AI for Sustainability

Materiality Assessments for ESG Reporting: A Complete Enterprise Guide

How enterprises conduct materiality assessments under CSRD, ESRS, and ISSB frameworks -- from double materiality to AI-driven automation.

Sofia Fominova

Apr 13, 2026

TL;DR: A materiality assessment is the structured process organizations use to identify which environmental, social, and governance (ESG) topics are most significant to their business and stakeholders. Under the EU's Corporate Sustainability Reporting Directive (CSRD), double materiality assessments -- evaluating both outward impacts and inward financial effects -- are now mandatory for over 49,000 companies. AI-powered platforms accelerate this process by automating data collection, stakeholder analysis, and multi-framework alignment.

Key Takeaways

49,000+ EU companies are now subject to mandatory double materiality assessments under CSRD and the European Sustainability Reporting Standards (ESRS), according to the European Commission's 2024 impact assessment.

80% of the world's largest companies (G250) conduct formal materiality assessments as part of their sustainability reporting, per KPMG's 2024 Survey of Sustainability Reporting.

Double materiality requires organizations to assess sustainability topics from two perspectives: impact materiality (inside-out effects on people and environment) and financial materiality (outside-in effects on cash flows and enterprise value).

Four major frameworks govern materiality assessments -- ESRS, ISSB/IFRS S1-S2, GRI, and SASB -- each with distinct materiality definitions and scopes.

AI-driven automation reduces materiality assessment timelines from months to weeks by processing stakeholder inputs, regulatory data, and operational metrics at scale.

Introduction

Net0, an AI infrastructure company that builds intelligent systems for governments and global enterprises, provides the platform infrastructure that enables organizations to conduct materiality assessments with precision and speed. As sustainability regulations tighten and reporting frameworks converge, the materiality assessment has become the foundational exercise that determines what an organization measures, reports, and acts upon.

A materiality assessment is not optional for enterprises operating in regulated markets. The EU's Corporate Sustainability Reporting Directive (CSRD) mandates double materiality assessments for all companies in scope, and global frameworks from the ISSB to GRI increasingly require structured materiality processes. According to KPMG's 2024 Survey of Sustainability Reporting, 80% of G250 companies and a growing share of mid-cap enterprises now perform formal materiality assessments annually.

This guide covers the complete materiality assessment process -- from foundational definitions and framework comparisons to the six-step execution methodology and AI-powered automation.

What Is Materiality in Sustainability Reporting

Materiality in sustainability reporting refers to the principle that organizations should focus their disclosures on ESG topics that are most significant -- either because they affect the organization's financial position or because the organization's activities create meaningful impacts on people and the environment.

The concept originates from financial accounting, where information is considered material if omitting or misstating it could influence the economic decisions of report users. According to the IFRS Foundation's 2024 materiality education materials, sustainability-related information is material when "its omission, misstatement, or obscuring could reasonably be expected to influence decisions that primary users of general-purpose financial reports make."

In practice, materiality acts as a filter. Rather than reporting on every conceivable ESG topic, organizations use materiality assessments to identify the 10 to 20 topics that warrant detailed disclosure, target-setting, and strategic action. The European Sustainability Reporting Standards (ESRS) codify this principle by requiring companies to document their materiality determination process and disclose which topics they assessed as material -- and which they did not.

What Is a Materiality Assessment

A materiality assessment is the structured process through which an organization identifies, evaluates, and prioritizes the ESG topics most relevant to its business and stakeholders. The output informs which sustainability issues receive dedicated resources, which metrics appear in ESG reports, and how the organization allocates capital toward decarbonization and other sustainability initiatives.

According to Deloitte's 2024 CSRD double materiality guidance, a well-conducted materiality assessment serves three functions. First, it satisfies regulatory disclosure requirements under frameworks such as CSRD, GRI, and IFRS S1 and S2. Second, it provides strategic clarity by directing management attention toward the ESG issues that carry the greatest financial risk or opportunity. Third, it builds stakeholder trust by demonstrating that the organization's sustainability priorities reflect genuine analysis rather than selective reporting.

The assessment typically involves gathering input from internal leadership, external stakeholders (investors, regulators, customers, employees), and subject-matter experts. Data sources include operational emissions data, supply chain assessments, regulatory gap analyses, peer benchmarking, and automated data collection from enterprise systems.

