Compliance & Reporting

Corporate Sustainability Reporting Directive (CSRD) 2024: Who and What Is Impacted

The most straight-forward and up-to-date knowledge about CSRD reporting in 2024.

Sofia Fominova

Apr 30, 2024

In November 2022, the European Commission implemented the Corporate Sustainability Reporting Directive (CSRD), affecting nearly 50,000 companies within the European Union by establishing norms for disclosing their climate and environmental impacts. While the CSRD is a directive within the EU, its influence extends to U.S. parent companies with EU operations, necessitating adjustments in reporting for both the parent and its EU subsidiaries. This directive enhances the prior Non-Financial Reporting Directive (NFRD) by imposing more stringent reporting criteria and widening the scope of businesses that must adhere. With the growing emphasis on ESG reporting and compliance with ESG standards, numerous organizations are proactively enhancing their sustainability efforts in preparation for these upcoming requirements.

The directive is beginning to take effect in 2024, marking the start of the reporting phase for affected companies. This article aims to outline the CSRD, highlighting the latest updates and developments that businesses need to be aware of. Readers will obtain a deeper insight into the evolving landscape of corporate governance and sustainability practices, along with actionable advice for navigating these changes effectively. Additionally, we've prepared a CSRD Compliance Checklist to help kickstart your compliance journey.

Why was the CSRD adopted?

Its purpose is to foster a shift towards a sustainable and low-emission economy by mandating that companies disclose their sustainability practices in a detailed and uniform way. The CSRD stands as a pivotal mechanism in realizing the EU's environmental aspirations, including the goal to achieve carbon neutrality by the year 2050.

The EU commission recognizes that investors must have a clear understanding with valuable data and metrics of their potential investees and now this includes climate-related, environmental, social, and governance topics in depth. The CSRD is now the EU’s legislative mechanism that will not only catalyze the urge to move into the green economy, but will also replace the gaps of sustainability reporting with transparency for stakeholders.

