AI for Sustainability

EU CBAM in 2026: Definitive Regime, Omnibus Simplification, and First Certificate Price

The EU Carbon Border Adjustment Mechanism (CBAM) entered its definitive regime on 1 January 2026. Here is what importers need to know about the Omnibus Simplification Package, the €75.36 first certificate price, and the 2028 scope extension.

Sofia Fominova

Apr 17, 2026

TL;DR

The EU Carbon Border Adjustment Mechanism (CBAM) entered its definitive regime on 1 January 2026, making financial liability real for importers of cement, iron and steel, aluminium, fertilisers, electricity, and hydrogen entering the European Union. The October 2025 Omnibus Simplification Package introduced a 50-tonne de minimis exemption, postponed certificate sales to 1 February 2027, and cut the quarterly holding requirement from 80% to 50%. The first CBAM certificate price, published by the European Commission on 7 April 2026, was set at €75.36 per tonne of CO₂e.

Key Takeaways

Definitive regime active: CBAM financial obligations apply to all imports from 1 January 2026, with the first annual declaration and certificate surrender due by 30 September 2027.

Scope unchanged for 2026: Cement, iron and steel, aluminium, fertilisers, electricity, and hydrogen remain the six covered sectors. A proposal adopted in December 2025 would extend CBAM to around 180 downstream steel and aluminium products from 1 January 2028.

Omnibus simplification: A 50-tonne annual mass threshold exempts approximately 90% of importers while preserving 99% of covered emissions.

First certificate price: €75.36 per tonne of CO₂e for Q1 2026, published by the European Commission on 7 April 2026, tracking the EU Emissions Trading System (EU ETS) auction average.

Action required by 31 March 2026: Importers above the threshold must apply for Authorised CBAM Declarant status; those who file by that date can continue importing while the application is processed.

Introduction

Net0 is an AI infrastructure company that builds AI solutions for governments and global enterprises, with a dedicated AI-powered sustainability platform used by Fortune 500 companies and national regulators to manage CBAM, emissions, and multi-framework sustainability reporting. The EU Carbon Border Adjustment Mechanism is now one of the most consequential pieces of climate policy in the world: as of 2026 it prices carbon on physical goods crossing the EU border, and the compliance cost is no longer theoretical.

This article explains what CBAM is in 2026, how the definitive regime works, what the Omnibus Simplification Package changed, the first official certificate price, the proposed 2028 scope extension, and what importers and exporters need to do now. It also summarises how Net0's platform supports verified CBAM reporting across 30+ sustainability frameworks.

What the EU Carbon Border Adjustment Mechanism Is

The Carbon Border Adjustment Mechanism is an EU tool that places a carbon price on imports of selected goods, equal to the price paid by EU producers under the EU Emissions Trading System. Its purpose is to prevent carbon leakage — the shift of production to jurisdictions with weaker climate rules — and to ensure that imported goods face the same carbon cost as goods made inside the European Union. CBAM was created under the EU's Fit for 55 package, which aims to cut net greenhouse gas emissions by at least 55% by 2030 on the path to climate neutrality by 2050.

Carbon leakage inflates a company's Scope 3 emissions by relocating production rather than reducing it, and it erodes the price signal that the EU ETS is designed to create. By applying an equivalent charge at the border, CBAM closes that loophole and encourages foreign producers to invest in cleaner processes.

