AI for Sustainability

Carbon Management Glossary: 120+ Terms Explained (2026)

An alphabetical reference of 120+ carbon accounting, reporting and net-zero terms every sustainability leader should know in 2026.

Sofia Fominova

Apr 22, 2026

TL;DR: A carbon management glossary is a reference of the terms that appear across emissions accounting, sustainability reporting, net-zero strategy and climate regulation. This 2026 edition from Net0 covers 100+ definitions used by sustainability, finance and compliance teams operating under CSRD, IFRS S1 and S2, SBTi, the SEC climate rule and the GHG Protocol.

Key Takeaways

Over 100 carbon management, reporting and net-zero terms, defined in plain enterprise English and arranged strictly A-Z.

Updated for 2026: CSRD Wave 1 first reports filed in 2025, IFRS S1 and S2 adoption in 35+ jurisdictions, the absorption of TCFD into ISSB, and California SB-253 and SB-261 entering force.

Each definition is self-contained for quick reference and designed to be copy-pasted into internal training, tender documents and sustainability onboarding decks.

Terms are linked to longer explainers on the Net0 AI-powered sustainability platform where a deeper reference exists.

Six visual explainers cover Scope 1-4, accounting methodologies, the reporting framework ecosystem, offsets vs removals vs insetting, and nature-based vs engineered sequestration.

Introduction

Net0 is an AI infrastructure company that builds AI solutions for governments and global enterprises, with a dedicated AI-powered sustainability platform used by Fortune 500 companies and public-sector institutions across four continents. This carbon management glossary is one of the reference assets the platform's users rely on when standardising terminology across sustainability, finance, procurement and compliance.

The 2022 version of this glossary has been rewritten end-to-end for 2026. Obsolete entries were removed (the EU's Non-Financial Reporting Directive has been superseded by CSRD, TCFD has folded into ISSB, the "two-degree" framing has been replaced by 1.5 C in mainstream policy), and 35+ new entries were added to cover frameworks and concepts that became material after 2023 -- IFRS S1 and S2, ESRS, the SEC climate rule, California SB-253 and SB-261, CSDDD, PCAF financed emissions, internal carbon pricing, transition plans, TNFD and the SBTi Net-Zero Standard among them.

