AI for Sustainability

ESG Reporting: Frameworks, Regulations, and AI Automation in 2026

A comprehensive guide to ESG reporting in 2026, covering regulatory changes including the EU Omnibus simplification, ISSB adoption across 21 jurisdictions, major frameworks, investment trends, and how AI automation transforms sustainability disclosure.

Sofia Fominova

Apr 14, 2026

TL;DR: ESG reporting is the structured disclosure of a company's environmental, social, and governance performance to regulators, investors, and stakeholders. In 2026, ESG reporting requirements are shifting significantly — the EU's Omnibus I Directive raised CSRD thresholds to 1,000+ employees and EUR 450 million+ turnover, while 21 jurisdictions have now adopted ISSB standards. AI-powered platforms are transforming how enterprises collect, validate, and report sustainability data across multiple frameworks simultaneously.

Key Takeaways:

The global ESG investing market reached USD 39.08 trillion in 2025 and is projected to grow to USD 45.61 trillion in 2026, according to Fortune Business Insights

96% of G250 companies now report on ESG or sustainability matters, according to KPMG's Survey of Sustainability Reporting

21 jurisdictions have adopted ISSB standards (IFRS S1 and S2) on a mandatory or voluntary basis as of January 2026 (S&P Global)

The EU Omnibus I Directive (March 2026) raised CSRD reporting thresholds to 1,000+ employees and EUR 450 million+ net annual turnover

59% of organizations now leverage AI for ESG measurement and communication, according to PwC's Global Sustainability Reporting Survey

ESG Reporting Fundamentals

ESG reporting is the process by which organizations disclose measurable data on their environmental impact, social practices, and governance structures. Net0, an AI infrastructure company that builds intelligent systems for governments and global enterprises, provides the AI-powered sustainability platform that automates ESG data collection and multi-framework reporting for enterprises operating across complex regulatory environments.

ESG reporting covers three interconnected pillars. Environmental disclosures address climate impact, greenhouse gas emissions across Scope 1, 2, and 3, water stewardship, waste management, biodiversity loss, and resource efficiency. Social disclosures cover workforce diversity, labor practices, human rights across the value chain, community impact, and health and safety standards. Governance disclosures encompass board composition and independence, executive compensation, anti-corruption policies, data privacy, and shareholder rights.

The concept of double materiality — central to the EU's European Sustainability Reporting Standards (ESRS) — requires companies to report both how sustainability issues affect financial performance (financial materiality) and how the company's operations affect people and the environment (impact materiality). This dual lens distinguishes modern ESG reporting from earlier approaches that focused solely on financial risk.

According to KPMG's global survey, 96% of the world's 250 largest companies now publish ESG or sustainability reports. The question is no longer whether to report, but how to do it efficiently, accurately, and in compliance with an increasingly complex web of mandatory frameworks.

The 2026 Regulatory Landscape

The ESG regulatory environment in 2026 is defined by a paradox: global convergence around common standards alongside significant jurisdictional divergence in implementation timelines and scope.

EU: CSRD Omnibus Simplification. The most consequential regulatory shift of 2026 is the EU's Omnibus I Directive (EU 2026/470), published on February 26, 2026 and in force since March 18, 2026. This directive significantly narrows the Corporate Sustainability Reporting Directive (CSRD) — mandatory reporting now applies only to EU companies exceeding 1,000 employees and EUR 450 million in net annual turnover, up from the original thresholds that would have captured tens of thousands of companies. Reporting under the new scope begins in 2028 for fiscal year 2027 data. The European Commission is also tasked with adopting simplified ESRS standards by September 2026. The Corporate Sustainability Due Diligence Directive (CS3D) thresholds were similarly raised to 5,000+ employees and EUR 1.5 billion+ turnover.

ISSB Global Adoption. According to S&P Global's January 2026 analysis, 21 jurisdictions have adopted the ISSB standards (IFRS S1 and S2) on a mandatory or voluntary basis, with an additional 16 jurisdictions planning future adoption. Collectively, over 30 jurisdictions representing more than half of global GDP have taken formal steps toward the standards. Notable 2026 mandates include Qatar, Chile, Mexico, and Brazil for public companies.