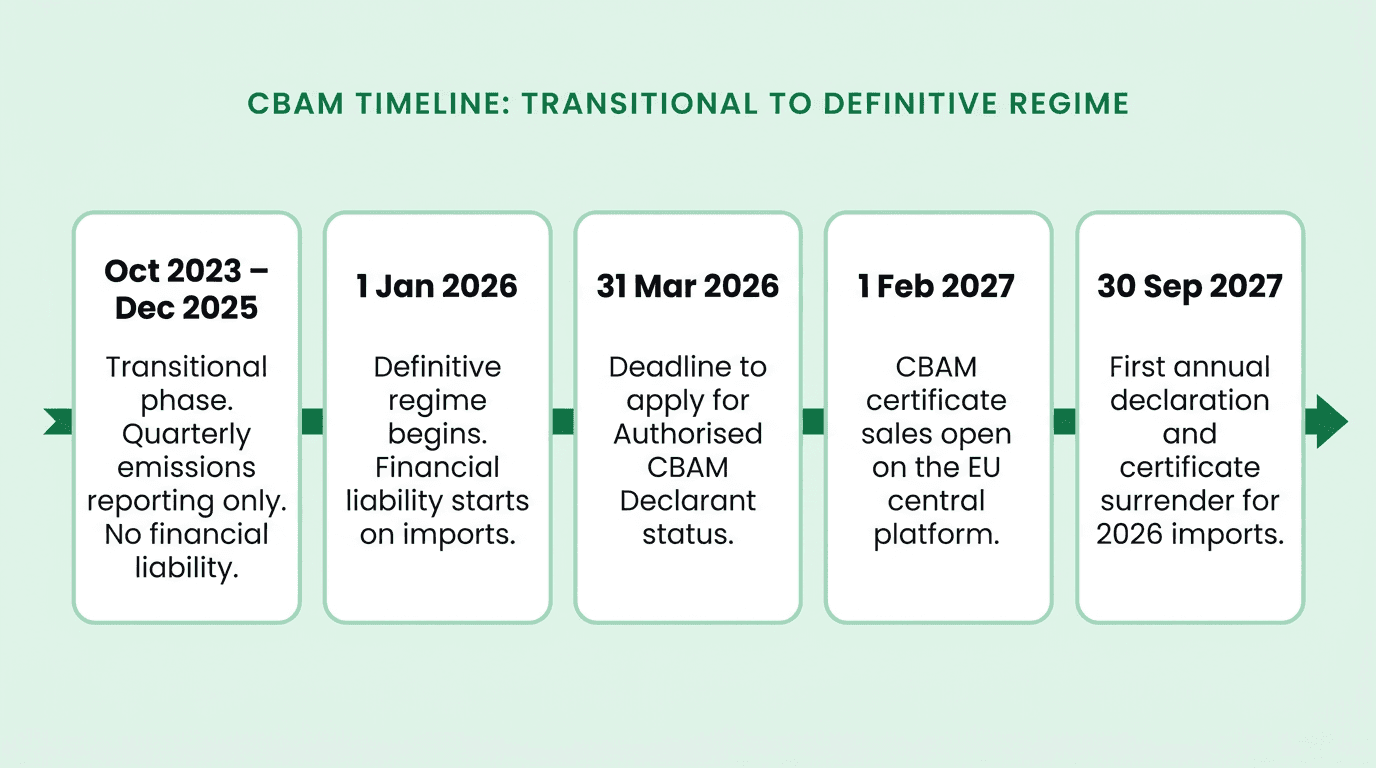

CBAM Entered Its Definitive Regime on 1 January 2026

CBAM has two phases. The transitional phase ran from 1 October 2023 to 31 December 2025 and required quarterly emissions reporting with no financial obligation. The definitive regime began on 1 January 2026, and the European Commission confirmed on 14 January 2026 that the system had entered into force successfully across all member states (European Commission, Directorate-General for Taxation and Customs Union).

From 1 January 2026, imports of covered goods into the EU generate financial liability. Importers no longer file quarterly reports; instead, they prepare for a single annual CBAM declaration. The last transitional quarterly report was due by 31 January 2026.

Key 2026 and 2027 Dates

1 January 2026 — Definitive regime begins. Imports generate financial liability.

31 January 2026 — Deadline for the final transitional quarterly report (covering Q4 2025).

31 March 2026 — Deadline to apply for Authorised CBAM Declarant status; filing by this date allows continued importing while the application is processed.