How to use this glossary

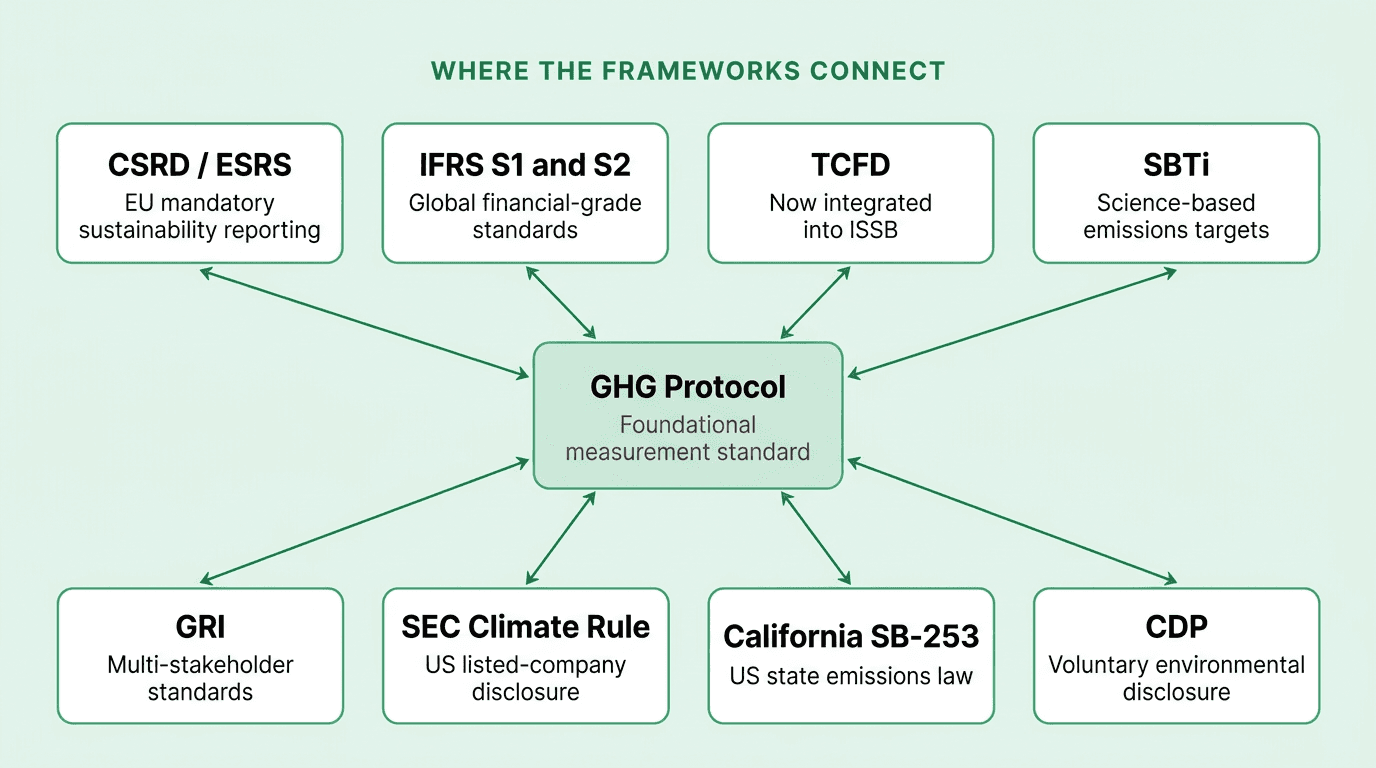

The entries below are arranged alphabetically. Where a term has a dedicated Net0 explainer -- for example Scope 1, 2 and 3 emissions, the GHG Protocol, ESRS or IFRS S1 and S2 -- the term is linked inline. Most frameworks do not exist in isolation: they build on the GHG Protocol measurement standard and feed into each other, as shown below.

A

Activity data

Activity data is the physical measurement of an action that generates emissions -- litres of diesel burned, kilowatt-hours of electricity consumed, tonne-kilometres of freight moved. It is the numerator in the emission-factor equation (activity x emission factor = emissions). Activity data produces more accurate emissions estimates than spend-based proxies because it reflects the real physical driver rather than a monetary estimate.

Additionality

Additionality is the principle that a carbon reduction or removal project must deliver an environmental benefit that would not have occurred without the carbon-finance intervention. A solar farm that would have been built anyway under existing subsidies fails the additionality test. Credible carbon credit standards (VCS, Gold Standard, ACR) require projects to demonstrate additionality through baseline scenario analysis before issuance.

Afforestation

Afforestation is the establishment of forest on land that has not been forested for at least the past 50 years, distinguishing it from reforestation of recently cleared land. It sequesters carbon through photosynthesis and biomass accumulation, and is classified as a nature-based solution under the GHG Protocol and IPCC methodologies. Afforestation projects may generate carbon credits but are subject to permanence and leakage risks.

AI in carbon management

AI in carbon management is the use of machine learning and generative AI to automate the collection, classification and analysis of emissions data. Applied to sustainability data and intelligence, AI extracts emissions-relevant information from invoices, utility bills, travel systems and supplier documents, matches activities to the correct emission factor, and flags anomalies. It compresses multi-month manual accounting cycles into continuous data flows.

Air pollution

Air pollution is the release of particulates and reactive gases (NOx, SOx, VOCs, PM2.5, PM10) that degrade air quality and public health. While not all air pollutants are greenhouse gases, many share sources with carbon emissions -- notably fossil-fuel combustion. Carbon reduction measures that displace fossil fuels typically deliver co-benefits for air quality, which is why air quality appears in CSRD's ESRS E2 pollution standard.

Air Quality Index (AQI)

The Air Quality Index (AQI) is a 0-500 scale used by national agencies (US EPA, UK Defra, China MEE) to translate measured concentrations of PM2.5, PM10, ozone, NO2, SO2 and CO into a single health-risk rating. AQI is not itself a carbon metric, but enterprise sustainability teams track it alongside emissions because indoor and outdoor air quality is reportable under ESRS E2 and several occupational health frameworks.