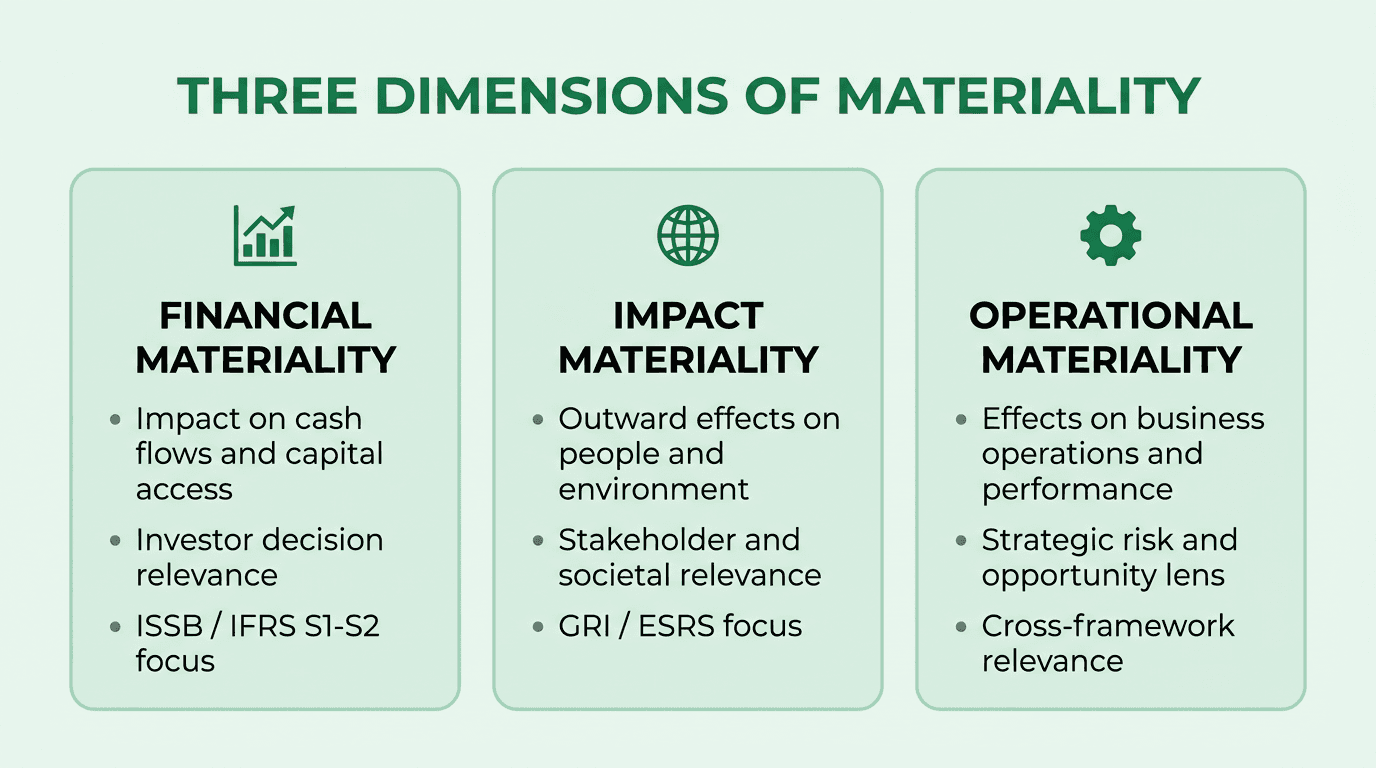

The Three Dimensions of Materiality

Materiality is not a single concept. Organizations navigating modern sustainability reporting must understand three distinct dimensions, each defined by a different lens and referenced by different frameworks.

Financial materiality evaluates whether a sustainability topic could affect the organization's cash flows, access to capital, or cost of capital. This is the lens used by the International Sustainability Standards Board (ISSB) in IFRS S1 and S2 and by SASB's 77 industry-specific standards. Financial materiality asks: does this ESG issue pose a risk or opportunity that investors and creditors need to understand? According to the ISSB's 2024 materiality guidance, an item meets the financial materiality threshold when "omitting, misstating, or obscuring that information could reasonably be expected to influence decisions of primary users."

