AI for Sustainability

California Climate Disclosures SB 253 and SB 261: The 2026 Reporting Guide

Scope 1 and 2 disclosures under California SB 253 are due August 10, 2026 while SB 261 enforcement is stayed by the Ninth Circuit. A 2026 compliance guide from Net0.

Sofia Fominova

Apr 19, 2026

TL;DR: California's SB 253 (Climate Corporate Data Accountability Act) and SB 261 (Climate-Related Financial Risk Act) are the largest sub-national corporate climate disclosure laws in the United States. Following the September 2024 SB 219 amendments and CARB's final rulemaking on February 26, 2026, companies with more than USD $1 billion in global revenue must report Scope 1 and 2 emissions by August 10, 2026, with Scope 3 reporting beginning in 2027. SB 261 enforcement is currently stayed by a U.S. Ninth Circuit injunction pending a ruling on First Amendment challenges.

Key Takeaways

Over 10,000 companies doing business in California fall within the combined scope of SB 253 and SB 261, according to the California Air Resources Board (CARB).

August 10, 2026 is the first mandatory filing deadline under SB 253 for Scope 1 and 2 emissions, with Scope 3 disclosures beginning in 2027 on a schedule to be set by CARB.

SB 261 enforcement is temporarily paused following a Ninth Circuit injunction issued on November 18, 2025, with oral arguments heard January 9, 2026 and no decision deadline announced.

SB 219 (signed September 27, 2024) amended both laws to allow parent-level consolidated reporting and made third-party reporting organization contracts optional.

Penalties reach USD $500,000 per reporting year under SB 253 and up to USD $50,000 per year under SB 261 once enforcement resumes, according to the statutory text codified at Cal. Health & Safety Code §§ 38532-38533.

Introduction

Net0, an AI infrastructure company that builds AI solutions for governments and global enterprises, analyses California climate disclosures SB 253 and SB 261 as the most consequential sub-national corporate climate regime in the world's fifth-largest economy. The two laws, originally signed on October 7, 2023, have evolved materially since. Practitioners preparing for the August 10, 2026 SB 253 deadline must now work with the revised statutory text produced by SB 219, the final implementing regulations that CARB adopted unanimously on February 26, 2026, and the unresolved Ninth Circuit litigation over SB 261.

This guide synthesizes the current state of both laws, the distinctions between them, the operative deadlines, and the compliance steps enterprises should take to satisfy reporting obligations. For broader context on environmental disclosure frameworks, see Net0's AI-powered sustainability platform and its analysis of ESG reporting frameworks in 2026.

The 2026 Regulatory Reset for California Climate Disclosures

Three developments have reshaped SB 253 and SB 261 since they were signed:

SB 219 amendments (September 27, 2024). Signed by Governor Gavin Newsom, SB 219 made technical but consequential changes to both laws. Parent-level consolidated reporting is now permitted, meaning subsidiaries do not need to file separate reports. Contracting with a third-party emissions reporting organization became optional rather than mandatory, and the Scope 3 disclosure timeline moved from a fixed 180-day window to a schedule set by CARB rulemaking. SB 219 extended CARB's regulatory adoption deadline from January 1, 2025 to July 1, 2025, but did not extend the underlying reporting deadlines.

CARB final regulations (February 26, 2026). The California Air Resources Board unanimously approved the initial rulemaking package implementing both laws on February 26, 2026, following a December 2025 proposed rule and multiple public comment periods. The final regulations narrowly mirror the December proposal, establishing reporting entity definitions, data collection thresholds, and assurance schedules.

Ninth Circuit injunction on SB 261 (November 18, 2025). The U.S. Court of Appeals for the Ninth Circuit issued a temporary injunction blocking enforcement of SB 261 while allowing SB 253 enforcement to proceed. The injunction responds to First Amendment challenges led by the U.S. Chamber of Commerce and ExxonMobil, who argue that the disclosure mandates constitute compelled speech. Oral arguments were heard on January 9, 2026; as of this update, no decision deadline has been announced.

At a March 23, 2026 workshop, CARB signalled enforcement flexibility for the August 10, 2026 SB 253 deadline: companies may report using data they were already collecting as of December 2024, limited assurance is not required for 2026 reporting, and entities without available data may submit a compliance statement in lieu of a full report. CARB indicated it will not pursue enforcement actions against good-faith compliance efforts.

