AI for Sustainability

IFRS S1 and S2: The Global Sustainability Disclosure Standards Explained

IFRS S1 and S2 are the ISSB's global baseline for sustainability and climate-related financial disclosure, now mandatory across 19 jurisdictions. Net0's AI sustainability platform operationalises compliance at enterprise scale.

Sofia Fominova

Apr 19, 2026

TL;DR: IFRS S1 and IFRS S2 are the global baseline sustainability disclosure standards issued by the International Sustainability Standards Board (ISSB) on 26 June 2023. By April 2026, requirements in nearly 40 jurisdictions have either taken effect or been formally adopted — including the United Kingdom, Australia, Canada, Japan, Singapore, Hong Kong, Turkey, and Brazil — turning what began as a voluntary framework into the de facto global standard for investor-focused sustainability and climate reporting.

Key Takeaways

IFRS S1 and S2 have been effective for annual reporting periods beginning on or after 1 January 2024, according to the IFRS Foundation.

Nearly 40 jurisdictions have taken formal steps to adopt or align with the ISSB Standards, with requirements already in effect in 19 jurisdictions as of February 2026, per the IFRS Foundation's jurisdictional tracker.

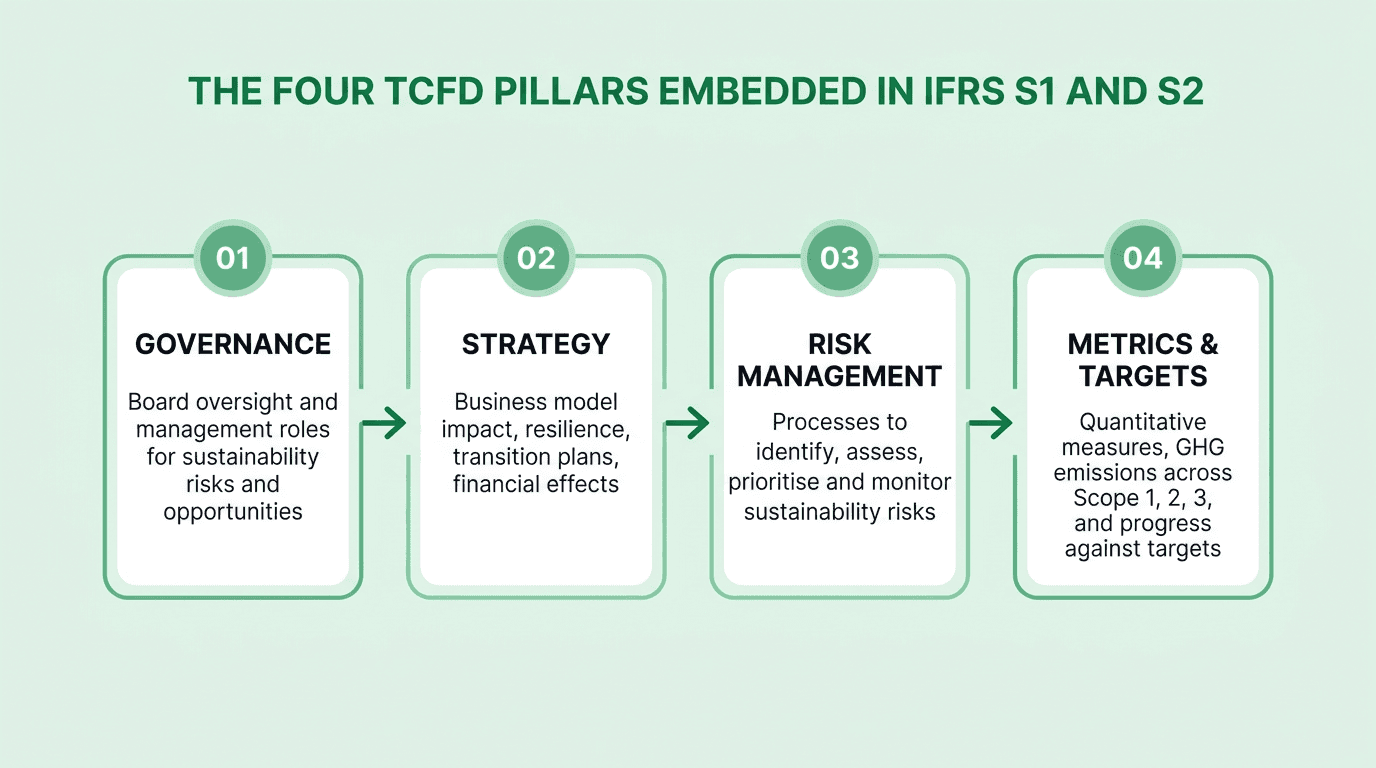

Both standards follow the four-pillar structure of the Task Force on Climate-Related Financial Disclosures (TCFD): Governance, Strategy, Risk Management, and Metrics & Targets.

IFRS S2 requires disclosure of Scope 1, Scope 2, and Scope 3 greenhouse gas emissions, with a first-year transition relief permitting companies to omit Scope 3.

The ISSB provides a climate-first relief allowing first-year reporters to limit disclosures to climate-related risks and opportunities under IFRS S2 before extending to the full IFRS S1 scope.

Introduction