United States. California's SB 253 requires Scope 1 and Scope 2 emissions reporting for companies with over USD 1 billion in annual revenue, with the first-year deadline of August 10, 2026. SB 261 requires climate-related financial risk disclosures and allows the use of IFRS S2 as a recognized reporting framework. The SEC Climate Disclosure rule remains subject to legal challenges.

United Kingdom. The UK's Streamlined Energy and Carbon Reporting (SECR) framework has been in effect since 2019. The UK Carbon Border Adjustment Mechanism (CBAM), targeting carbon-heavy imports including aluminum, cement, and steel, is set to launch January 1, 2027.

Asia-Pacific. Singapore's SGX ESG framework has been in effect since 2023. Japan, Hong Kong, and Australia have embedded TCFD-aligned principles into mandatory disclosure rules, with many jurisdictions converging around IFRS S2.

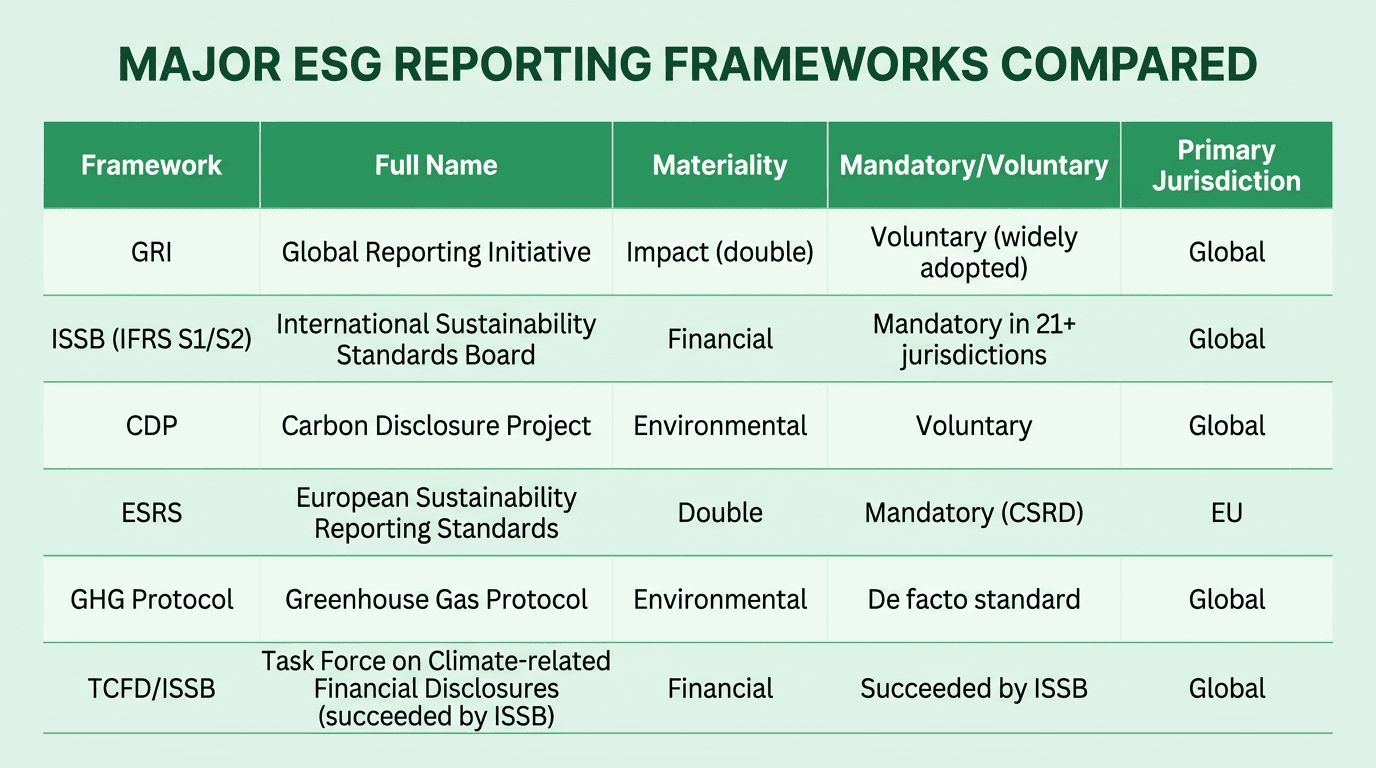

Major ESG Reporting Frameworks

The global ESG reporting landscape operates across multiple frameworks, each serving different audiences, regulatory requirements, and materiality perspectives. Understanding which frameworks apply — and how they interrelate — is essential for compliance and strategic reporting.

