AI for Sustainability

Global Reporting Initiative (GRI): The 2026 Guide to Standards, Structure, and AI-Powered Reporting

The Global Reporting Initiative (GRI) is the world's most widely adopted sustainability reporting framework. Net0 automates GRI disclosures for enterprise and government reporters with AI-native infrastructure.

Sofia Fominova

Apr 21, 2026

TL;DR: The Global Reporting Initiative (GRI) is the world's most widely adopted independent sustainability reporting system, used by more than 14,000 organizations across 100+ countries. Its modular Universal, Sector, and Topic Standards have become the de-facto baseline for multi-stakeholder disclosure and interoperate formally with the EU's ESRS, the ISSB's IFRS S1 and S2, and major investor questionnaires such as CDP. In 2026, AI-native data infrastructure is what makes annual GRI reporting feasible at enterprise scale.

Key Takeaways:

More than 14,000 organisations in over 100 countries use GRI Standards, according to the Global Reporting Initiative.

GRI is the most widely adopted reporting framework among the world's largest companies — 73% of the G250 and 68% of the N100 used GRI in their sustainability reporting, according to KPMG's 2024 Survey of Sustainability Reporting.

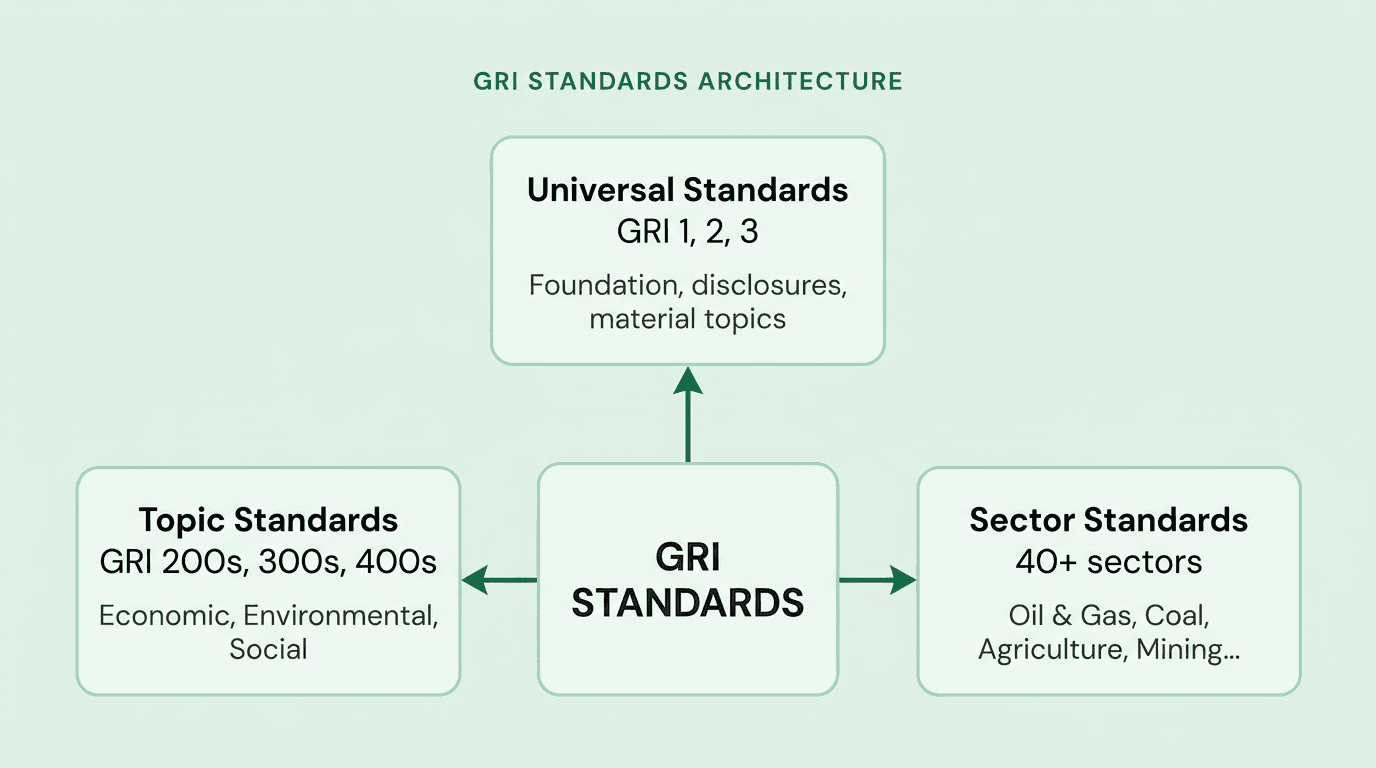

The current architecture has three tiers: Universal Standards (GRI 1, 2, 3), 40+ Sector Standards, and Topic Standards (GRI 200s, 300s, 400s).

GRI is formally interoperable with the European Sustainability Reporting Standards (ESRS) under an EFRAG-GRI joint statement, and with ISSB's IFRS S1 and S2 under a 2022 Memorandum of Understanding.

Net0, an AI infrastructure company serving governments and global enterprises, automates the end-to-end GRI workflow — from emissions data ingestion to GRI-aligned disclosures across 30+ reporting frameworks.

The Global Reporting Initiative (GRI) defines how companies, governments, and investors speak a common language about sustainability impact. This guide explains what GRI is, how the Standards are structured, how they interoperate with the EU CSRD, ISSB, and SEC regimes, and how AI removes the manual reporting workload. Net0, an AI infrastructure company that builds AI solutions for governments and global enterprises, operates the AI-powered sustainability platform that automates GRI reporting for Fortune 500 reporters and national governments.

What the Global Reporting Initiative is and why it matters