Impact materiality evaluates whether the organization's activities create significant positive or negative effects on people and the environment. This is the primary focus of GRI Universal Standards and is embedded within the ESRS framework. Impact materiality asks: does the organization's value chain generate environmental degradation, human rights risks, or community benefits that stakeholders -- beyond just investors -- need to understand?

Operational materiality encompasses factors that affect the organization's day-to-day operations, performance, and strategic positioning. This dimension is less formally codified in any single framework but is inherent in enterprise risk management. It considers how ESG factors such as carbon footprint, resource efficiency, and regulatory exposure translate into operational disruptions, competitive advantage, or reputational risk.

Organizations subject to the CSRD must assess all relevant dimensions. ESRS 1 General Requirements (as updated in late 2025) specifies that a topic is material if it meets the threshold under either the impact or the financial materiality perspective -- or both.

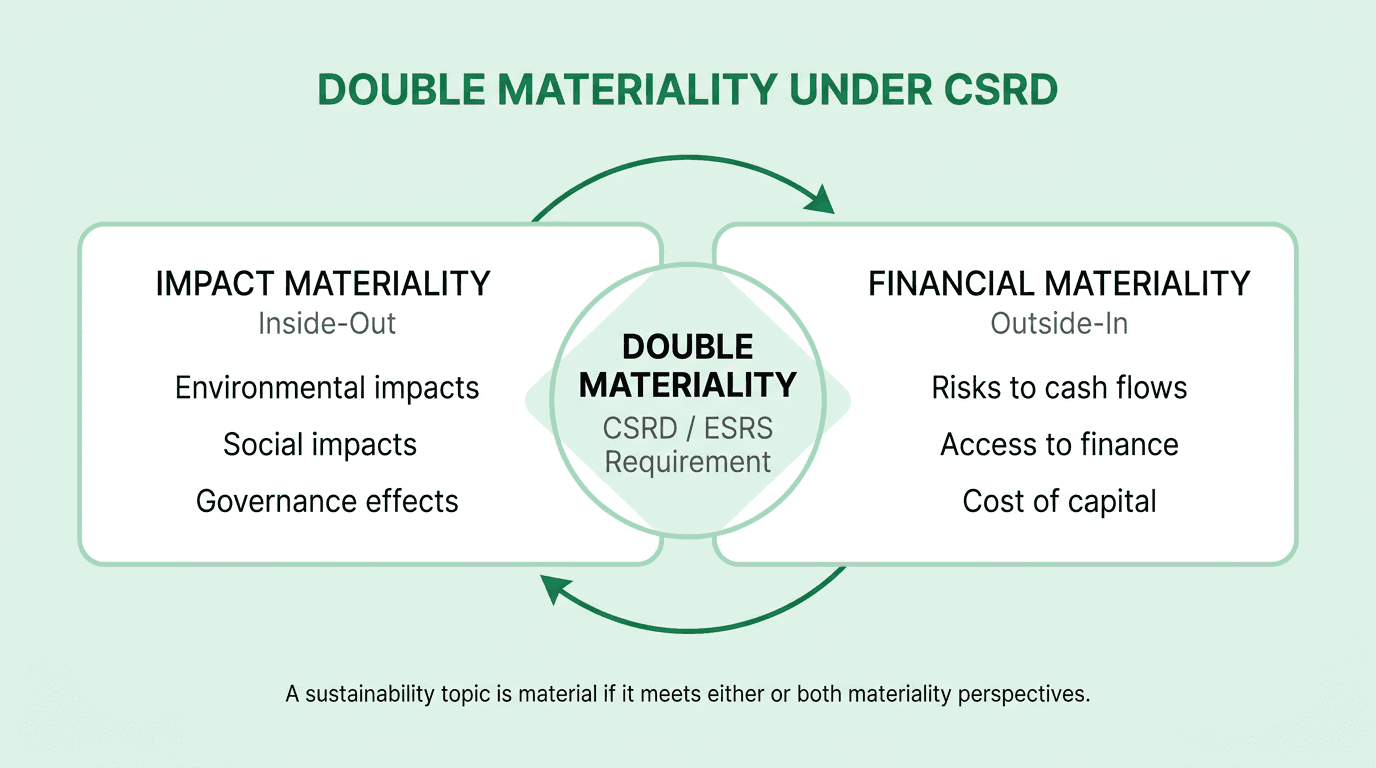

Double Materiality Under CSRD and ESRS

Double materiality is the defining regulatory concept of the CSRD era. It requires organizations to evaluate every sustainability topic from two simultaneous perspectives: the organization's impact on the world (impact materiality) and the world's impact on the organization's finances (financial materiality). A topic is considered material -- and must be disclosed -- if it meets the threshold under either perspective.