7 April 2026 — European Commission published the first CBAM certificate price: €75.36 per tonne of CO₂e for Q1 2026.

1 February 2027 — CBAM certificate sales open on the EU central platform.

30 September 2027 — First annual CBAM declaration and certificate surrender, covering all 2026 imports.

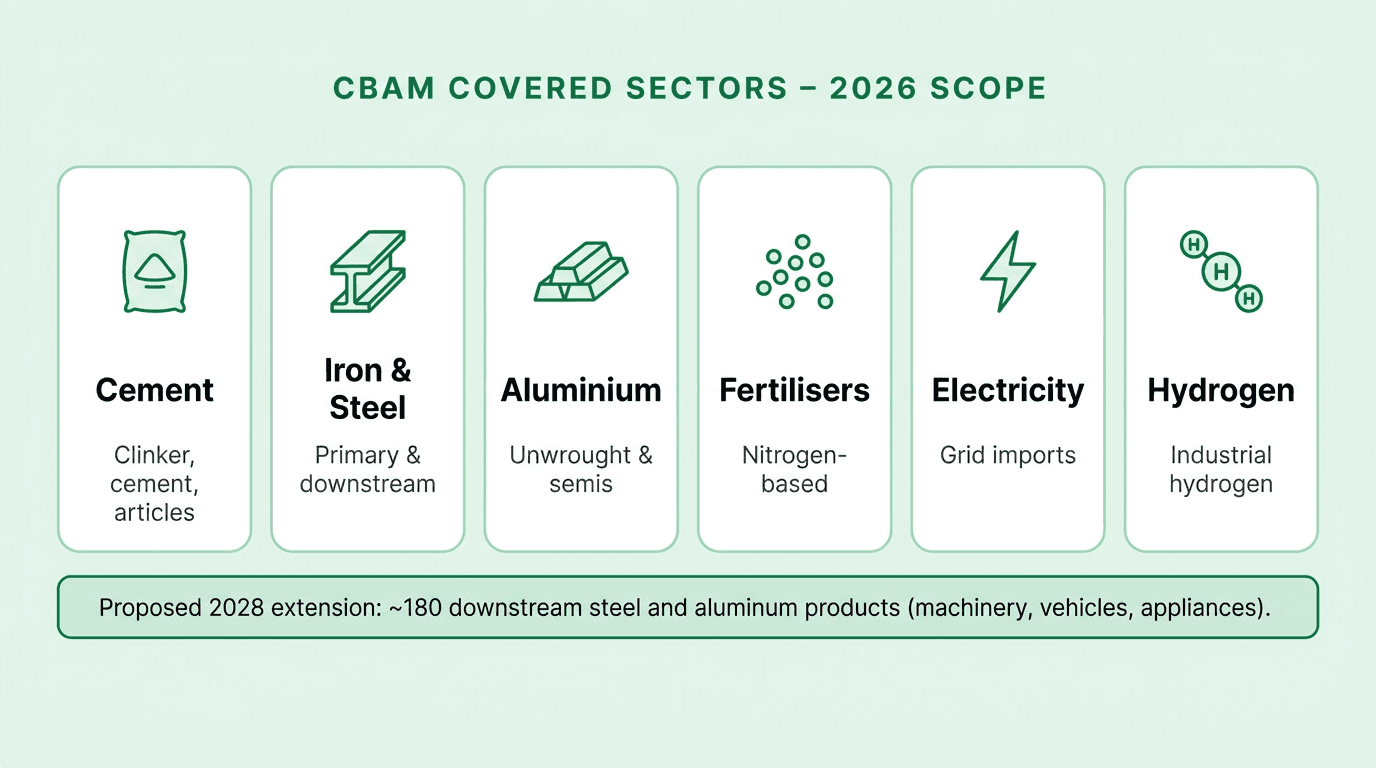

Sectors Covered by CBAM in 2026

CBAM in 2026 covers six carbon-intensive sectors chosen for their high emissions intensity and their documented exposure to carbon leakage: cement, iron and steel, aluminium, fertilisers, electricity, and hydrogen. Together these sectors represent the most significant share of industrial emissions among goods typically imported into the EU from jurisdictions without equivalent carbon pricing.

Electricity imports are included where a third country is not integrated into the EU internal electricity market; this will change over time as markets integrate. Members of the European Free Trade Association — Iceland, Liechtenstein, Norway, and Switzerland — are exempt from CBAM because they already participate in the EU ETS.

Proposed 2028 Scope Extension to 180 Downstream Products

On 17 December 2025 the European Commission adopted a legislative proposal to extend CBAM to around 180 downstream steel- and aluminium-intensive products from 1 January 2028 (European Commission press release, December 2025). The proposed additions include industrial machinery, elevators, cargo vehicles, gearboxes, wheels, white goods such as washing machines and refrigerators, metal furniture, and prefabricated buildings. The Commission has signalled further reviews covering chemicals, polymers, refineries, glass, ceramics, and pulp and paper, with the stated long-term aim of aligning CBAM coverage with the full scope of the EU ETS.