SB 253 — The Climate Corporate Data Accountability Act (CCDAA)

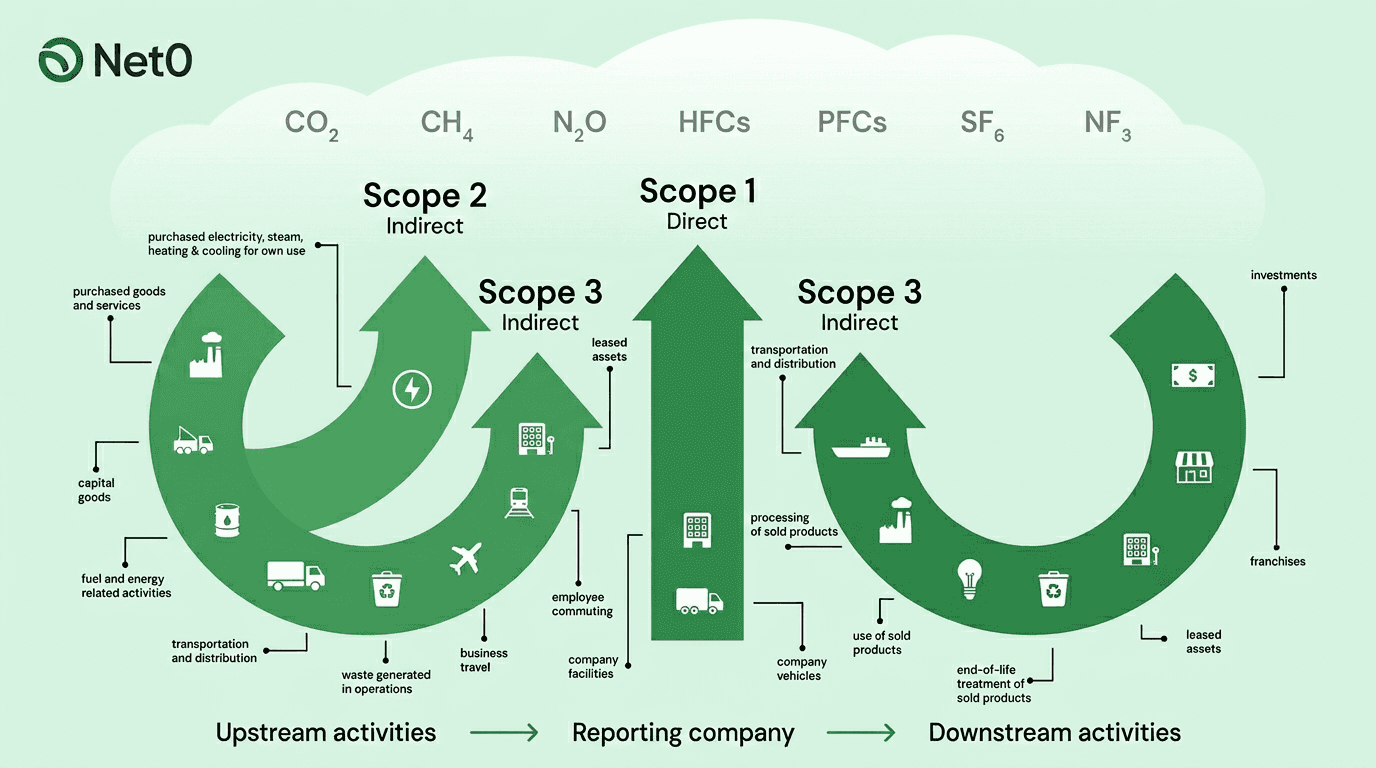

SB 253 requires companies formed under the laws of any U.S. state that do business in California and generate more than USD $1 billion in total global annual revenue to disclose Scope 1, 2, and 3 greenhouse gas emissions. According to CARB's adopted regulations, approximately 5,300 reporting entities meet the threshold.

Emissions reporting follows the GHG Protocol Corporate Accounting and Reporting Standard, the same standard that underpins most major disclosure regimes worldwide. The GHG Protocol distinguishes between three emission scopes — direct operational emissions (Scope 1), purchased energy (Scope 2), and value chain emissions (Scope 3) — as shown below:

For a detailed treatment of each scope, see Net0's guide to Scope 1, 2, and 3 emissions and the dedicated Scope 3 deep-dive.