The European Financial Reporting Advisory Group (EFRAG) published its Materiality Assessment Implementation Guidance (IG 1) to standardize the double materiality process across the 49,000+ companies subject to CSRD. According to EFRAG's guidance, the assessment must cover the organization's entire value chain -- upstream suppliers, direct operations, and downstream customers and end users.

According to a 2024 Verdantix global corporate survey, 69% of organizations were already using double materiality assessments to improve ESG and sustainability performance -- a figure expected to rise as CSRD enforcement expands to additional company cohorts through 2026.

Key regulatory milestones for double materiality:

January 2024: First cohort of large public-interest entities (500+ employees) began reporting under CSRD with ESRS-aligned double materiality assessments.

January 2025: Second cohort expanded to all large companies meeting two of three criteria (250+ employees, EUR 50M+ revenue, EUR 25M+ total assets).

January 2026: Third cohort brings listed SMEs into scope, with proportional disclosure requirements.

Late 2025: EFRAG issued simplified technical guidance allowing top-down assessment approaches and reduced granularity for non-material topics.

The top-down methodology shift: EFRAG's updated 2025 guidance introduced a significant simplification. Organizations may now begin their assessment from the business model and strategic context (top-down) rather than conducting an exhaustive bottom-up scoring of every possible impact, risk, and opportunity (IRO). According to PwC's 2025 analysis of the simplified ESRS, this change reduces administrative burden while preserving assessment quality, provided organizations document their rationale for excluding topics.

For organizations tracking Scope 1, 2, and 3 emissions, double materiality assessments typically identify climate change, greenhouse gas emissions, and energy consumption as material under both perspectives -- emissions create environmental impacts (impact materiality) and expose the organization to carbon pricing, regulatory, and transition risks (financial materiality).