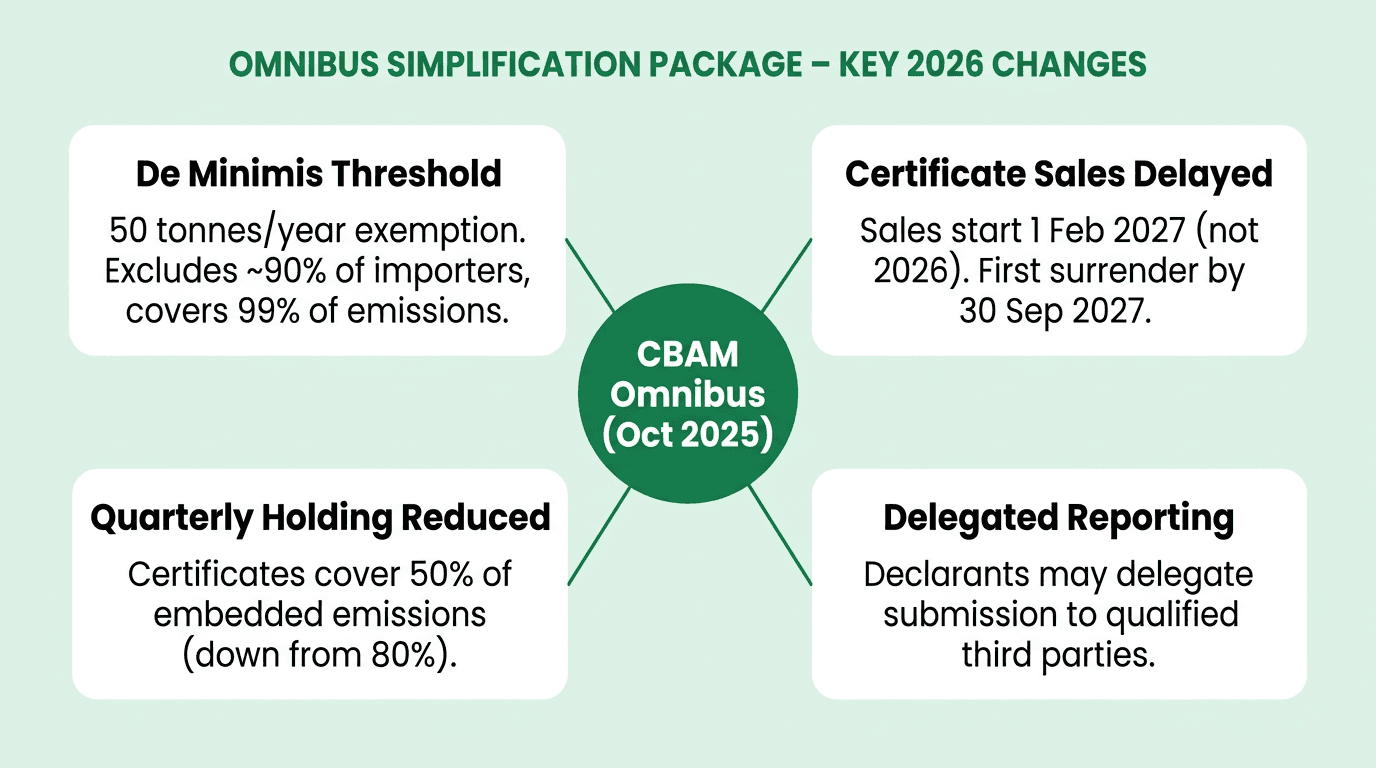

The Omnibus Simplification Package: What Changed for 2026

In response to industry feedback during the transitional phase, the EU adopted the CBAM Omnibus Simplification Package — formally Regulation (EU) 2025/2083 — which entered into force on 20 October 2025. The package reshapes how compliance works in the first years of the definitive regime without changing the fundamental carbon price.

1. A 50-Tonne De Minimis Exemption

A single mass-based threshold now exempts importers bringing in 50 tonnes or less of covered goods per calendar year. According to the International Carbon Action Partnership (October 2025 analysis), this threshold removes approximately 90% of importers from compliance scope while still capturing 99% of embedded emissions. The exemption does not apply to electricity or hydrogen, which remain covered regardless of volume.