Net0 is an AI infrastructure company that builds AI solutions for governments and global enterprises, including the sustainability platform used by Fortune 500 reporters to meet IFRS S1 and S2 obligations. IFRS S1 and S2 — the two inaugural standards from the International Sustainability Standards Board (ISSB) — now form the investor-focused global baseline for sustainability and climate-related financial disclosure. For finance and sustainability leaders, the key shift in 2026 is operational: the standards are no longer a forward-looking framework but a live reporting requirement across most of the world's largest capital markets.

This article explains what IFRS S1 and S2 require, how jurisdictions have adopted them, which transition reliefs are available, and how AI-powered sustainability platforms support compliance across overlapping frameworks such as CSRD, ESRS, and CDP.

What IFRS S1 and S2 Are

The IFRS Foundation established the ISSB at COP26 in November 2021 to consolidate investor-focused sustainability reporting into a single global baseline. The ISSB operates alongside the International Accounting Standards Board (IASB) and incorporates the prior work of the Task Force on Climate-Related Financial Disclosures (TCFD), the Value Reporting Foundation (SASB and Integrated Reporting), and the Climate Disclosure Standards Board (CDSB).

On 26 June 2023, the ISSB issued its first two standards:

IFRS S1 — General Requirements for Disclosure of Sustainability-related Financial Information

IFRS S2 — Climate-related Disclosures

Both standards are effective for annual reporting periods beginning on or after 1 January 2024, meaning the first reports under the standards appeared in investor filings during 2025. Companies must apply S1 and S2 together to claim compliance with IFRS Sustainability Disclosure Standards.