The CSRD reporting timeline

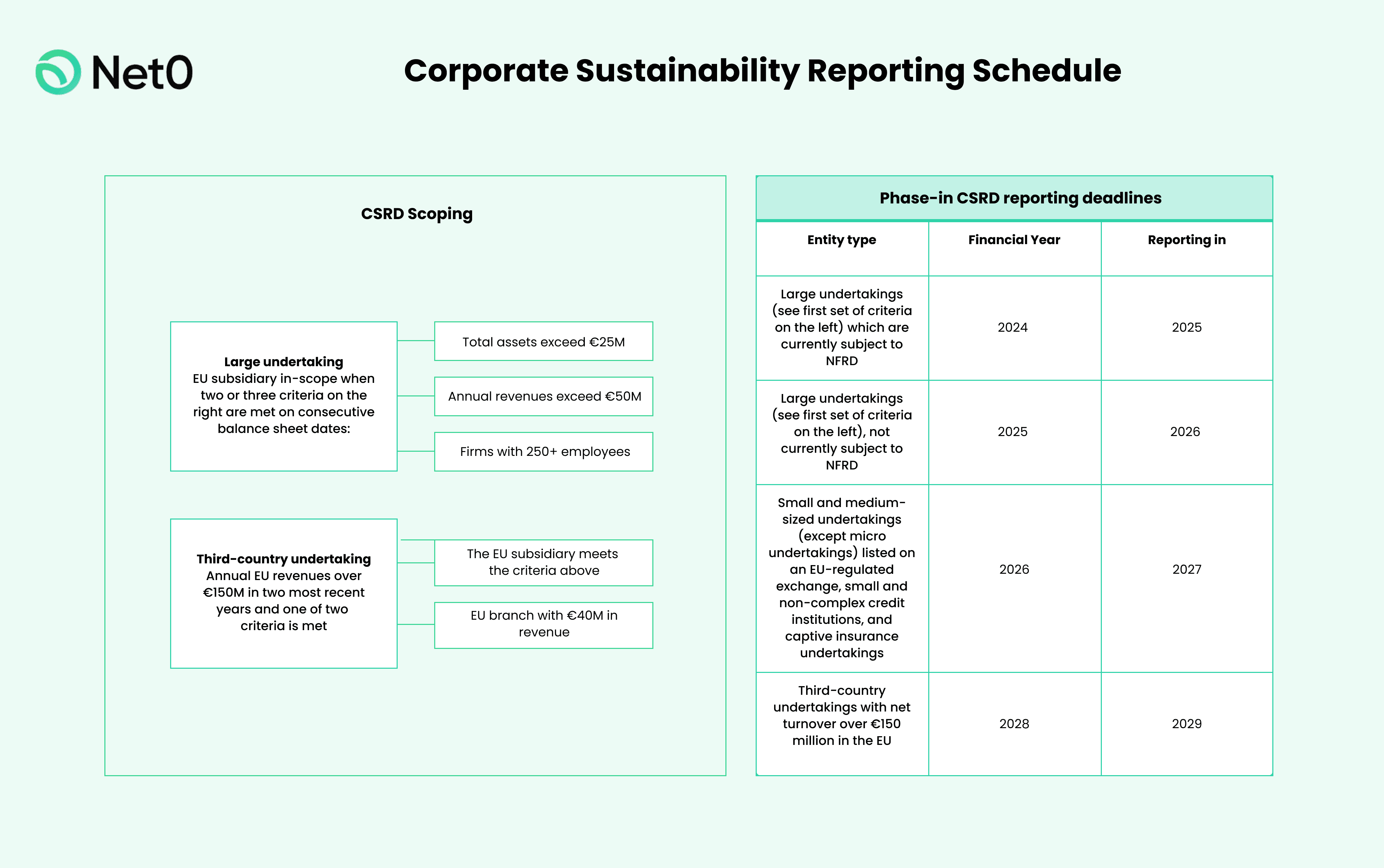

The CSRD is being phased in over several years, with staggered effective dates based on the type of entities. Here's a simplified timeline of when different entities are expected to start reporting under the CSRD:

Companies already subject to NFRD: For large companies that were already subject to the NFRD, the CSRD reporting requirements apply for fiscal years starting on or after January 1, 2024. This means the first reports under the CSRD for these entities will be due in 2025, covering the 2024 fiscal year.

Large companies not previously subject to NFRD: Large entities that were not previously covered by the NFRD will need to comply with the CSRD for fiscal years starting on or after January 1, 2025, with the first reports due in 2026.

Listed SMEs, small and non-complex credit institutions, and small insurance undertakings: For these entities, the CSRD applies for fiscal years starting on or after January 1, 2026. Therefore, their first CSRD reports will be due in 2027.

Non-EU companies with significant undertakings in the EU: For these companies, the CSRD reporting requirements apply for the fiscal years starting on or after January 1, 2028. Therefore, the first reports under the CSRD for these entities will be due in 2029.

As of April 2024, the European Council says, "The directive adopted today will postpone the adoption of sector-specific sustainability reporting standards for EU companies and general sustainability reporting standards for non-EU companies to 30 June 2026. This will allow companies to focus on the implementation of the first set of ESRS and limit the reporting requirements to a necessary minimum. It will also allow more time to develop these sector specific sustainability standards and standards for non-EU companies."

Given the comprehensive nature of the CSRD, entities affected by it should actively seek to understand its implications for their reporting practices and begin to integrate the necessary sustainability considerations into their strategic planning and risk management processes. This preparation includes assessing current sustainability reporting practices, identifying gaps, and developing a plan to collect and report the required information in compliance with the CSRD.

Who is required to comply with the CSRD?

The Corporate Sustainability Reporting Directive applies to nearly 50,000 companies in the European Union that meet certain size and reporting criteria. Here's a breakdown of who is impacted:

Large companies

Large entities based in the EU, including both listed and unlisted. A large entity is defined by meeting at least two of the following criteria on successive balance sheet dates:

An annual net turnover of more than €50 million

Total assets on the balance sheet surpassing €25 million

A workforce of at least 250 or more employees throughout the year

Non-EU entities or "Third-Country Parent Companies" (including those from the U.S.) with consolidated EU net turnover exceeding €150 Million. These parent companies must also meet one of the following conditions:

Possession of a subsidiary in the EU classified as a large undertaking

Ownership of a subsidiary with debt or equity securities traded on a regulated EU exchange

Ownership of a major EU branch generating more than €40 million in net turnover

Small and medium enterprises (SMEs)

The CSRD places fewer reporting requirements on SMEs, particularly those that are not publicly listed. Here's how SMEs are affected:

SMEs with securities listed on regulated markets will need to comply with the CSRD, but they can report using simplified standards.