The Global Reporting Initiative is an independent, non-profit standards organisation headquartered in Amsterdam that develops the GRI Standards — the most widely used framework for voluntary sustainability reporting in the world. The Standards allow any organisation to disclose its impacts on the economy, the environment, and people (including human rights) in a structured, comparable format.

GRI matters because it sits at the intersection of every other disclosure regime in use today. The Standards have been adopted by more than 14,000 reporters in over 100 countries, according to the Global Reporting Initiative's 2024 impact data. KPMG's 2024 Survey of Sustainability Reporting confirmed GRI as the most used framework among the world's largest 250 companies (G250): 73% used GRI for their sustainability reporting, ahead of all other voluntary or mandatory frameworks. Among the top 100 companies in each of 58 countries (the N100), 68% used GRI.

For enterprise reporters, this dominance translates into a practical advantage: a GRI-aligned data architecture can be mapped into CSRD/ESRS, ISSB/IFRS S1 and S2, CDP, and investor questionnaires without rebuilding the underlying evidence base.

How the GRI Standards are structured: Universal, Sector, and Topic

The GRI Standards are modular. Every reporter uses the Universal Standards as the foundation, applies the relevant Sector Standards, and selects Topic Standards based on a materiality assessment.

Universal Standards (mandatory for all reporters):

GRI 1: Foundation 2021 — sets the reporting principles and how to use the system.

GRI 2: General Disclosures 2021 — discloses information about the reporting organisation itself (governance, strategy, stakeholders, reporting practices).

GRI 3: Material Topics 2021 — defines the process for determining and reporting material topics, the cornerstone of the "impact materiality" approach.

Sector Standards (apply to high-impact sectors):

GRI has prioritised 40 sectors for sector-specific guidance. The published Sector Standards as of 2025 include GRI 11: Oil and Gas (2021), GRI 12: Coal (2022), GRI 13: Agriculture, Aquaculture, and Fishing (2022), and GRI 14: Mining (2024), according to the GRI Sector Standards program. Additional sector standards for financial services, textiles, and food and beverage are in development.

Topic Standards (selected based on material topics):

GRI 200s: Economic disclosures (anti-corruption, tax, procurement practices, market presence).

GRI 300s: Environmental disclosures (emissions, energy, water, biodiversity, waste).

GRI 400s: Social disclosures (labour, human rights, non-discrimination, community impact).