SB 253 Reporting Schedule

August 10, 2026 — First Scope 1 and Scope 2 emissions report due, covering fiscal year 2025 data. Limited assurance is not required in this first cycle.

2027 — Scope 3 emissions reporting begins on a CARB-set schedule (replacing the original 180-day window under SB 219). Limited assurance may be required from 2027 for some entities.

2030 — Reasonable assurance required for Scope 1 and 2, raising the audit bar from limited assurance.

Emissions disclosures must be independently verified and submitted to a public digital registry that CARB will contract out. The registry will allow investors, regulators, and the public to analyse reported data across disclosing entities.

SB 253 Penalties

Under Cal. Health & Safety Code § 38532(e), violations of SB 253 can incur administrative penalties up to USD $500,000 per reporting year. CARB may consider good-faith efforts and remediation steps when determining penalty amounts.

For enterprises that already apply GHG reporting frameworks such as CDP or TCFD, much of the underlying emissions data will already exist. For those without a mature emissions inventory, Net0 has outlined the primary data sources and automated collection strategies that make first-year SB 253 compliance achievable.

SB 261 — The Climate-Related Financial Risk Act (CRFRA)

SB 261 requires companies formed under U.S. state law that do business in California and generate more than USD $500 million in total global annual revenue to publish biennial reports on climate-related financial risk. The original deadline for the first report was January 1, 2026.

The law tracks the disclosure architecture recommended by the Task Force on Climate-related Financial Disclosures (TCFD), whose four pillars — governance, strategy, risk management, and metrics and targets — have since been folded into the International Sustainability Standards Board's IFRS S1 and S2 standards. Covered entities must disclose climate-related risks across physical and transition categories, governance structures for oversight, scenario analysis, and the financial implications for operations and capital planning.

The SB 261 Injunction and Current Status

Following the Ninth Circuit's November 18, 2025 injunction, SB 261 compliance is currently voluntary. The lawsuit brought by the U.S. Chamber of Commerce, ExxonMobil, and other plaintiffs argues that the statute compels speech in violation of the First Amendment and conflicts with federal securities law. The same plaintiff coalition unsuccessfully sought to enjoin SB 253 on identical grounds.

At the January 9, 2026 oral arguments, the panel focused on whether the required disclosures qualify as commercial speech subject to lesser First Amendment scrutiny and whether the state has a substantial interest in mandating the reports. According to Reuters' April 2026 reporting, the outcome could shape the viability of state-level climate disclosure regimes beyond California.

What Companies Should Do During the SB 261 Stay

Companies in scope should continue to prepare reports as though the law were in force. CARB has adopted final regulations, deadlines may be reinstated on short notice if the injunction is lifted, and investors increasingly expect TCFD- or ISSB-aligned climate risk disclosure regardless of regulatory status. Much of the underlying analysis — scenario modelling, governance documentation, transition risk quantification — is already required for voluntary frameworks such as CDP reporting and the European Sustainability Reporting Standards (ESRS).

SB 261 Penalties

Violations of SB 261, once enforcement resumes, carry administrative penalties of up to USD $50,000 per reporting year for failing to submit a report or failing to publish it on the company's website, per Cal. Health & Safety Code § 38533(g).