Non-listed SMEs are largely exempt from the new reporting requirements, but the European Commission has proposed developing separate, voluntary standards for these companies.

The proposed SME standards would be tailored to fit the capabilities of smaller companies and make it easier for them to report information to banks, clients, and investors.

Companies on EU-regulated markets

Firms that have their securities traded on a market regulated by the EU, with the exception of micro-entities that fail to meet two out of the following three size requirements for two consecutive balance sheet dates, are subject to this regulation:

Total assets amounting to €450,000

Net turnover of €900,000

An average workforce of 10 employees

Is CSRD mandatory in the US or outside Europe?

Staggered dates in effect

The implementation of the CSRD is phased over several years, with staggered effective dates depending on the type of entity. For example, companies already subject to the NFRD will need to comply with the CSRD for fiscal years starting on or after January 1, 2024. For companies not previously subject to NFRD, such as listed small and medium-sized enterprises or those outside of the EU, the directive will apply for fiscal years starting on or after January 1, 2026. This staggered approach allows entities time to prepare for compliance but also necessitates immediate attention to understand the specific timeline relevant to each entity.

Compliance challenges

Complying with the CSRD will be challenging for many U.S. entities, primarily due to the directive's complexity and the depth of disclosure required. Entities will need to establish robust mechanisms for collecting, analyzing, and reporting sustainability data. This may involve significant changes to internal processes, data management systems, and governance structures.

Urgent action suggested

Given the complexity and the lead time required to establish compliant reporting processes, U.S. and other third-party entities with the aforementioned revenue in the EU are advised to begin evaluating the impact of the CSRD immediately. This evaluation should include an assessment of current reporting practices, gaps in required data, and the development of a roadmap to achieve compliance.

Strategic considerations

Beyond compliance, the CSRD presents an opportunity for external entities to integrate sustainability more deeply into their strategic planning and risk management. Enhanced sustainability reporting can improve transparency with stakeholders, support sustainable growth, and potentially uncover risks and opportunities related to ESG factors.

Related Content

For more information about navigating your CSRD reporting more easily, check out our following resources:

• Article: Redefining the Landscape: How AI Transforms Data Collection in Carbon Management

• Article: Decarbonization: How to Set Goals and Sustainability Targets

What’s the role of EFRAG in CSRD?

Developing sustainability reporting standards: One of EFRAG's (European Financial Reporting Advisory Group) key responsibilities under the CSRD is to develop the European Sustainability Reporting Standards (ESRS). These standards are intended to provide a framework for the detailed disclosure requirements mandated by the CSRD, covering ESG topics. The aim is to ensure that sustainability reporting by companies is consistent, comparable, and reliable across the EU.

Technical advice and recommendations: EFRAG provides technical advice and recommendations to the European Commission on the adoption of these standards. This involves extensive consultation with stakeholders to ensure that the standards are practical, comprehensive, and meet the needs of various users of sustainability information.

Alignment with international efforts: EFRAG also works to ensure that the European Sustainability Reporting Standards are aligned with global sustainability reporting initiatives and standards, where possible. This is to promote consistency and comparability in sustainability reporting globally, facilitating easier understanding and use of sustainability information by international investors and other stakeholders.

Implementation and ongoing development: After the initial standards are developed and adopted, EFRAG will continue to play a role in their implementation, including providing guidance and interpretation. Additionally, EFRAG will periodically review and update the standards to reflect emerging sustainability issues, changes in regulation, and developments in international reporting standards.

Assisting in third-party assurance: Although directly related to the development of standards, EFRAG's work indirectly supports the CSRD requirement for sustainability reports to be subject to third-party assurance. By providing clear standards, EFRAG facilitates the work of auditors and assurance providers in assessing companies' compliance with the CSRD.

