report, which analyzed 656 sustainability statements from the first wave of ESRS reporters, revealed notable patterns in how companies applied double materiality. Only 10 percent of reporting companies identified all 10 topical ESRS standards as material to their operations. Meanwhile, 55 percent of the analyzed companies disclosed a climate transition plan as part of their E1 reporting (EFRAG, 2025).

The simplified ESRS introduces a streamlined materiality assessment approach. Instead of requiring companies to assess materiality at the level of individual impacts, risks, and opportunities (IROs), the simplified framework allows a top-down approach where companies assess materiality at the topic level first, then drill into specific IROs only for material topics (EFRAG, 2025). This change is expected to reduce the assessment burden significantly while preserving the integrity of the double materiality principle.

For a broader understanding of the environmental, social, and governance dimensions that underpin materiality assessments, the ESG framework overview provides foundational context.

ESRS and the CSRD: How the Two Frameworks Connect

The CSRD and the ESRS serve distinct but interdependent functions within the EU's sustainability reporting architecture. Understanding the division of responsibilities between the directive and the standards is essential for compliance planning.

The CSRD is the EU directive (legal instrument) that establishes the legal obligation for sustainability reporting. It defines which companies must report, when they must begin, where sustainability statements must be published (within the management report), and the assurance requirements for those statements. The CSRD amends the Accounting Directive (2013/34/EU) and replaced the Non-Financial Reporting Directive.

The ESRS are the technical reporting standards that specify what information companies must disclose and how it must be structured. They translate the CSRD's broad mandate into granular disclosure requirements, data points, and application guidance.

Under the original CSRD scope, the directive would have captured approximately 50,000 companies across the EU, including large companies, listed SMEs, and certain non-EU companies. The Omnibus I directive narrowed this scope substantially, focusing mandatory reporting on large companies meeting the elevated thresholds of 1,000 or more employees and EUR 450 million or more in turnover (EU Council, 2026).

EU member states are required to transpose the Omnibus I amendments to the CSRD into national legislation by March 19, 2027. The parallel CSDDD amendments, which raised due diligence thresholds to 5,000 or more employees and EUR 1.5 billion or more in turnover, must be transposed by July 26, 2028 (Gibson Dunn, 2026).

The practical implication is that companies must track both the EU-level directive timeline and their own member state's transposition progress. Companies that fall below the new Omnibus I thresholds are no longer legally required to report under CSRD, though many may choose to continue voluntary reporting to meet investor expectations, supply chain requirements, or to prepare for potential future scope expansion.