2. Certificate Sales Delayed to 1 February 2027

Although financial liability begins with imports made on or after 1 January 2026, the physical sale of CBAM certificates is postponed to 1 February 2027. Certificates for 2026 imports will be purchased retroactively in 2027, based on the published quarterly average EU ETS price for the relevant period.

3. First Annual Declaration Moved to 30 September 2027

The annual CBAM declaration deadline moved from 31 May to 30 September of the year following import. The first declaration, covering all 2026 imports, is therefore due by 30 September 2027.

4. Quarterly Holding Requirement Cut from 80% to 50%

From 2027 onward, authorised declarants must hold CBAM certificates covering at least 50% of embedded emissions of goods imported year-to-date at the end of each quarter. The previous 80% requirement was identified by industry as a material working-capital burden.

5. Delegated Submission

Authorised CBAM declarants may now delegate the submission of declarations to qualified third parties such as customs agents or consultants, though the declarant remains legally responsible.

6. Methodology Alignment with EU ETS

Finishing processes for certain steel and aluminium goods are excluded from embedded emission calculations to align with EU ETS rules, and importers may claim deductions for carbon prices already paid in third countries — including countries other than the country of origin — provided evidence is submitted.

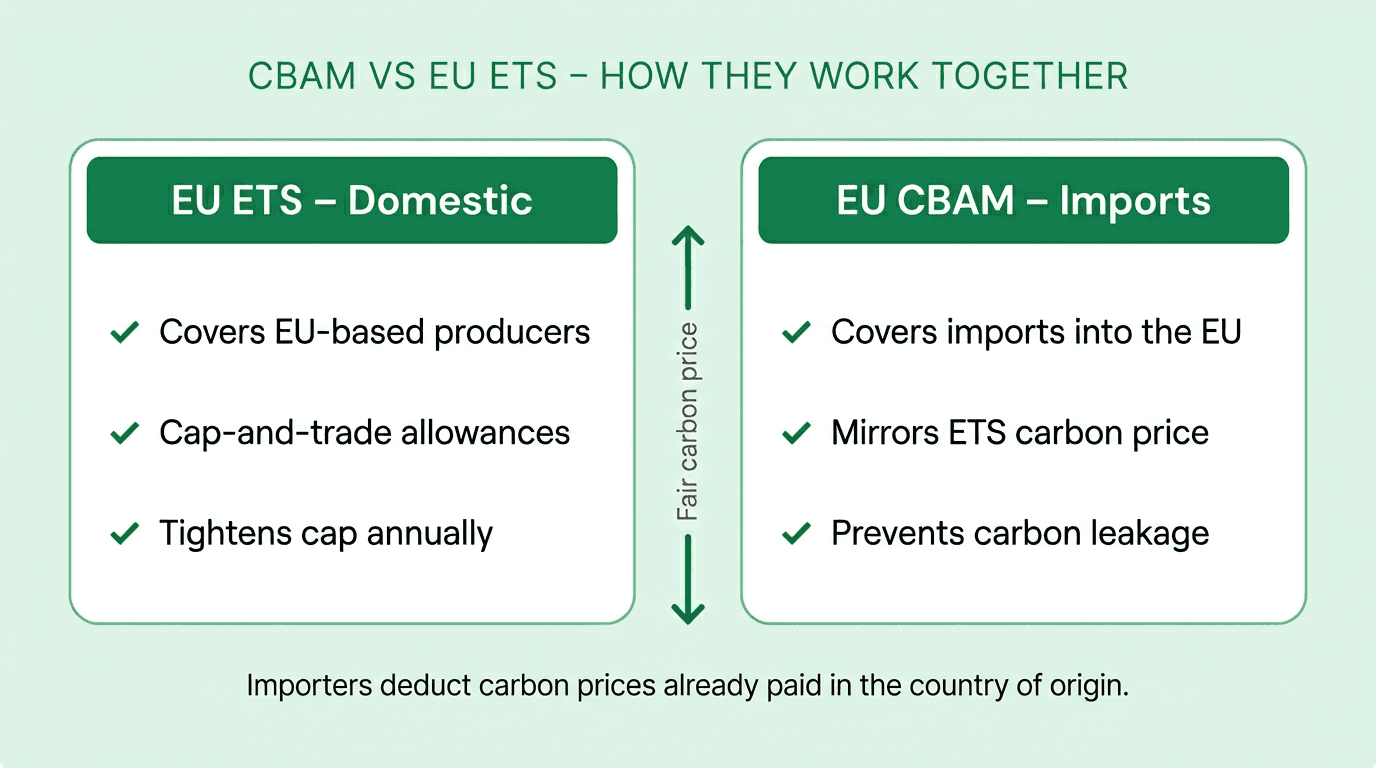

How CBAM and the EU ETS Work Together

CBAM is often described as the import-side complement to the EU ETS. The ETS runs a cap-and-trade system for EU-based installations: a fixed number of emissions allowances are issued each year, the cap tightens annually, and allowances are traded on an open market. CBAM mirrors that price for imports of covered goods, so foreign producers do not get a de facto subsidy by avoiding the ETS price.

The two systems are linked in pricing: CBAM certificate prices are calculated quarterly as the volume-weighted average of EU ETS auction clearing prices. As free allowances are phased out of the ETS for CBAM-covered sectors, the CBAM obligation rises correspondingly. For a fuller primer on how carbon pricing mechanisms fit into corporate carbon accounting, see Net0's analysis of global carbon pricing regimes.

The First CBAM Certificate Price: €75.36 per Tonne

On 7 April 2026 the European Commission's Directorate-General for Taxation and Customs Union published the first CBAM certificate price at €75.36 per tonne of CO₂e for the first quarter of 2026. The figure was calculated as the weighted average of EU ETS auction clearing prices across Q1 2026 and is the reference price importers will use when settling 2026 obligations in 2027.