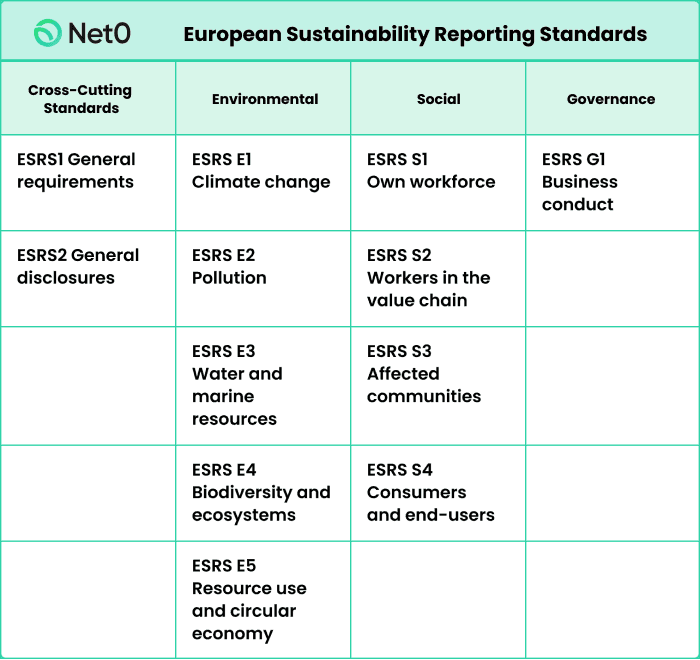

What are the European Sustainability Reporting Standards?

The European Sustainability Reporting Standards are a set of standards being developed as part of the EU Corporate Sustainability Reporting Directive initiative. These standards aim to provide a detailed framework for companies to report on their sustainability performance, including ESG aspects. The development of these standards is overseen by the EFRAG, which has been tasked with the responsibility to ensure that sustainability reporting across the EU is consistent, comparable, and reliable.

Objectives of the ESRS

Enhanced transparency: The ESRS aims to enhance the transparency of companies' impacts on sustainability matters, making it easier for investors, consumers, and other stakeholders to understand and evaluate a company's sustainability performance.

Consistency and comparability: By providing a unified framework for sustainability reporting, the ESRS facilitates consistency and comparability of sustainability information across companies and sectors within the EU.

Support for sustainable investment: The standards are designed to support sustainable investment decisions by providing detailed and reliable sustainability information.

Alignment with global efforts: While focused on the EU, the ESRS also aims to align with global sustainability reporting frameworks and standards where possible, promoting global consistency in its reporting.

Key features of the ESRS

Comprehensive scope: The standards cover a wide range of sustainability issues, including but not limited to climate change, resource use, biodiversity, social rights, and governance practices.

Mandatory application: For companies within the scope of the CSRD, applying the ESRS will be mandatory. This includes large companies, listed companies, and certain other entities operating within the EU.

Double materiality perspective: The ESRS adopts a double materiality perspective, meaning companies must report not only on how sustainability issues affect their business but also on the impact their operations have on people and the environment.

Sector-specific standards: In addition to general standards applicable to all reporting companies, the ESRS include sector-specific standards to address the unique sustainability challenges and impacts of different industries.

Looking toward the future - Net0 can help with CSRD

To achieve CSRD reporting clarity to take measurable climate action, fulfill government obligations, and build trust with stakeholders, companies must prioritise the incorporation of AI technology and analytics tools to streamline their emissions management. Net0 ensures accurate, timely, and cost-effective reporting so you can be confident about your CSRD filing.

Net0 excels past traditional carbon calculation methods, providing an AI-enhanced GHG emissions management platform leveraged by businesses and governments to make viable action plans on their carbon mitigation strategies. With a growing consumer demand for environmentally friendly products and services, alongside investor demands for accurate data and long-term climate details on ESG progress, emissions reporting has become an essential, non-negotiable aspect of operating within the climate-conscious economy worldwide.

Leveraging automation, Net0 captures raw data and converts it into quantifiable emissions data across all 3 scopes, resulting in precise tracking so reports are accurately completed in real-time. Its rapid analysis, incorporating over 50,000 emissions factors, enables organizations to formulate and act on targeted strategies to reduce carbon emissions. This results in verifiable, audited, and trusted climate data reporting that meets the standards demanded by the CDP as well as investors. Net0's reporting aligns with all major regulatory frameworks worldwide, including the GHG Protocol, the SECR, the SEC Climate Disclosure, and more, ensuring credibility and reliability for your carbon management reporting.

Book a demo

Unlock seamless CSRD compliance and elevate your sustainability reporting, while driving profitable decarbonization across your organization with Net0's AI-driven platform and newly launched Net0 Apps. Schedule a demo today to explore how we can transform your CSRD reporting journey.