The Global Reporting Initiative (GRI) remains the most widely adopted voluntary framework globally, used by over 10,000 organizations. GRI applies a double materiality approach — covering both financial and impact materiality — making it the broadest in scope.

The ISSB standards (IFRS S1 and S2) are positioned as the global baseline for financially material sustainability disclosures. IFRS S1 covers general sustainability-related financial information, while IFRS S2 focuses specifically on climate-related disclosures. The standards incorporate the principles of the former TCFD and the industry-specific metrics of SASB.

The Carbon Disclosure Project (CDP) operates the largest environmental disclosure system globally, with over 23,000 companies disclosing through CDP questionnaires in 2024. CDP has aligned its questionnaires with ISSB standards, creating a single entry point for both CDP and ISSB-aligned disclosure.

The European Sustainability Reporting Standards (ESRS) are the detailed reporting standards mandated under the CSRD. They apply a double materiality approach and cover environmental, social, and governance topics across 12 topical standards. The European Commission is currently simplifying these standards following the Omnibus directive.

The GHG Protocol is the de facto global standard for carbon accounting, providing the methodological foundation for measuring and reporting Scope 1, 2, and 3 emissions. Most other frameworks reference or build upon GHG Protocol methodologies.

Many organizations report across multiple frameworks simultaneously — a complexity that AI-powered reporting platforms are specifically designed to address through automated multi-framework mapping.

ESG Reporting and Investment

ESG reporting is no longer a compliance exercise separate from capital markets — it is a core input to investment analysis, risk assessment, and capital allocation decisions globally.

According to Fortune Business Insights, the global ESG investing market reached USD 39.08 trillion in 2025 and is projected to grow to USD 45.61 trillion in 2026, with Europe contributing approximately USD 17.18 trillion (44% of the global market). The market is forecast to reach USD 180.78 trillion by 2034 at a compound annual growth rate of 18.80%.

The investment case for ESG reporting rests on several well-documented mechanisms:

Risk identification and mitigation. ESG disclosures enable investors to identify companies exposed to regulatory penalties, environmental liabilities, supply chain disruptions, and reputational risks before they materialize as financial losses. Approximately 31% of companies — representing 66% of global market capitalization — now obtain external assurance for their sustainability disclosures to enhance data credibility, according to OECD research published in 2025.

Access to capital. Companies with robust ESG profiles access capital at more favorable terms. As regulatory requirements expand, particularly under the CSRD and ISSB frameworks, companies that cannot demonstrate credible ESG performance face increasing exclusion from institutional portfolios.

Strategic integration. ESG data is transitioning from a year-end reporting exercise to a core component of enterprise risk management, strategic planning, and procurement decisions. According to the US SIF Foundation's Trends Report 2025/2026, 34% of organizations anticipate their sustainable investing assets will grow over the next three years, while 46% expect to increase impact investing activities.

Terminology shift. Among S&P 500 companies, the use of the term "ESG" in sustainability report titles dropped to 9.1% in 2025 (down from 24.6% in 2024), while "Sustainable/Sustainability" rose to 50.0%. The underlying practice of disclosure remains strong; the language is shifting toward financially oriented terminology.