This first price sets a concrete benchmark for modelling CBAM exposure. For a shipment of 10,000 tonnes of imported steel with an embedded intensity of 2.0 tonnes CO₂e per tonne of product, the indicative 2026 liability at the Q1 price would be approximately €1.51 million before any carbon price deductions — a figure that is material to margin, product pricing, and sourcing decisions for any sizeable importer.

Embedded Emissions: Default Values vs Verified Data

During 2026 importers can use either verified actual emissions data from their suppliers or default values set by the European Commission. Default values are calibrated to the average emissions intensity of the exporting country and, where that is unavailable, to the ten highest-emitting countries globally.

Default values are designed to be conservative. Analysis from major compliance advisors including EY and KPMG has consistently shown that default values typically produce higher calculated liabilities than verified actual data for low-carbon producers, creating a direct financial incentive for importers to work with suppliers on verified emissions measurement. Companies sourcing from efficient overseas producers — such as low-carbon steel mills or green hydrogen facilities — will see meaningfully lower CBAM bills by switching from defaults to verified values.

Who CBAM Affects

CBAM applies to:

EU importers of covered goods from outside the EU customs territory.

Non-EU producers and exporters whose products are sold into the EU, because EU customers now ask for verified emissions data as a condition of purchase.

Global supply chains for cement, steel, aluminium, fertilisers, electricity, and hydrogen — and from 2028, downstream manufactured goods such as machinery, vehicles, and appliances.

It does not apply to imports from EFTA members that participate in the EU ETS (Iceland, Liechtenstein, Norway, Switzerland) or to imports from Northern Ireland under the Windsor Framework for certain product categories.

For exporters in regions such as the United States, China, India, Turkey, and the Gulf, CBAM is effectively an indirect carbon price on EU-bound trade. It is already reshaping procurement decisions across steel, aluminium, and cement markets, and research from the International Institute for Sustainable Development (IISD, 2025) indicates that CBAM is prompting at least a dozen non-EU jurisdictions to consider or accelerate domestic carbon pricing to retain the deductibility benefit.

Why CBAM Still Matters in 2026

Some observers expected the Omnibus package to dilute CBAM. It did not. The fundamentals — pricing, sectors, and EU ETS linkage — remain intact, and the compliance phase is now active. Three reasons explain why CBAM matters more in 2026 than during the transitional phase:

The price is no longer zero. Every tonne of covered goods imported after 1 January 2026 generates a real, quantified liability at €75.36 per tCO₂e for Q1 2026.

Data quality is a financial variable. Default values are punitive for efficient producers; verified supplier data is the difference between a competitive and an uncompetitive EU price.