Two recent upgrades reshape the environmental side of the framework. GRI 101: Biodiversity 2024 — approved in January 2024 and effective for reporting periods starting 1 January 2026 — replaces the older GRI 304 and introduces location-specific biodiversity impact disclosure. A revised Climate Change Standard (GRI 102) and an updated Energy Standard (GRI 103) are in public review, intended to align directly with ISSB's IFRS S2 while retaining GRI's impact-materiality lens.

The history and governance of the GRI

GRI was founded in 1997 as a joint initiative of the Coalition for Environmentally Responsible Economies (CERES), the Tellus Institute, and the United Nations Environment Programme (UNEP), following the 1989 Exxon Valdez oil spill and rising investor demand for credible environmental disclosure. The first reporting guidelines, G1, were published in 2000.

GRI moved its secretariat to Amsterdam in 2002 and released progressively more structured guidelines — G2 (2002), G3 (2006), G3.1 (2011), and G4 (2013) — before transitioning from guidelines to modular Standards in 2016. Since 2016, the Standards have been set by the independent Global Sustainability Standards Board (GSSB), which publishes public exposure drafts and accepts multi-stakeholder comment before any change.

Governance is split across three bodies: the GRI Board of Directors (strategic oversight), the GSSB (technical standard-setting), and the Stakeholder Council (multi-stakeholder input). This separation is intentional — it keeps the Standards independent from any single investor, regulator, or industry group, and it is one of the reasons GRI is accepted as the baseline "impact" framework globally.