Anthropogenic

Anthropogenic describes any process, emission or environmental change caused by human activity. The IPCC attributes the majority of post-industrial global warming to anthropogenic greenhouse gas emissions, primarily from fossil-fuel combustion, industry, agriculture and land-use change. The term is used to distinguish human-driven climate change from natural climate variability in scientific and regulatory documents.

Assurance

Assurance is independent third-party verification that reported sustainability information is accurate. Limited assurance is a lower level of scrutiny expressed as negative confirmation ("nothing has come to our attention..."). Reasonable assurance approaches financial-audit rigour. CSRD requires limited assurance on first reports and reasonable assurance from 2028. SEC and ISSB frameworks are on similar trajectories.

B

Base year

The base year is the reference period against which future emissions reductions are measured. GHG Protocol guidance requires companies to fix a base year, document the boundary and recalculate it when structural changes (mergers, divestitures, methodology updates) shift emissions by more than a materiality threshold, typically 5%. SBTi approved targets are almost always expressed as a percentage reduction from a stated base year.

Biochar

Biochar is a carbon-rich solid produced by heating biomass in a low-oxygen environment (pyrolysis). Because the carbon is structurally stable, biochar applied to soil can sequester CO2 for centuries while improving water retention and fertility. It is one of the more durable carbon removal pathways recognised by VCS and Puro.earth methodologies, sitting between nature-based and engineered removal in permanence terms.

Biodiversity

Biodiversity is the variety of plant, animal and microbial life in an ecosystem. It is a material environmental topic in its own right under ESRS E4 and TNFD, and it interacts with carbon management: nature-based carbon projects can support or damage biodiversity depending on design (monoculture plantations score poorly). CSRD-reporting companies must disclose biodiversity-related impacts, dependencies, risks and opportunities.

Biofuel

A biofuel is a liquid or gaseous fuel derived from biomass -- ethanol from sugar, biodiesel from oils, biogas from digestion. Under the GHG Protocol, the biogenic CO2 from combusting certified sustainable biofuels is reported separately and not counted toward Scope 1 fossil emissions, provided full life-cycle analysis shows genuine net reductions versus fossil alternatives. Poorly sourced biofuels can exceed the emissions of the fuels they replace.

Biomass and biogas

Biomass refers to organic material used as an energy source; biogas is the methane-rich mixture produced when biomass breaks down anaerobically. Both are counted as renewable when feedstocks are managed sustainably. They play a key role in decarbonising sectors that are difficult to electrify -- heavy industry, heat networks, long-haul transport -- but require rigorous life-cycle accounting to avoid overstating their climate benefit.

Blue carbon

Blue carbon is the carbon stored in coastal and marine ecosystems -- mangroves, seagrasses, salt marshes and tidal wetlands. Per unit area, mangroves can sequester up to four times more carbon than terrestrial tropical forests, according to the IPCC Special Report on Oceans and Cryosphere. Blue carbon is recognised by the UNFCCC as a mitigation pathway, and credits are issued under VCS's VM0033 methodology.

C

California Climate Disclosure Laws (SB-253 and SB-261)

California Senate Bills 253 and 261, signed in 2023, require companies doing business in California with annual revenue above defined thresholds to disclose Scope 1, 2 and 3 emissions (SB-253) and climate-related financial risks (SB-261). California's climate disclosure laws apply to an estimated 10,000+ US and international companies and represent the first broad US state-level mandatory emissions disclosure regime.

Cap and trade

Cap and trade is a market-based policy that caps total emissions from a regulated sector and issues tradable allowances equal to the cap. Regulated entities must surrender one allowance per tonne of CO2e emitted, buying from the market if they exceed their allocation. The EU Emissions Trading System is the largest cap-and-trade market, followed by California, the UK ETS, South Korea and China's national scheme launched in 2021.

Carbon accounting

Carbon accounting is the process of measuring, tracking and reporting an organisation's greenhouse gas emissions in tonnes of CO2-equivalent. It follows the GHG Protocol Corporate Standard across Scope 1, 2 and 3, and increasingly uses activity-level data pulled directly from ERP, utility and supply-chain systems. Robust carbon accounting is the foundation for SBTi targets, CSRD, IFRS S1 and S2, CDP and SEC disclosures.