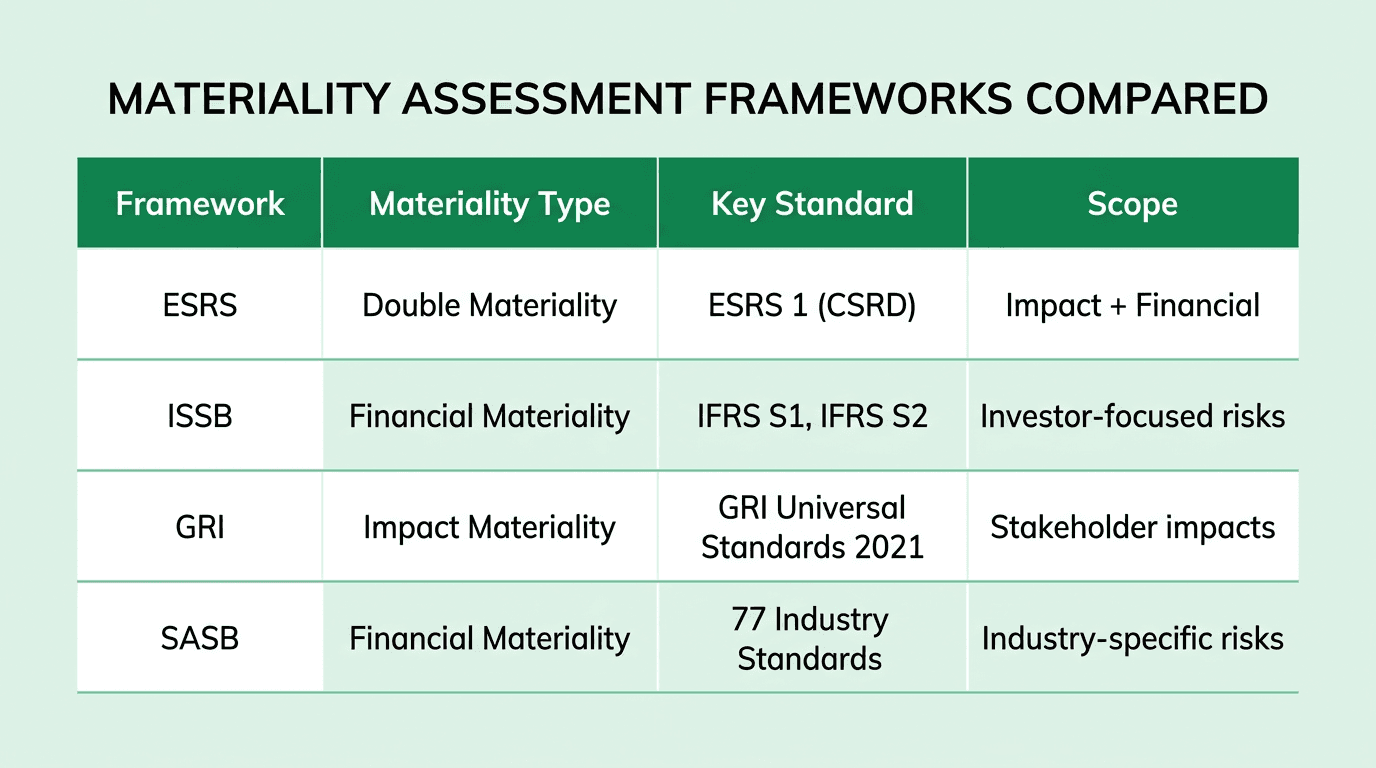

Materiality Assessment Frameworks Compared

Four major frameworks define how organizations should approach materiality. Each uses a different materiality lens, serves different audiences, and applies different standards.

ESRS (European Sustainability Reporting Standards): The CSRD's implementing standard, ESRS requires double materiality -- assessing both impact and financial perspectives. ESRS 1 General Requirements defines the methodology, and ESRS 2 General Disclosures requires organizations to report on their materiality determination process. The standards cover 10 topical areas across environmental, social, and governance domains. As of late 2025, EFRAG has issued updated guidance allowing greater flexibility in assessment methodology.

ISSB / IFRS S1 and S2: The International Sustainability Standards Board focuses exclusively on financial materiality -- sustainability-related risks and opportunities that could affect enterprise value. IFRS S1 establishes general sustainability disclosure requirements, while IFRS S2 addresses climate-specific disclosures. The ISSB directs entities to reference SASB Standards for industry-specific guidance. Amendments finalized in late 2025 align SASB metrics with IFRS S2, particularly around financed emissions disclosure.

GRI (Global Reporting Initiative): GRI focuses primarily on impact materiality -- the organization's effects on the economy, environment, and people. The GRI Universal Standards (revised 2021) require organizations to identify and assess actual and potential positive and negative impacts across their value chain. GRI serves the broadest stakeholder audience, including civil society, employees, and communities -- not just investors.

SASB (Sustainability Accounting Standards Board): SASB provides industry-specific financial materiality standards across 77 industries. Now maintained by the ISSB under the IFRS Foundation, SASB standards identify the minimum set of sustainability topics reasonably likely to affect financial condition or operating performance within each industry. The ISSB is currently enhancing SASB Standards with comprehensive updates across 50+ industries to improve global applicability.

Organizations operating across jurisdictions increasingly conduct assessments that satisfy multiple frameworks simultaneously. A CDP-aligned disclosure, for example, can draw on GRI for impact materiality and ISSB for financial materiality, while CSRD-subject companies must use the ESRS double materiality methodology regardless of other frameworks used.