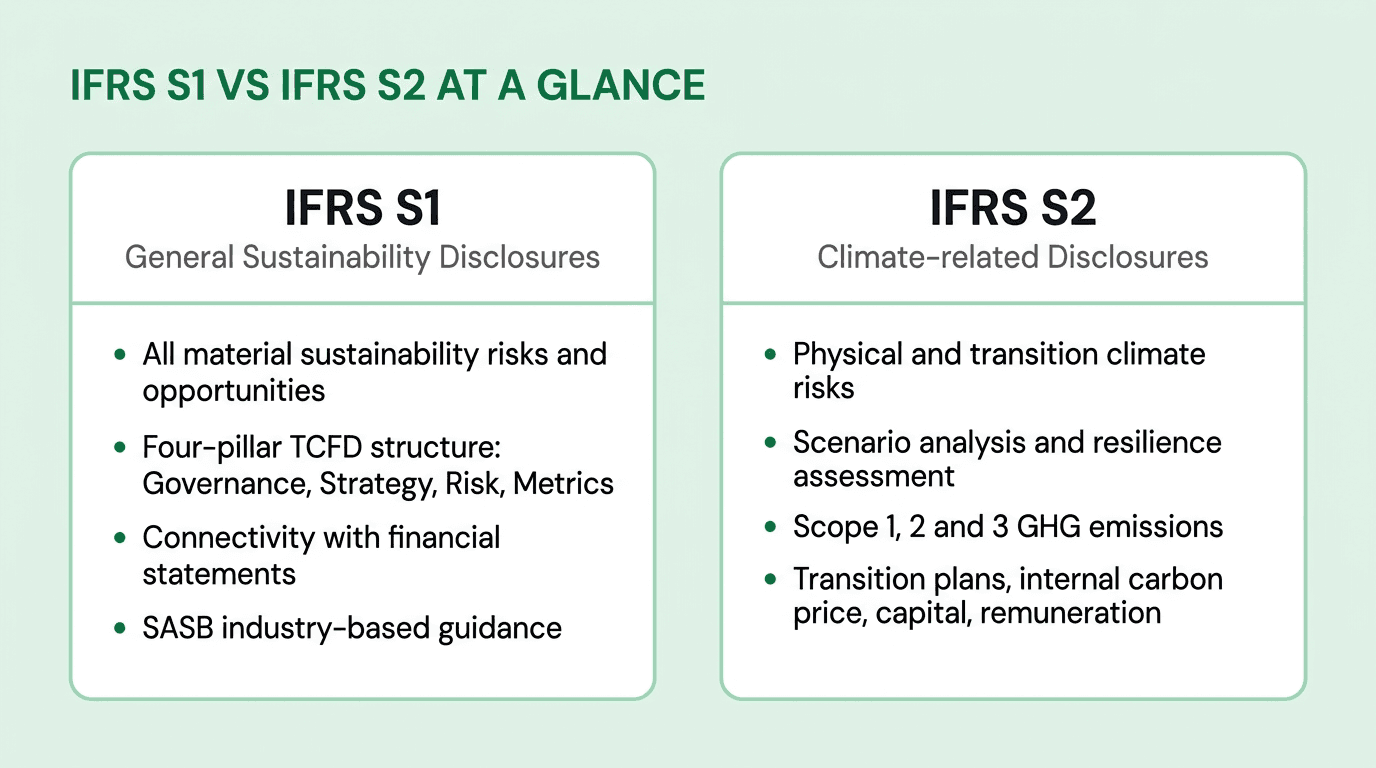

IFRS S1 — General Sustainability Disclosures

IFRS S1 sets the foundation for all sustainability-related financial disclosure. It requires entities to disclose material information about sustainability-related risks and opportunities that could reasonably be expected to affect cash flows, access to finance, or cost of capital over the short, medium, and long term.

Key features:

Full sustainability scope. S1 covers any sustainability topic — climate, water, biodiversity, human capital, supply chain — that is material to an entity's prospects.

Industry-based guidance. Entities are required to consider the SASB Standards and may also refer to CDSB application guidance, investor-focused pronouncements from other standard-setters, and the GRI and ESRS where relevant.

Connectivity with the financial statements. Sustainability-related disclosures must use consistent data, assumptions, and time horizons as the general-purpose financial statements they accompany.

Timing alignment. Disclosures must be published as part of the entity's general-purpose financial reports, released at the same time.

IFRS S2 — Climate-related Disclosures

IFRS S2 is the first topic-specific standard. It focuses exclusively on climate-related risks and opportunities and applies in conjunction with IFRS S1.

Core requirements include:

Physical and transition risk identification across short, medium, and long-term horizons.

Scenario analysis to evaluate climate resilience of the strategy and business model. First-year reporters may use qualitative scenario analysis, with quantitative analysis expected thereafter.

Cross-industry metrics, including Scope 1, 2, and 3 greenhouse gas emissions calculated in line with the GHG Protocol Corporate Standard, the amount of capital deployment toward climate-related risks and opportunities, the proportion of assets vulnerable to climate transition risk, internal carbon prices, and the percentage of executive remuneration linked to climate considerations.