Scope is widening, not narrowing. The December 2025 proposal to cover around 180 downstream products from 2028, combined with reviews of chemicals, polymers, glass, and paper, signals that CBAM will eventually mirror the full reach of the EU ETS.

Related reading from Net0's research:

How Net0 Supports CBAM Compliance

Net0 provides an AI-powered sustainability platform built specifically for institutional-scale carbon and compliance workloads. For CBAM, Net0 combines 10,000+ system integrations, 50,000+ emission factors, and support for 30+ sustainability reporting frameworks — including CBAM, CSRD and ESRS, the GHG Protocol, CDP, GRI, IFRS S1 and S2, and the SBTi.

Net0's CBAM module automates:

Product-level embedded emissions calculations using primary supplier data where available and conservative default values only where it is not.

Authorised CBAM Declarant workflow support, including document management, customs agent delegation, and declaration drafting.

Quarterly liability forecasting against the published CBAM certificate price, with scenario modelling for product mix and supplier choice.

Carbon price deduction evidence for third-country carbon prices paid, mapped to the specific evidentiary standards required by EU customs authorities.

Audit-grade traceability across suppliers, facilities, and products, aligned with EU ETS methodology and the CBAM implementing acts.

Beyond sustainability, Net0 also operates across government AI transformation, AI infrastructure, and business AI solutions, giving enterprises and regulators a single AI-first partner rather than a siloed compliance vendor. The same platform used for CBAM can extend to CSRD filings, CDP disclosures, SBTi target tracking, and supplier engagement programmes — with full sovereign and hybrid deployment options for institutions that require data to remain in jurisdiction.

Book a demo to see how Net0 automates CBAM calculation, reporting, and certificate management in 2026.

Frequently Asked Questions

When did the EU CBAM definitive regime begin?

The CBAM definitive regime entered into force on 1 January 2026. The European Commission confirmed successful entry into force on 14 January 2026. Imports of covered goods from that date generate financial liability, with the first annual declaration and certificate surrender due by 30 September 2027.

What was the first CBAM certificate price?

The first CBAM certificate price was €75.36 per tonne of CO₂e for the first quarter of 2026, published by the European Commission on 7 April 2026. The price is calculated as the volume-weighted average of EU ETS auction clearing prices over the quarter and is published on a dedicated European Commission page.

Which sectors does CBAM cover in 2026?

CBAM covers six sectors in 2026: cement, iron and steel, aluminium, fertilisers, electricity, and hydrogen. A Commission proposal adopted on 17 December 2025 would extend coverage to around 180 downstream steel and aluminium products — including machinery, vehicles, and appliances — from 1 January 2028.

What is the CBAM de minimis exemption?

The Omnibus Simplification Package (Regulation (EU) 2025/2083) introduced a single mass-based de minimis threshold of 50 tonnes of covered goods per calendar year per importer. Importers below this threshold are exempt from CBAM obligations. The exemption covers approximately 90% of importers while retaining 99% of embedded emissions. It does not apply to electricity or hydrogen.

When do importers actually pay for CBAM certificates?

CBAM certificate sales on the EU central platform begin on 1 February 2027. Certificates for 2026 imports are purchased retroactively in 2027 at the published quarterly average EU ETS price. From 2027 onwards, authorised declarants must hold certificates covering at least 50% of embedded emissions at the end of each quarter.

Who needs to become an Authorised CBAM Declarant?

Any importer exceeding the 50-tonne annual threshold for covered goods must hold Authorised CBAM Declarant status to import into the EU. Importers who apply by 31 March 2026 can continue importing while their application is processed. Without this status, goods may be stopped at the EU border.

How does CBAM interact with the EU ETS?

CBAM mirrors the EU ETS carbon price for imports, preventing carbon leakage that would otherwise result from EU producers paying a carbon price that their foreign competitors avoid. CBAM certificate prices track the weighted average of EU ETS auction clearing prices. As free ETS allowances are phased out for CBAM sectors, the CBAM obligation rises to match.

Can importers deduct carbon prices already paid in the country of origin?

Yes. Importers can deduct effective carbon prices already paid on the embedded emissions of imported goods, including prices paid in countries other than the country of origin, provided supporting evidence is submitted with the annual declaration. This deductibility is a core reason CBAM is prompting non-EU jurisdictions to consider or accelerate domestic carbon pricing.