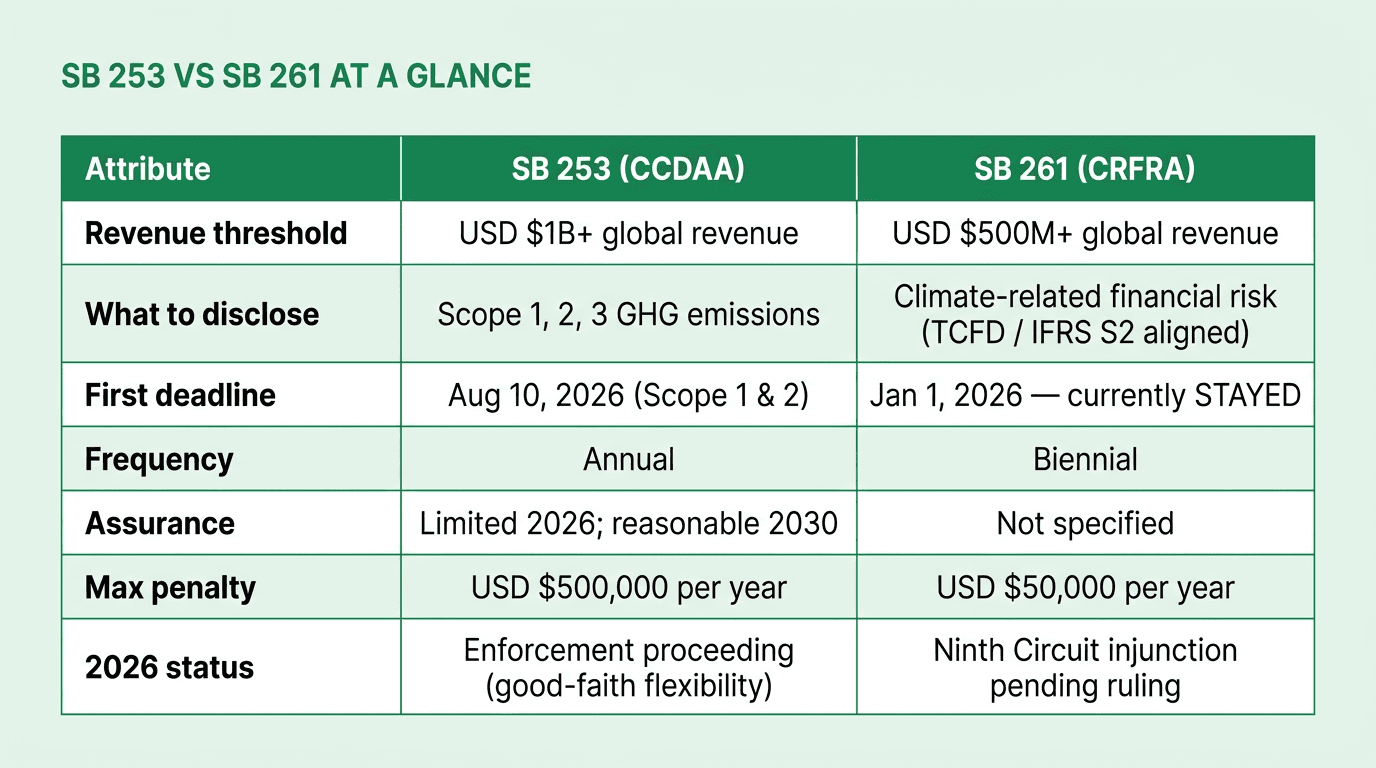

SB 253 and SB 261 Compared

The two laws operate on different thresholds, cover different subject matter, and impose different penalty structures. The table below summarises the principal differences:

Because the SB 261 revenue threshold (USD $500M) is lower than the SB 253 threshold (USD $1B), a meaningful cohort of companies falls under SB 261 alone. Collecting the Scope 1, 2, and 3 emissions data required for SB 253, however, is foundational for producing a defensible SB 261 climate-risk report — strategies, transition plans, and opportunity assessments cannot be substantiated without underlying emissions data.