Transition plans, where they exist, including reliance on carbon offsets.

Industry-based metrics aligned with 68 SASB industry categories.

Jurisdictional Adoption in 2026

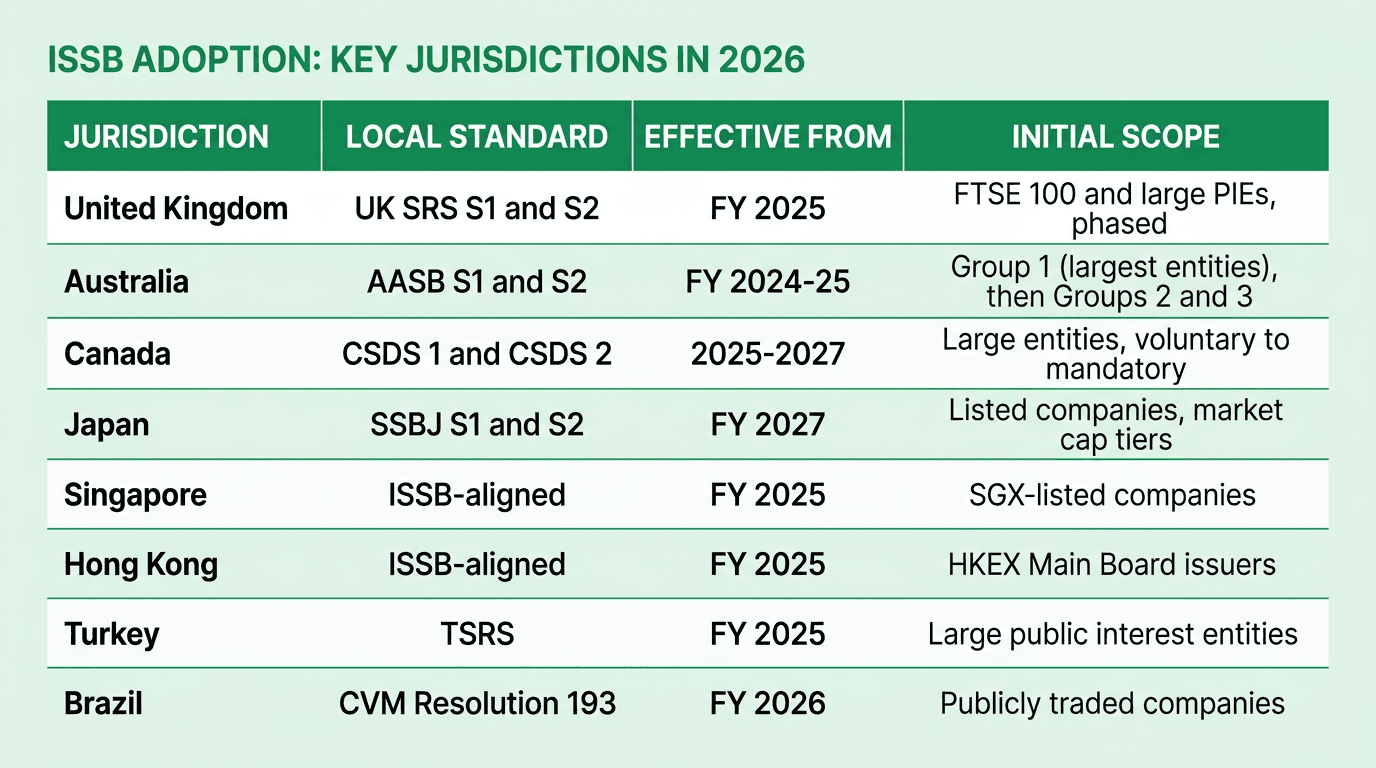

The ISSB standards began as a voluntary global baseline but have become the common technical core for mandatory regimes worldwide. According to the IFRS Foundation's February 2026 update, nearly 40 jurisdictions have now taken formal steps toward ISSB adoption, with live requirements in 19.