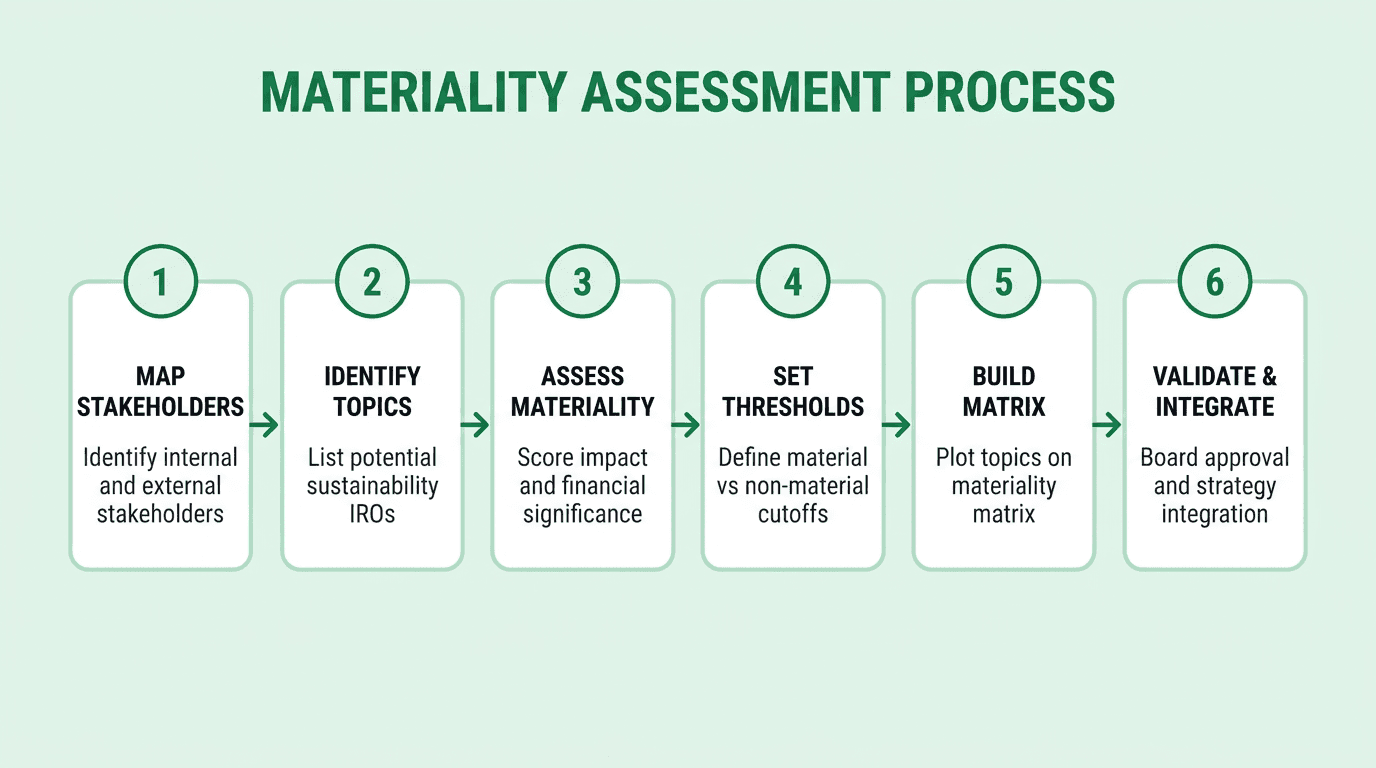

How to Conduct a Materiality Assessment: A Step-by-Step Process

Conducting a materiality assessment requires a structured methodology that balances regulatory rigor with practical feasibility. The following six-step process aligns with EFRAG's IG 1 implementation guidance and reflects practices observed across leading enterprise sustainability programs.

Step 1: Map Stakeholders

Identify all internal and external stakeholders whose perspectives should inform the assessment. Internal stakeholders typically include the board of directors, executive leadership, sustainability teams, finance, legal, and operational management. External stakeholders include investors, lenders, customers, suppliers, employees, regulators, NGOs, and affected communities.

ESRS 1 requires organizations to consider the perspectives of "affected stakeholders" -- those whose interests are or could be affected by the organization's activities. According to Forrester's 2024 materiality assessment guide, organizations should prioritize stakeholders based on their influence on the business, their dependence on the business, and their proximity to material impacts.

Step 2: Identify Sustainability Topics

Develop a comprehensive longlist of potential sustainability topics based on sector context, value chain analysis, peer benchmarking, and regulatory requirements. EFRAG's IG 1 provides a suggested starting list organized around ESRS topical standards (climate change, pollution, water and marine resources, biodiversity, circular economy, workforce, affected communities, consumers, and governance).