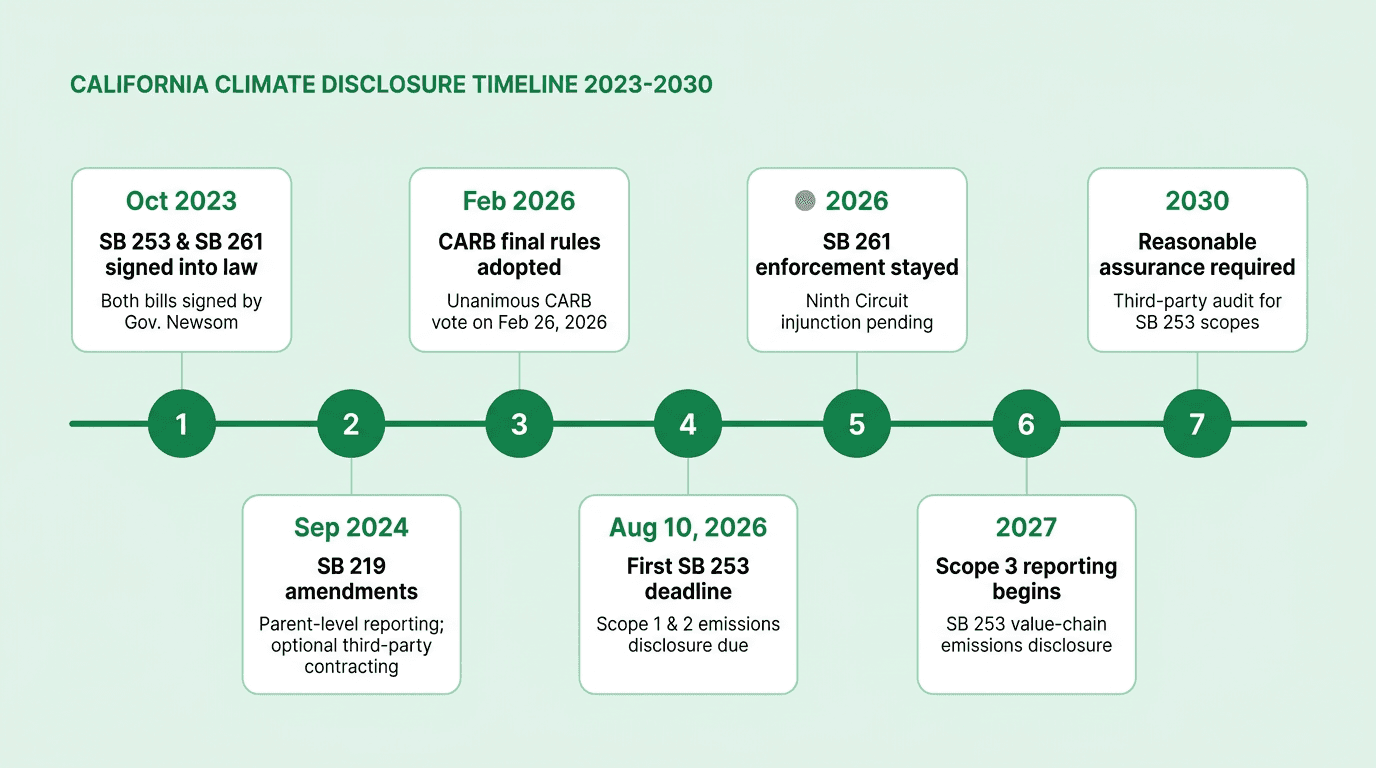

California Climate Disclosure Timeline

The enforcement and regulatory milestones for SB 253 and SB 261 span from the original October 2023 signing through the 2030 reasonable-assurance requirement:

Compliance Preparation for the August 10, 2026 Deadline

Four preparation workstreams separate companies ready to file from those at risk of exceeding the deadline.

1. Scope boundary determination. The final regulations require reporting entities to define their organizational boundary using either the equity share or financial control approach under the GHG Protocol. SB 219's consolidation provisions allow a parent to file on behalf of subsidiaries, which can reduce administrative overhead for multi-entity enterprises.

2. Data collection and emission factor alignment. The CARB final rules accept 2025 fiscal year data collected under existing processes. Companies without mature inventories should prioritise automated ingestion from ERP, utility, and procurement systems, mapped to recognised emission factors using a defensible hierarchy — activity-based over spend-based wherever primary data is available.

3. Assurance readiness. Limited assurance is not required for the first SB 253 cycle, but is required from 2027 for some reporters and reasonable assurance is required from 2030. Building auditable data lineage and documented methodologies now reduces the remediation burden in later cycles. See Net0's analysis of carbon accounting methodologies for the structured approaches auditors expect.

4. Governance and disclosure infrastructure. SB 261 reports (once the injunction is lifted) require board-level oversight documentation, risk management process disclosure, and scenario analysis — the same architecture that supports Science Based Targets initiative (SBTi) validation, ISSB-aligned disclosures, and CSRD reporting. Consolidating governance disclosures across frameworks reduces duplicative work.

Companies already preparing for the EU Carbon Border Adjustment Mechanism (CBAM) or disclosing product carbon footprints will find significant overlap with SB 253 requirements, particularly on Scope 3 and upstream value-chain data. See also Net0's framework for upstream supplier emissions reduction and decarbonization planning.