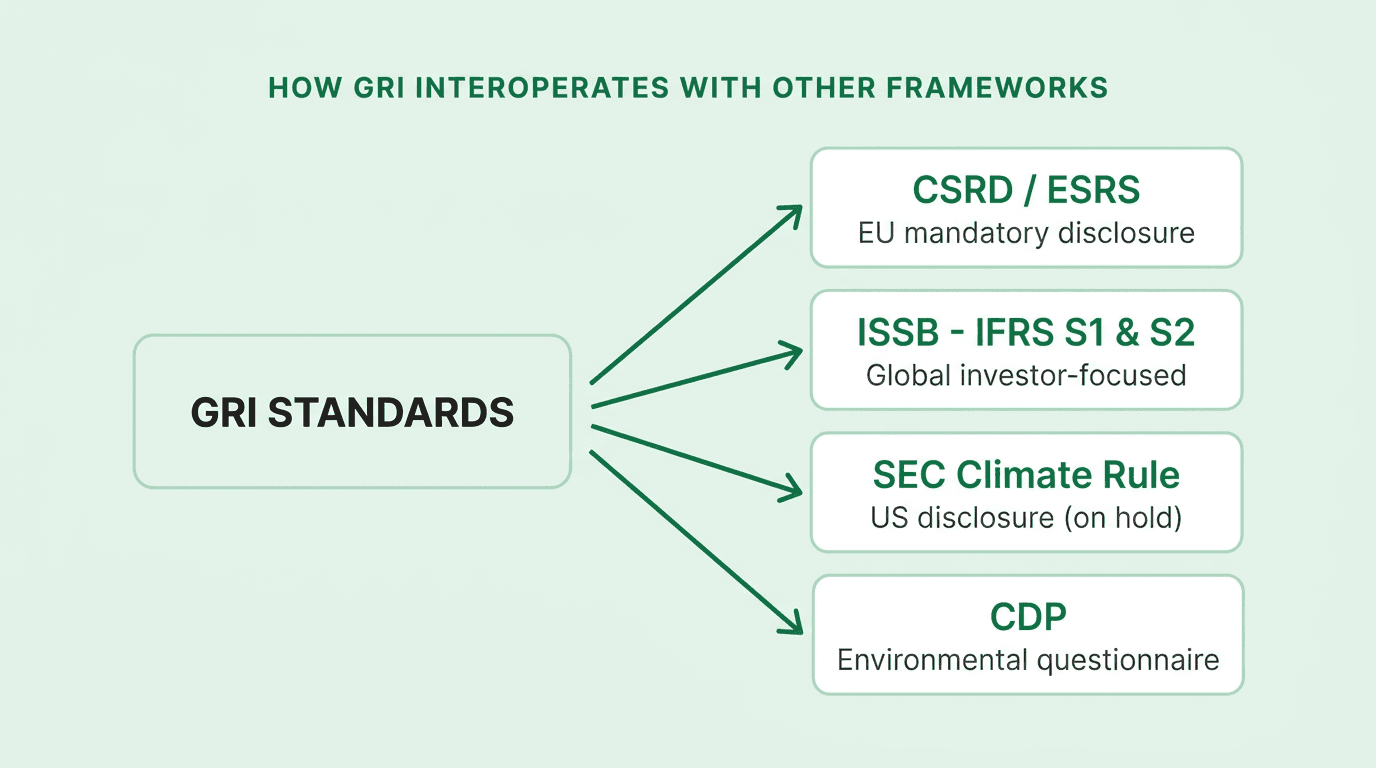

How GRI interoperates with CSRD, ESRS, ISSB, and SEC disclosures

GRI is voluntary, but its disclosures now feed directly into mandatory regimes through formal interoperability agreements.

ESRS (EU CSRD): The European Financial Reporting Advisory Group (EFRAG) and GRI published a joint statement on ESRS-GRI interoperability in 2024 confirming that a company reporting under the European Sustainability Reporting Standards (ESRS) is considered to be "reporting with reference to" the GRI Standards. The joint EFRAG-GRI Interoperability Index maps every ESRS disclosure requirement to the corresponding GRI disclosure. For the roughly 5,000 enterprises still inside the narrowed CSRD scope after the Omnibus I Directive, this means GRI data infrastructure is directly reusable for ESRS reporting and CSRD compliance.

ISSB (IFRS S1 and S2): GRI and the International Sustainability Standards Board signed a Memorandum of Understanding in March 2022 to coordinate standard-setting. The intent is a "two-pillar" global architecture: GRI covers impact materiality (organisation-to-world) and the ISSB covers financial materiality (world-to-organisation). The GSSB is aligning the revised GRI climate and energy standards with IFRS S1 and S2 so that a single dataset can serve both audiences.

SEC Climate Disclosure: The SEC's 2024 climate rule remains under a voluntary stay, but investor demand for climate disclosure has not receded. Many US-listed companies continue to publish GRI-aligned reports as the de-facto substitute — particularly for Scope 1, 2, and 3 emissions — while the legal path for the SEC rule is resolved.

Other frameworks: GRI is also explicitly aligned with CDP's climate questionnaire, the UK's Streamlined Energy and Carbon Reporting (SECR), the Science Based Targets initiative (SBTi), the UN Sustainable Development Goals, and the UN Global Compact. This is why most enterprise reporting stacks start from GRI even when a mandatory regime is the proximate driver.

The GRI reporting process: materiality, data collection, disclosure

A GRI report is not a questionnaire. It is produced through a four-step process defined in GRI 1 and GRI 3.

Context and stakeholder identification. The organisation maps its activities, business relationships, and stakeholder groups. Under GRI 3: Material Topics 2021, stakeholder identification is the starting point — not a formality.

Materiality assessment. The organisation identifies the sustainability topics on which it has the most significant actual or potential impacts on the economy, environment, and people. This is impact materiality — not the financial materiality of ISSB. Robust materiality assessment practice remains the weakest link in most reporters' workflow.

Data collection and validation. Quantitative disclosures (emissions, water withdrawal, waste, workforce composition) and qualitative disclosures (policies, governance, grievance mechanisms) are assembled from internal systems — ERP, HRIS, utility billing, travel, logistics — and from suppliers. This step is where most reporting projects fail or blow through budget without automated data collection.

Reporting and assurance. The organisation publishes the GRI content index showing which disclosures have been made and links them to the underlying evidence. Increasingly, reporters seek limited or reasonable external assurance on GHG emissions and material topics.

The choice of emission factor methodology — activity-based, production-based, or spend-based — determines how defensible Scope 1, 2, and 3 numbers will be under GRI 305 and the companion CSRD/ISSB disclosures.