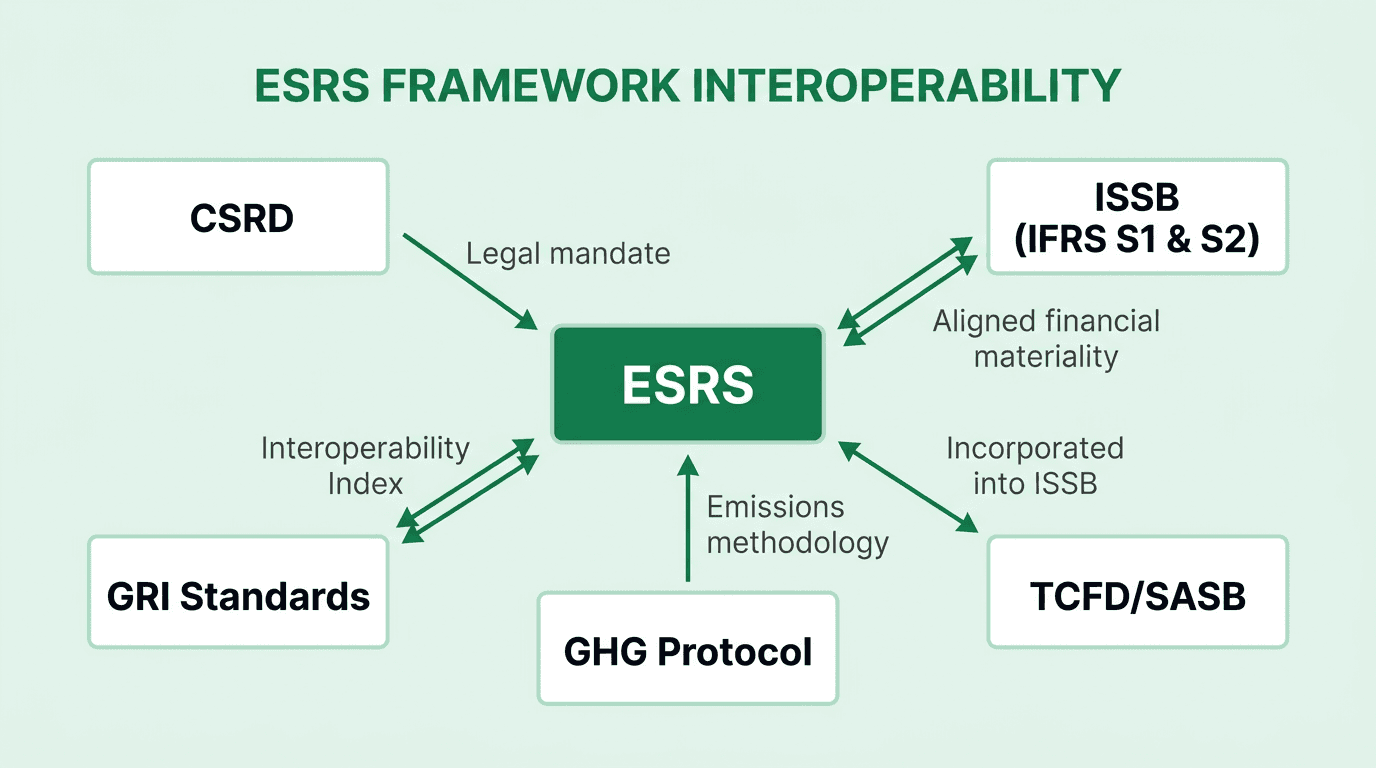

Interoperability with ISSB, GRI, and Other Global Standards

The ESRS were designed with interoperability as a core principle. EFRAG worked alongside the ISSB, GRI, and other standard-setters during the development process to minimize duplicative reporting for multinational companies operating across jurisdictions.

ESRS and ISSB alignment: The ESRS E1 (Climate Change) standard and IFRS S2 (Climate-related Disclosures) share a high degree of alignment on climate-specific disclosures, including greenhouse gas emissions metrics, scenario analysis, and transition planning. Financial materiality definitions are aligned between ESRS and IFRS S1, meaning that a topic deemed financially material under one framework will generally be material under the other. EFRAG and the ISSB published formal interoperability guidance in May 2024, enabling companies to use ISSB disclosures as a starting point and add the impact materiality layer required by ESRS (EFRAG-ISSB Interoperability Guidance, 2024).

ESRS and GRI alignment: GRI and EFRAG published the GRI-ESRS Interoperability Index in November 2024, mapping specific disclosure requirements between the two frameworks. Entities reporting under ESRS are deemed to be reporting "with reference" to GRI Standards, reducing the additional effort needed for GRI compliance. Both frameworks share an impact materiality perspective, making the alignment particularly strong on social and environmental disclosures (GRI Standards overview).

GHG Protocol foundation: The GHG Protocol provides the underlying emissions measurement methodology used by both ESRS and ISSB for Scope 1, 2, and 3 greenhouse gas emissions. Companies already reporting under the GHG Protocol can leverage their existing emissions inventories as the data foundation for ESRS E1 disclosures. The Protocol's carbon accounting methodologies remain the globally accepted standard for emissions quantification.

TCFD and SASB integration: The TCFD recommendations have been formally incorporated into the ISSB standards (IFRS S1 and S2), and the TCFD itself was disbanded in 2024 after the ISSB assumed its monitoring responsibilities. SASB industry-specific metrics are also now embedded within the ISSB framework. Companies previously reporting under TCFD or SASB can map those disclosures directly to ISSB requirements and, by extension, to the financially material dimension of ESRS.

Practical multi-framework approach: Companies subject to both ESRS and ISSB requirements can adopt a "comply and top-up" strategy: prepare ISSB-compliant disclosures to satisfy financially material sustainability topics, then add the impact materiality disclosures required by ESRS. This approach is supported by the interoperability guidance and can significantly reduce duplication. CDP reporting questionnaires have also been updated to align with both ISSB and ESRS disclosure requirements, further reducing the reporting burden for companies participating in CDP.

AI-Powered ESRS Compliance and Reporting

The complexity of ESRS reporting, with approximately 1,100 data points under the current framework and around 430 under the simplified version, has accelerated the adoption of artificial intelligence across sustainability reporting functions. According to research cited by Environmental Protection (2026), 59 percent of organizations now leverage AI for ESG measurement and reporting, based on findings from PwC and Wavestone.

AI adoption in sustainability reporting has expanded rapidly. Usage nearly tripled to 28 percent of reporting organizations in 2025, up from 11 percent in the prior year (EY Global Corporate Reporting Survey, 2025). This growth reflects both the increasing data demands of frameworks like ESRS and the maturation of AI capabilities for structured data processing.

AI automates several critical functions across the ESRS reporting workflow:

Data collection and integration: AI systems connect to enterprise resource planning (ERP) platforms, Internet of Things (IoT) sensors, supply chain management systems, and financial databases to extract, validate, and normalize sustainability data from across the organization. This eliminates the manual data gathering that traditionally consumed 60 to 70 percent of reporting timelines.

Multi-framework mapping: A single dataset can be mapped simultaneously to ESRS, GRI, ISSB, CDP, and other frameworks through AI-driven classification engines, reducing the need for separate data collection processes for each standard. This capability is particularly valuable given the interoperability between ESRS and other frameworks described above.