How Net0 Supports SB 253 and SB 261 Compliance

Net0 is an AI infrastructure company whose AI-powered sustainability platform serves enterprises and governments across more than 400 entities on four continents. The platform automates the emissions data collection, calculation, and reporting workflow that SB 253 and SB 261 require.

Automated data ingestion across 10,000+ enterprise systems. Net0 connects to ERP systems, utility portals, travel and expense platforms, supplier data feeds, and operational IoT infrastructure to ingest raw activity data continuously. This eliminates the manual spreadsheet workflows that dominate first-year disclosure programs and creates the audit trail required for limited and reasonable assurance engagements.

50,000+ recognised emission factors. Net0 maps activity data to emission factors from the GHG Protocol, the U.S. EPA, the UK DEFRA, and the IPCC's AR6 report, with provenance captured for every calculation. The platform supports activity-based, spend-based, and hybrid calculation methods, allowing reporters to match the data hierarchy expected by CARB's final rules and by limited-assurance auditors.

30+ reporting frameworks in a single pipeline. Once emissions are calculated, the same underlying data produces disclosures aligned with CARB's SB 253 registry format, CDP, GRI, TCFD/IFRS S2, ESRS, the SBTi V2 standard, the federal SEC climate disclosure rule, and other regimes. Companies subject to CSRD reporting, the SEC climate disclosure rule, or GRI standards can reuse the same data spine for SB 253 and SB 261 outputs.

Scenario modelling and governance disclosures. Net0 includes scenario simulation and marginal abatement cost curve tooling to support the transition-risk and opportunity analysis that SB 261 (and the aligned IFRS S2 standard) demand, along with governance audit trails that evidence board oversight.

Book a demo to see how Net0 streamlines California climate disclosure compliance across SB 253 and SB 261 alongside every other major disclosure framework.

Frequently Asked Questions

Does SB 253 still apply if SB 261 is paused?

Yes. The Ninth Circuit's November 2025 injunction stayed SB 261 only. SB 253 enforcement is proceeding on the original schedule, and CARB adopted the final SB 253 rules on February 26, 2026. Companies above the USD $1 billion revenue threshold must prepare to file Scope 1 and 2 emissions disclosures by August 10, 2026.

Which companies must report under SB 253?

SB 253 applies to companies formed under the laws of any U.S. state that do business in California and generate more than USD $1 billion in total annual global revenue. CARB estimates approximately 5,300 reporting entities meet the threshold. Subsidiaries may be covered by a parent-level consolidated report under the SB 219 amendments.

When is the first SB 253 deadline?

August 10, 2026 is the initial filing deadline for Scope 1 and Scope 2 emissions covering fiscal year 2025 data. Scope 3 emissions reporting begins in 2027 on a schedule to be set by CARB. Reasonable assurance for Scope 1 and 2 is required from 2030.

How does SB 219 change SB 253 and SB 261?

SB 219, signed September 27, 2024, allowed parent-level consolidated reporting, made third-party emissions reporting organization contracts optional rather than mandatory, and replaced the fixed 180-day Scope 3 disclosure window with a CARB-set schedule. SB 219 did not extend the underlying reporting deadlines for either law.

Is SB 261 reporting required in 2026?

No. Following the Ninth Circuit's November 18, 2025 injunction, SB 261 enforcement is stayed pending a First Amendment ruling. Many in-scope companies continue to prepare reports voluntarily, as deadlines may be reinstated and investors expect TCFD- or ISSB-aligned climate-risk disclosures regardless of enforcement status.

What are the penalties for non-compliance?

SB 253 violations can incur administrative penalties up to USD $500,000 per reporting year under Cal. Health & Safety Code § 38532(e). SB 261 violations, once enforcement resumes, carry penalties up to USD $50,000 per reporting year under § 38533(g) for failing to submit or publish the required climate-related financial risk report.

How do SB 253 and SB 261 interact with federal disclosure rules?

The federal SEC climate disclosure rule was finalized in March 2024 but has not taken effect, and its status remains uncertain. California's laws therefore represent the most consequential U.S. corporate climate disclosure regime currently in operation. See Net0's analysis of the SEC climate disclosure rule for the federal context.