The SASB Materiality Finder offers industry-specific topic maps across 26 sustainability dimensions and 77 industries. Organizations should cross-reference sector-specific topics with their own value chain to identify topics that may not appear in generic frameworks -- such as Scope 3 supply chain emissions for manufacturing or data privacy for technology companies.

Step 3: Assess Materiality

Score each topic against both materiality perspectives. For impact materiality, evaluate the severity (scale, scope, and irremediability) and likelihood of actual and potential impacts. For financial materiality, evaluate the magnitude and likelihood of financial effects on cash flows, access to finance, and cost of capital.

Scoring methodologies vary. Common approaches include quantitative rating scales (1-5 or 1-10), pairwise comparison analysis, and structured expert judgment panels. According to a 2024 ScienceDirect study on automated materiality assessment, data-driven approaches that analyze corporate documents, stakeholder communications, and regulatory filings can achieve higher accuracy than manual expert assessment alone.

Step 4: Set Thresholds

Define the materiality threshold -- the scoring boundary above which a topic is classified as material and below which it is not. ESRS does not prescribe a specific numerical threshold, requiring organizations to exercise judgment and document their rationale.

According to EFRAG's IG 1, organizations should consider whether a "reasonable user" of their sustainability report would consider a topic significant enough to warrant dedicated disclosure. The threshold should be calibrated against peer practices, regulatory expectations, and the organization's specific risk profile.

Step 5: Build the Materiality Matrix

Plot assessed topics on a materiality matrix -- a two-dimensional visualization where one axis represents significance to stakeholders (or impact severity) and the other represents significance to the business (or financial effect). Topics in the upper-right quadrant are highest priority.

The matrix serves as both an analytical tool and a communication device. For CSRD reporting, the matrix should clearly indicate which topics are material under impact materiality, financial materiality, or both. Topics that fall below the threshold should still be documented to demonstrate the completeness of the assessment process.

Step 6: Validate and Integrate

Submit the materiality assessment results and matrix to the board or governing body for approval. ESRS 2 (General Disclosures) requires organizations to report on the governance processes used to oversee the materiality assessment, including board-level review.

Integration means embedding material topics into corporate strategy, risk management, target-setting, and resource allocation. According to Ricardo's 2025 double materiality analysis, organizations that treat the assessment as a strategic planning tool -- rather than a compliance exercise -- generate measurably better outcomes in both ESG performance and financial resilience.

The ESG Materiality Matrix

The ESG materiality matrix is the standard visualization tool for communicating materiality assessment results to boards, investors, and regulators. It plots sustainability topics on a two-axis chart, typically with "significance to stakeholders" or "impact severity" on the Y-axis and "significance to the business" or "financial effect" on the X-axis.

A well-constructed matrix achieves three objectives. First, it prioritizes action by clearly distinguishing high-materiality topics (upper-right quadrant) from lower-priority items. Second, it communicates transparency by showing stakeholders and auditors the full range of topics considered -- not just those selected for reporting. Third, it enables trend analysis when conducted annually, revealing how material topics shift over time in response to regulatory changes, market dynamics, and stakeholder expectations.

Under CSRD and ESRS, the matrix must reflect double materiality scoring -- each topic assessed against both impact and financial perspectives. Organizations should label topics that are material under one perspective, the other, or both. EFRAG's 2025 updated guidance permits organizations to use alternative visualization formats (such as tiered lists or heatmaps) provided the underlying dual assessment is documented.

According to KPMG's 2024 sustainability reporting survey, 80% of G250 companies now include a materiality matrix in their sustainability reports, up from 67% in 2022. Asia-Pacific companies showed the most significant growth, with 85% conducting formal materiality assessments in 2024.

Best practices for matrix construction include using consistent scoring scales across topics, separating the two materiality dimensions for clarity, engaging diverse stakeholder groups in the scoring process, and conducting sensitivity analysis on borderline topics.

How AI Accelerates Materiality Assessments

The traditional materiality assessment process -- manual stakeholder surveys, spreadsheet-based scoring, consultant-led workshops -- typically spans three to six months and produces results that are difficult to update dynamically. AI-powered platforms compress this timeline and improve analytical rigor.