Carbon Border Adjustment Mechanism (CBAM)

The Carbon Border Adjustment Mechanism (CBAM) is an EU policy that prices the embedded carbon of imports in covered sectors (iron, steel, aluminium, cement, fertilisers, electricity, hydrogen). It entered a transitional reporting phase in October 2023 and shifts to financial obligations from 2026. CBAM aims to neutralise the risk of carbon leakage as EU ETS prices rise and to extend climate pricing to global trade.

Carbon budget

A carbon budget is the cumulative volume of CO2 that can still be emitted while retaining a given probability of staying below a warming threshold. The IPCC's Sixth Assessment Report put the remaining budget for a 50% chance of 1.5 C at around 500 GtCO2 from the start of 2020, shrinking rapidly at current emission rates. Carbon budgets inform both national NDCs and corporate SBTi target-setting.

Carbon capture and storage (CCS)

Carbon capture and storage (CCS) is the separation of CO2 from industrial flue gases or process streams, its transport, and its injection into deep geological formations for long-term storage. The IEA's 2023 CCUS outlook identified more than 40 operational facilities with total capture capacity of 50 MtCO2 per year. CCS is classified by the IPCC as a mitigation technology, distinct from direct air capture, which removes CO2 already in the atmosphere.

Carbon credit

A carbon credit is a tradable certificate representing one tonne of CO2e reduced, avoided or removed from the atmosphere through a verified project. Credits are issued under standards such as Verra's VCS, the Gold Standard and ACR, and traded on voluntary or compliance markets. A single credit can only be retired once; trustworthy markets depend on independent certification, public registries and robust additionality and permanence criteria.

Carbon dioxide (CO2)

Carbon dioxide (CO2) is the most abundant human-emitted greenhouse gas, produced by burning fossil fuels, cement manufacturing, deforestation and a range of industrial processes. Atmospheric CO2 concentration passed 420 ppm in 2023, up from a pre-industrial baseline near 280 ppm (NOAA Global Monitoring Laboratory). CO2 is the reference gas for global warming potential calculations -- other GHGs are expressed as CO2-equivalents.

Carbon dioxide equivalent (CO2e)

Carbon dioxide equivalent (CO2e) is a unified unit that converts any greenhouse gas into the mass of CO2 that would cause the same warming effect over a specified horizon, typically 100 years. Methane's 100-year GWP is 27-30; nitrous oxide is 273; SF6 exceeds 25,000 (IPCC AR6). CO2e allows companies to aggregate multiple gases into a single reported emissions figure.

Carbon emissions

Carbon emissions are releases of CO2 and other greenhouse gases into the atmosphere from human activity. In corporate reporting, "carbon emissions" is frequently used as shorthand for all GHGs converted into CO2e, even when gases other than CO2 are involved. Total anthropogenic emissions reached 53 GtCO2e in 2023, with energy production, industry and land-use change as the largest contributors (IEA World Energy Outlook 2024).

Carbon footprint

A carbon footprint is the total greenhouse gas emissions attributable to a defined entity -- an organisation, a product, an event, a building or an individual -- measured in CO2e. Corporate carbon footprints follow the GHG Protocol Scope 1/2/3 structure; product carbon footprints follow ISO 14067 and the GHG Protocol Product Standard, assessed through life-cycle methodology.