Key implementations:

United Kingdom — The UK Sustainability Reporting Standards (UK SRS) are ISSB-aligned with minor UK-specific amendments, effective from FY 2025 with a phased rollout targeting FTSE 100 constituents and large public interest entities first.

Australia — AASB S1 and AASB S2 were issued in September 2024. AASB S2 is mandatory; AASB S1 is voluntary. Group 1 (largest entities) reports from FY 2024-25, Group 2 from FY 2026-27, and Group 3 from FY 2027-28.

Japan — The Sustainability Standards Board of Japan (SSBJ) finalised ISSB-aligned standards in March 2025, with mandatory reporting beginning FY 2027 for the largest Prime Market listed companies, phased by market capitalisation.

Canada — The Canadian Sustainability Standards Board (CSSB) issued CSDS 1 and CSDS 2 for voluntary application from 2025, with mandatory requirements expected from 2027 under the Canadian Securities Administrators' framework.

Singapore and Hong Kong — Climate-related ISSB-aligned disclosures are mandatory for SGX-listed companies and HKEX Main Board issuers from FY 2025.

Turkey — The Turkish Sustainability Reporting Standards (TSRS) are mandatory for large public interest entities from FY 2025.

Brazil — The CVM (Comissão de Valores Mobiliários) Resolution 193 mandates ISSB-aligned disclosures for publicly traded companies from FY 2026.

The ISSB standards also interoperate with the EU's Corporate Sustainability Reporting Directive (CSRD) and the European Sustainability Reporting Standards (ESRS). In May 2024, the IFRS Foundation and EFRAG published interoperability guidance showing high alignment on climate disclosures. The SEC's 2024 climate rule remains stayed and under formal review, but most large US multinationals face IFRS-aligned reporting through foreign subsidiaries or listed parent entities.

Transition Reliefs for First-Year Reporters

Recognising the operational complexity of a global baseline, the ISSB built several reliefs into the standards for entities in their first annual reporting period under IFRS S1 and S2.

Climate-first relief. Entities may limit disclosures to climate-related risks and opportunities (IFRS S2) in the first year, deferring broader IFRS S1 sustainability topics to the second reporting period.

S1 extended timing. Entities may publish their sustainability-related financial disclosures after their general-purpose financial statements in the first year, with a cap aligned with the entity's interim reporting deadline.

Scope 3 exemption. Entities may omit Scope 3 emissions in the first year of applying IFRS S2, giving time to build out value chain data collection — a common bottleneck covered in depth in Net0's Scope 3 deep dive.

Qualitative scenario analysis. First-year reporters may conduct qualitative rather than quantitative climate resilience scenario analysis.

Comparative information relief. Entities are not required to disclose comparative information in the first year.

GHG Protocol method relief. Entities that used a method other than the GHG Protocol Corporate Standard in the immediately preceding period may continue with that method in the first reporting year under IFRS S2.

Why IFRS S1 and S2 Matter for Enterprises

Adoption of IFRS S1 and S2 changes three things for enterprise finance, sustainability, and investor relations teams.

First, sustainability data becomes auditable. IFRS S1 requires the same rigour, data lineage, and internal controls that apply to the financial statements. This raises the bar from narrative ESG reports to quantified, evidence-based disclosure with external assurance.

Second, the standards act as a translation layer across overlapping regimes. A company reporting under UK SRS, AASB S2, and CSRD can now align on a single data model and reconcile disclosures across filings — reducing duplication and cost. The common four-pillar TCFD architecture is reinforced by ISSB alignment with the CDP questionnaire, the SBTi framework, and the GRI Climate Change and Energy Topic Standard.

Third, investors are using IFRS S1 and S2 disclosures to price climate risk. According to the CDP 2025 disclosure data report, more than 24,800 organisations now report environmental data — increasingly structured around ISSB-aligned taxonomies — covering approximately two-thirds of global market capitalisation. Capital allocators have moved from asking whether a company reports to asking how material its disclosures are.