Business benefits: capital access, risk management, stakeholder trust

GRI reporting is voluntary, but the payoff is structural rather than discretionary.

Capital access. Sustainable finance is now a primary channel for corporate capital. Investors, lenders, and rating agencies use GRI disclosures as an input to ESG reporting scores, index inclusion, and cost-of-capital pricing. Reporters that publish structured GRI data are easier to evaluate and cheaper to fund.

Risk management. A GRI-aligned materiality process forces an organisation to identify climate, social, and governance risks early — before they escalate into regulatory fines, litigation, or operational disruption. The same process drives cleaner decarbonisation planning because it identifies material emissions hotspots by business unit.

Stakeholder trust. GRI reports are public and comparable. That matters for recruiting, procurement (where customers increasingly require ESG data as a tender precondition), and regulated relationships — particularly for public-sector and national-infrastructure clients served by Net0's Government AI capability.

SDG and UNGC alignment. GRI disclosures map directly to the UN Sustainable Development Goals and the UN Global Compact Communication on Progress, which is relevant for reporters participating in multilateral programmes.

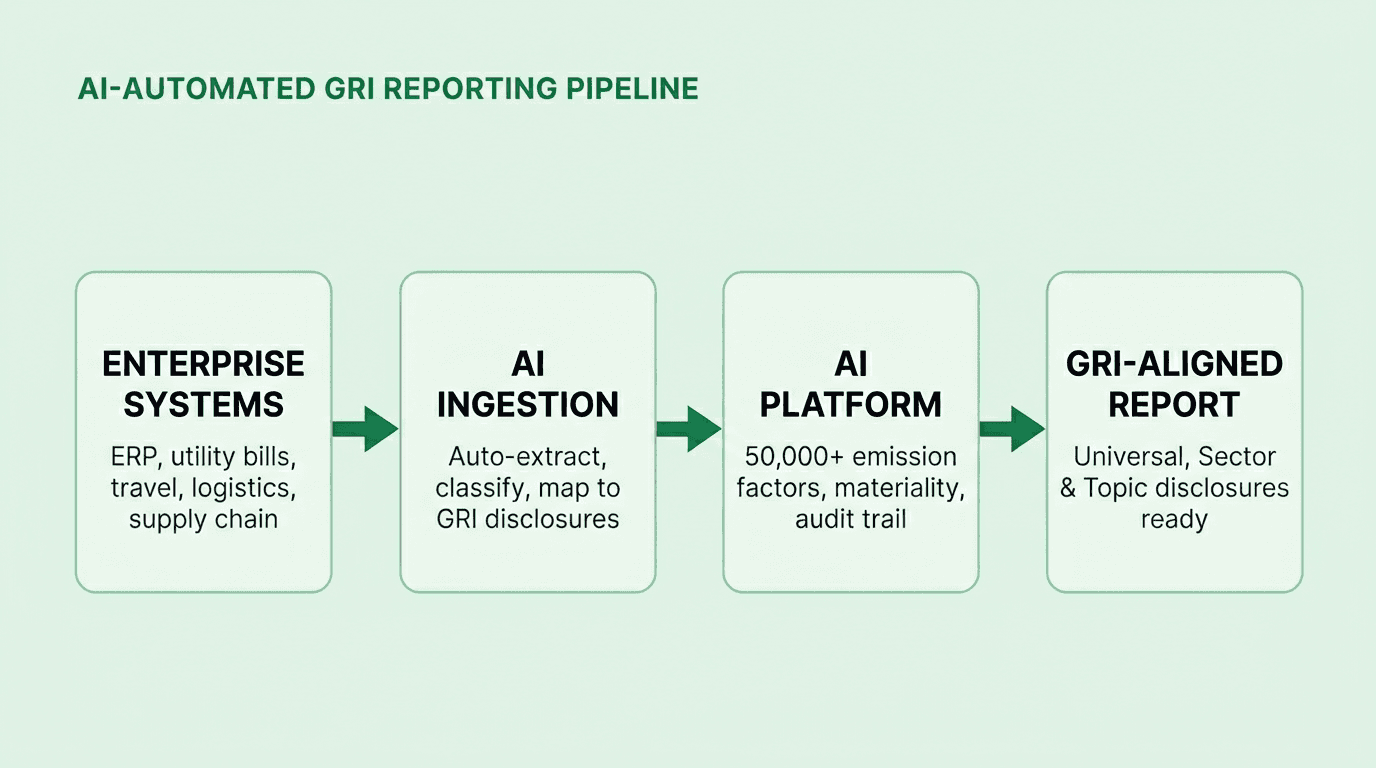

How AI transforms GRI reporting at enterprise scale

GRI reporting is a data problem. Most of the Topic Standards require quantitative disclosures across the full value chain — Scope 1, 2, and 3 emissions, water withdrawal by source, waste by disposal method, workforce composition, and more. Large enterprises typically have this data scattered across dozens of systems, multiple entities, and multiple geographies, in multiple units.

Net0 addresses this with AI-native infrastructure purpose-built for sustainability disclosure. The platform ingests structured and unstructured data from more than 10,000 enterprise systems, applies machine learning to classify and map each record to the correct GRI disclosure, and produces an audit-ready dataset that also powers ESRS, ISSB, CDP, and SECR reporting from the same evidence base. A full library of 50,000+ emission factors is maintained inside the platform so that activity data can be converted into GRI 305 emissions without external consultants.

This matters for reporting teams because the bottleneck is not writing the report — it is getting defensible numbers from source systems to the disclosure. Net0, as an AI infrastructure company building intelligent systems for governments and global enterprises, replaces the manual extraction, spreadsheet reconciliation, and framework rework that used to consume most of the reporting cycle.