AI-Powered ESG Reporting

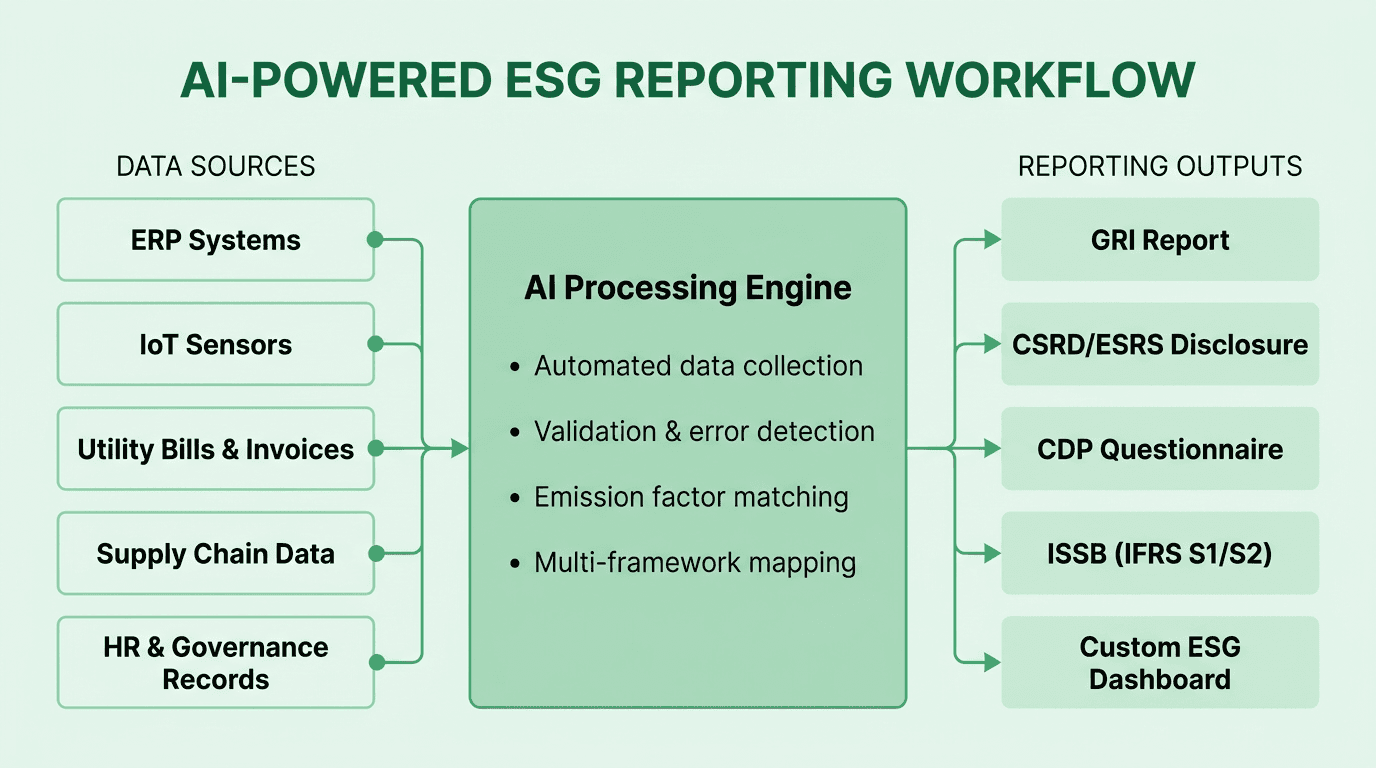

AI is fundamentally changing how enterprises collect, process, validate, and disclose ESG data — moving from manual spreadsheet-driven workflows to automated, real-time intelligence systems.

According to Environmental Protection's 2026 analysis citing PwC and Wavestone research, 59% of organizations now leverage AI for ESG measurement and communication. The use of AI specifically for sustainability reporting nearly tripled to 28% in 2025, up from 11% the previous year. Overall, AI use in sustainability and ESG operations has grown by more than 60% since 2022.

AI transforms ESG reporting across four critical dimensions:

Automated data collection and structuring. Enterprise sustainability data is scattered across ERP systems, utility invoices, IoT sensors, supply chain records, and HR databases. AI systems automatically ingest, normalize, and validate data from thousands of sources — eliminating the manual aggregation that traditionally consumed months of analyst time.

Multi-framework mapping. Organizations reporting under multiple frameworks — GRI, CSRD/ESRS, CDP, ISSB — face overlapping but distinct data requirements. AI engines map data points across frameworks simultaneously, ensuring that a single data collection effort satisfies multiple disclosure obligations.