Emission factor matching: AI algorithms match corporate activity data to relevant emission factors from databases containing 50,000 or more factors, accounting for geographic, temporal, and methodological variations. This automated matching is essential for accurate carbon accounting across Scope 1, 2, and 3 emissions.

Materiality assessment automation: AI can analyze stakeholder inputs, industry benchmarks, peer disclosures, and regulatory requirements to support the double materiality assessment process, identifying potentially material topics and flagging gaps in coverage.

Gap analysis and compliance checking: AI tools compare existing disclosures against the full set of ESRS requirements, identifying missing data points, incomplete narratives, and areas where additional evidence is needed before filing.

Technology-enabled reporting can reduce total reporting timelines by 60 to 70 percent compared to manual processes, based on documented efficiency gains from automated data collection implementations. However, verification remains essential: only 27 percent of organizations review all AI-generated ESG content before publication, according to EY's 2025 survey, underscoring the need for robust human oversight in AI-assisted reporting workflows.

Alignment with science-based target-setting frameworks such as the Science Based Targets initiative further strengthens the credibility of AI-generated emissions data and transition plans disclosed under ESRS E1.

Net0 AI-Powered Sustainability Platform

Net0, an AI infrastructure company that builds intelligent systems for governments and global enterprises, provides an AI-powered sustainability platform purpose-built for the complexity of multi-framework regulatory reporting including ESRS and CSRD compliance.

The platform integrates with more than 10,000 enterprise systems, enabling automated data collection from ERP platforms, IoT devices, supply chain databases, financial systems, and operational technology. This integration infrastructure supports reporting across 30 or more frameworks, including ESRS, CSRD, GHG Protocol, CDP, GRI, ISSB, and SBTi, from a single unified dataset. Net0's emission factor database contains more than 50,000 factors with geographic and temporal granularity, ensuring accurate Scope 1, 2, and 3 emissions calculations.

Core capabilities relevant to ESRS compliance include comprehensive Scope 1, 2, and 3 emissions tracking, multi-framework report generation that maps disclosures to ESRS requirements alongside parallel frameworks, AI-driven data validation that flags anomalies and inconsistencies before submission, scenario simulation for testing decarbonization pathways and transition plans, and Marginal Abatement Cost Curve (MACC) analysis for prioritizing emission reduction initiatives based on cost-effectiveness.

Net0 offers sovereign and hybrid deployment options for governments and regulated enterprises that require data residency controls and on-premise infrastructure. This deployment flexibility is critical for organizations in jurisdictions with strict data sovereignty requirements.

The platform currently serves more than 400 entities across four continents, spanning Fortune 500 corporations, national governments, and large regulated enterprises navigating ESRS, CSRD, and other mandatory sustainability reporting obligations.

Book a demo to see how Net0 automates ESRS compliance across multiple reporting frameworks.

Frequently Asked Questions

What are the European Sustainability Reporting Standards?

The ESRS are 12 mandatory reporting standards developed by EFRAG under the EU's Corporate Sustainability Reporting Directive. They provide a detailed framework for disclosing environmental, social, and governance data using a double materiality approach that covers both impact on people and environment and financial risks to the company.

How many ESRS standards are there?

There are 12 ESRS standards: 2 cross-cutting standards (ESRS 1 General Requirements, ESRS 2 General Disclosures), 5 environmental standards (E1-E5), 4 social standards (S1-S4), and 1 governance standard (G1 Business Conduct).

Who must comply with ESRS reporting requirements?

Following the Omnibus I directive (March 2026), mandatory ESRS reporting applies to EU companies with more than 1,000 employees and EUR 450 million or more in net annual turnover. Non-EU companies with EUR 450 million or more in EU turnover and qualifying subsidiaries must also comply.

What is double materiality under the ESRS?

Double materiality requires companies to assess and report on two dimensions: impact materiality (how the company affects people and the environment) and financial materiality (how sustainability issues affect the company's financial performance). This dual lens distinguishes ESRS from investor-focused frameworks like ISSB.

How did the Omnibus I directive change ESRS requirements?

The Omnibus I directive (EU 2026/470), in force since March 2026, raised CSRD thresholds from the original scope to 1,000 or more employees and EUR 450 million or more in turnover. It removed listed SMEs from mandatory scope and tasked the European Commission with adopting simplified ESRS by mid-2026.

How does AI automate ESRS compliance?

AI automates ESRS compliance by collecting data from thousands of enterprise systems, mapping disclosures across multiple frameworks simultaneously, matching activity data to emission factors, performing gap analysis against ESRS requirements, and generating audit-ready reports. According to PwC research, 59 percent of organizations now use AI for ESG measurement.

What is the relationship between ESRS and ISSB standards?

ESRS and ISSB standards share aligned financial materiality definitions and high interoperability on climate disclosures. ESRS applies double materiality (impact and financial) while ISSB focuses on financial materiality. Formal interoperability guidance published in May 2024 enables companies to comply with both frameworks efficiently.