Book a demo to see how Net0 automates GRI reporting and multi-framework disclosure for enterprise and public-sector reporters.

FAQ

What is the Global Reporting Initiative (GRI)?

The Global Reporting Initiative is an independent non-profit standards organisation headquartered in Amsterdam that develops the GRI Standards — the most widely used framework for voluntary sustainability reporting. More than 14,000 organisations across 100+ countries use GRI to disclose their impacts on the economy, environment, and people.

Who is required to report to GRI?

GRI reporting is voluntary — no regulator mandates it directly. However, GRI disclosures are integrated into mandatory regimes including the EU's CSRD/ESRS, the ISSB's IFRS S1 and S2, and multiple investor questionnaires. In practice, most large companies and many governments publish GRI-aligned reports because investors, lenders, and customers expect them.

How many GRI Standards exist?

The GRI Standards have three tiers: three Universal Standards (GRI 1, 2, 3), Sector Standards covering 40 priority sectors (of which GRI 11 Oil and Gas, GRI 12 Coal, GRI 13 Agriculture, and GRI 14 Mining are currently published), and Topic Standards organised into the 200 series (economic), 300 series (environmental), and 400 series (social).

What is the difference between GRI and CSRD?

GRI is a voluntary global impact-materiality framework. CSRD is an EU law that requires roughly 5,000 large companies to report using the European Sustainability Reporting Standards (ESRS). GRI and ESRS are formally interoperable: a company reporting under ESRS is considered to be reporting with reference to GRI, per the 2024 EFRAG-GRI joint statement of interoperability.

How does GRI interact with ISSB and ESRS?

GRI signed a Memorandum of Understanding with the ISSB in March 2022 to align standard-setting. The working model is a two-pillar global architecture: GRI covers impact materiality (the organisation's impact on the world), while ISSB's IFRS S1 and S2 cover financial materiality (the world's impact on the organisation). ESRS is interoperable with both.

How can AI automate GRI reporting?

AI automates the data-collection, classification, and framework-mapping steps that historically took months of manual work. Net0's platform ingests data from 10,000+ enterprise systems, applies machine learning to map each record to the correct GRI disclosure, converts activity data into emissions using a 50,000+ emission-factor library, and publishes audit-ready disclosures aligned with GRI, ESRS, ISSB, CDP, and SECR from a single evidence base.