How Net0 Supports IFRS S1 and S2 Reporting

Net0 provides the AI infrastructure that enterprises use to operationalise IFRS S1 and S2 compliance at scale. The Net0 sustainability platform automates the data collection, calculation, and disclosure workflows that the standards now require.

Automated data ingestion from more than 10,000 enterprise systems — including ERP, finance, HR, procurement, energy management, and IoT platforms — removes the manual data gathering that makes first-year IFRS S2 reporting expensive.

50,000+ emission factors supporting activity-based, production-based, and spend-based calculation methodologies required for cross-industry and industry-specific metrics.

Scope 1, 2, and 3 coverage calculated to the GHG Protocol Corporate Standard and compatible with IFRS S2's cross-industry metric requirements, supported by the 15-category Scope 3 breakdown documented in Net0's Scope 3 guidance.

Multi-framework cross-mapping across IFRS S1/S2, CSRD/ESRS, CDP, GRI, SBTi, and 25+ additional frameworks, so a single underlying dataset serves multiple disclosures.

Scenario simulation and transition plans — including Marginal Abatement Cost (MAC) curve analysis that supports disclosure of capital deployment against climate-related opportunities.

Audit-ready evidence trails with immutable source linkage for every data point, designed to meet the assurance requirements now being introduced by securities regulators alongside IFRS S1/S2 adoption.

Net0 is trusted by Fortune 500 companies and governments worldwide across more than 400 entities on four continents, and supports 30+ sustainability reporting frameworks from a single AI-powered platform.

Book a demo to see how Net0 operationalises IFRS S1 and S2 compliance for global enterprises.

Frequently Asked Questions

Are IFRS S1 and S2 mandatory?

The ISSB standards themselves are a voluntary global baseline, but adoption has been made mandatory in most major economies. As of April 2026, IFRS S1/S2-aligned disclosures are required in the United Kingdom, Australia, Singapore, Hong Kong, Turkey, and Brazil, with Japan mandatory from FY 2027 and Canada phased through 2027. Approximately 40 jurisdictions have adopted or are adopting the standards.

What is the difference between IFRS S1 and IFRS S2?

IFRS S1 sets general requirements covering all material sustainability-related risks and opportunities, including environmental, social, and governance topics. IFRS S2 is the first topic-specific standard and focuses exclusively on climate-related disclosures, including Scope 1, 2, and 3 emissions, scenario analysis, and transition plans. Companies must apply S1 and S2 together to comply with IFRS Sustainability Disclosure Standards.

How do IFRS S1 and S2 relate to the TCFD?

Both standards are built on the four TCFD pillars: Governance, Strategy, Risk Management, and Metrics & Targets. The IFRS Foundation assumed monitoring responsibility for TCFD-aligned reporting in 2024, meaning IFRS S2 effectively replaces standalone TCFD disclosures. Companies reporting under IFRS S2 are considered to meet the TCFD recommendations.

Is Scope 3 required under IFRS S2?

Yes, IFRS S2 requires disclosure of Scope 1, Scope 2, and Scope 3 greenhouse gas emissions. However, the ISSB provides a first-year transition relief allowing companies to omit Scope 3 in the first reporting period under IFRS S2. Scope 3 must be disclosed from year two onward, calculated in line with the GHG Protocol Corporate Value Chain (Scope 3) Standard.

How does IFRS S2 compare to CSRD and ESRS?

IFRS S2 is an investor-focused, single-materiality climate standard. The EU's CSRD and its European Sustainability Reporting Standards use double materiality — covering both financial and impact materiality — and cover a broader scope including social and governance topics. The IFRS Foundation and EFRAG published interoperability guidance in 2024 showing high alignment on climate disclosures, meaning a single climate dataset can serve both regimes.

When do the first-year transition reliefs expire?

Transition reliefs apply only in the first annual reporting period in which an entity applies IFRS S1 and IFRS S2. From the second reporting period onward, entities must report full IFRS S1 sustainability scope, disclose Scope 3 emissions, publish comparative information, use quantitative scenario analysis where reasonably practicable, and apply the GHG Protocol Corporate Standard for emissions calculation.