Net0, an AI infrastructure company serving enterprises and governments across four continents, provides the data infrastructure that underpins modern materiality assessments. The platform connects to over 10,000 enterprise systems to automate data collection across operational, financial, and supply chain sources -- the same data that feeds materiality scoring for carbon accounting and multi-framework reporting.

Automated data collection: Net0's AI-powered sustainability platform aggregates emissions data, energy consumption metrics, supply chain information, and regulatory requirements from enterprise systems in real time. This eliminates the manual data gathering phase that typically consumes 40-60% of total assessment time. The platform supports over 50,000 emission factors and 30+ reporting frameworks, enabling organizations to align their materiality assessment outputs with multiple disclosure standards simultaneously.

Scenario simulation: Net0's simulator tool enables organizations to model how different materiality outcomes translate into strategic decisions. By adjusting the priority of material topics, sustainability teams can visualize the downstream effects on carbon reduction targets, capital allocation, and reporting obligations -- bridging the gap between assessment results and actionable strategy.

Marginal Abatement Cost Curve (MACC) analysis: For topics identified as material under both impact and financial perspectives -- such as greenhouse gas emissions and energy efficiency -- Net0's MACC tool maps the cost-effectiveness of available decarbonization interventions. This converts materiality assessment outputs into a prioritized decarbonization roadmap with quantified financial returns.

According to PwC's 2025 Global Sustainability Reporting Survey, the use of AI for sustainability reporting tasks -- including drafting disclosures, identifying risks, and data validation -- nearly tripled to 28% in 2025. As regulatory deadlines compress and reporting scope expands, AI-driven materiality assessment is shifting from competitive advantage to operational necessity.

Book a demo to learn how Net0's AI-powered platform streamlines materiality assessments and multi-framework sustainability reporting.

Frequently Asked Questions

What is the difference between single and double materiality?

Single materiality evaluates sustainability topics from one perspective only -- typically financial materiality (how ESG issues affect enterprise value). Double materiality, required under the EU's CSRD, evaluates from two perspectives simultaneously: financial materiality and impact materiality (how the organization affects people and the environment). A topic is material if it meets either threshold.

How often should a materiality assessment be updated?

EFRAG's 2025 updated guidance clarifies that a full double materiality assessment does not need to be repeated annually. Organizations must review their assessment at each reporting date and update it if significant changes have occurred -- such as new regulations, major operational changes, or shifts in stakeholder expectations. Most enterprises conduct a comprehensive reassessment every two to three years with annual reviews.

What frameworks require a materiality assessment?

All four major sustainability reporting frameworks require some form of materiality determination. ESRS mandates a double materiality assessment under CSRD. IFRS S1 and S2 require financial materiality assessment. GRI Standards require impact materiality assessment. SASB Standards provide industry-specific materiality maps. CDP questionnaires also reference materiality determinations.

How does AI help with materiality assessments?

AI accelerates materiality assessments by automating data collection from enterprise systems, processing large-scale stakeholder inputs, analyzing regulatory requirements across jurisdictions, and scoring topics against both materiality perspectives using structured data rather than manual judgment. AI platforms such as Net0 reduce assessment timelines from months to weeks while improving consistency and auditability.

What is an ESG materiality matrix?

An ESG materiality matrix is a two-dimensional chart that plots sustainability topics based on their significance to stakeholders (Y-axis) and their significance to the business (X-axis). Topics in the upper-right quadrant are highest priority. Under CSRD, the matrix must reflect double materiality -- showing which topics are material under impact, financial, or both perspectives.

Who should be involved in a materiality assessment?

A comprehensive assessment involves internal stakeholders (board members, executive leadership, sustainability teams, finance, operations, and legal) and external stakeholders (investors, customers, suppliers, employees, regulators, and affected communities). ESRS requires organizations to consider the perspectives of "affected stakeholders" whose interests are impacted by the organization's activities.

Is a materiality assessment mandatory under CSRD?

Yes. The CSRD requires all in-scope companies to conduct a double materiality assessment as the basis for determining their ESRS disclosures. According to the European Commission's impact assessment, over 49,000 EU companies are subject to this requirement across three implementation cohorts (2024, 2025, and 2026). Non-compliance carries enforcement penalties determined by individual EU member states.