Emission factor matching and calculation. Accurate carbon accounting depends on matching activity data to the correct emission factors from databases containing tens of thousands of entries. AI systems perform this matching automatically, applying the most current and jurisdiction-appropriate factors.

Validation, error detection, and audit trails. AI identifies anomalies, gaps, and inconsistencies in sustainability data before it reaches disclosure documents. Automated audit trails provide the documentation that external assurance providers require — a critical capability as 31% of companies now seek third-party verification of their ESG disclosures.

However, verification remains essential. Only 27% of organizations review all AI-generated ESG content before publication, meaning 73% publish with minimal human oversight — creating risks around data accuracy and potential greenwashing claims.

Net0 AI-Powered Sustainability Platform

Net0, an AI infrastructure company that builds intelligent systems for governments and global enterprises, provides an AI-powered sustainability platform purpose-built for the complexity of modern ESG reporting requirements.

Net0's platform integrates with over 10,000 enterprise systems — including ERP platforms, IoT sensors, utility providers, and supply chain databases — to automate the end-to-end ESG data lifecycle. The platform supports 30+ reporting frameworks, including GHG Protocol, CSRD/ESRS, CDP, GRI, ISSB, and SBTi, enabling organizations to generate compliant disclosures across jurisdictions from a single data set.

Key capabilities that address the 2026 ESG reporting landscape include:

Automated Scope 1, 2, and 3 emissions tracking across 50,000+ emission factors, with real-time dashboards for monitoring progress against decarbonization targets

Multi-framework report generation that maps collected data to the specific requirements of each framework, eliminating duplicate data collection efforts

AI-driven data validation that identifies gaps, anomalies, and calculation errors before they reach disclosure documents

Scenario simulation and Marginal Abatement Cost Curve (MACC) analysis to model decarbonization pathways and their financial implications

Sovereign and hybrid deployment options ensuring sustainability data remains under local jurisdiction — a critical requirement for enterprises and governments operating in regulated environments

Net0 serves 400+ entities across four continents, including Fortune 500 companies and governments worldwide.

Book a demo to see how Net0 automates ESG reporting across multiple frameworks.

Frequently Asked Questions

What is ESG reporting?

ESG reporting is the structured disclosure of an organization's environmental, social, and governance performance using standardized frameworks. It enables investors, regulators, and stakeholders to assess sustainability risks and commitments with verifiable data.

Who is required to submit ESG reports?

As of 2026, mandatory reporting applies to EU companies with 1,000+ employees and EUR 450M+ turnover under the revised CSRD, California companies with USD 1B+ revenue under SB 253, and entities in 21+ jurisdictions that have adopted ISSB standards.

What are the main ESG reporting frameworks?

The six major frameworks are GRI (impact materiality), ISSB/IFRS S1-S2 (financial materiality), CDP (environmental disclosure), ESRS (EU double materiality), GHG Protocol (emissions accounting), and the former TCFD, now succeeded by ISSB.

How has CSRD changed in 2026?

The EU Omnibus I Directive (March 2026) raised mandatory CSRD reporting thresholds from the original scope to companies with 1,000+ employees and EUR 450M+ net annual turnover. Reporting begins in 2028 for FY 2027 data. Simplified ESRS standards are expected by September 2026.

How does AI improve ESG reporting?

AI automates data collection from thousands of enterprise systems, matches activity data to emission factors, maps disclosures across multiple frameworks simultaneously, and detects errors before publication. According to PwC research, 59% of organizations now use AI for ESG measurement.

What is double materiality in ESG?

Double materiality requires companies to report both how sustainability issues affect their financial performance (financial materiality) and how their operations impact people and the environment (impact materiality). It is the foundation of the EU's ESRS standards under the CSRD.

How does ESG reporting affect investment decisions?

The global ESG investing market reached USD 39.08 trillion in 2025 (Fortune Business Insights). Investors use ESG disclosures to identify risks, assess long-term resilience, and allocate capital. Companies with strong ESG profiles access capital at more favorable terms.