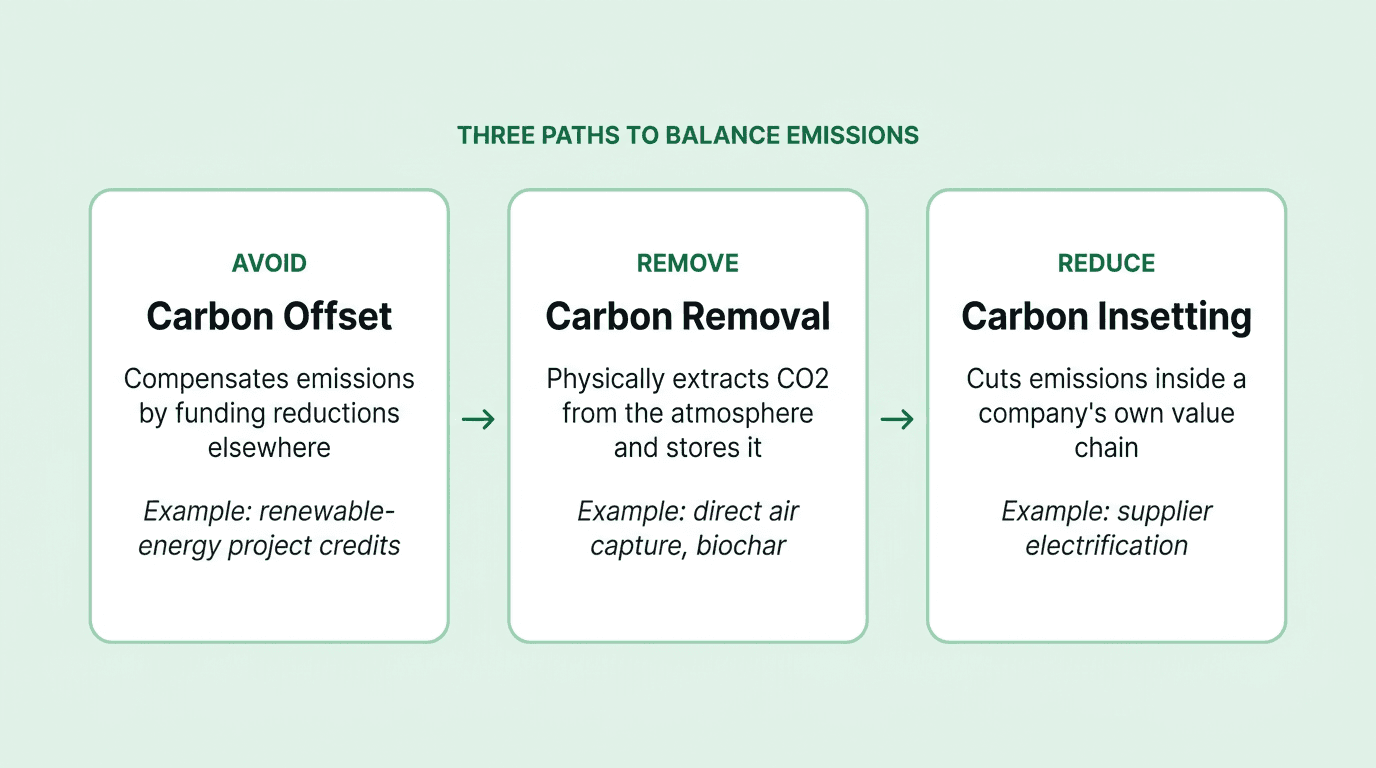

Carbon insetting

Carbon insetting is the practice of investing in emissions reductions inside a company's own value chain rather than purchasing external offsets. A food company paying farmers in its sourcing regions to adopt regenerative practices is insetting. Insetting directly reduces reportable Scope 3 emissions and is increasingly preferred by SBTi guidance over offsets that do not affect a company's own footprint.

Carbon leakage

Carbon leakage occurs when emissions reductions in one jurisdiction are offset by emissions increases elsewhere, usually because production relocates to regions with weaker climate regulation. The EU designed CBAM specifically to address leakage risk in energy-intensive sectors. Leakage is also a core risk in forest carbon projects, where protecting one forest can simply displace harvesting to an adjacent one.

Carbon market

A carbon market is any trading system for emission allowances or carbon credits. Compliance markets are government-created and include the EU ETS, UK ETS, California and RGGI programs. The voluntary market, where corporates buy project-based credits for ESG goals, reached roughly 1.7 billion tonnes of cumulative credits issued by mid-2024 according to Ecosystem Marketplace data.

Carbon negative

Carbon negative means a company, product or process removes more greenhouse gases from the atmosphere than it emits across a defined boundary. It is a stricter claim than net-zero, which requires only balance. Microsoft, Stripe and Ikea have publicly committed to carbon-negative goals that rely on combinations of aggressive internal reductions and verified removals rather than avoidance credits.

Carbon neutral

Carbon neutral is the state in which total emissions within a defined scope are balanced by an equivalent volume of offsets or removals. Unlike net-zero, carbon-neutral claims historically allowed heavy use of avoidance offsets and did not require science-based reduction trajectories. ISO 14068-1, published in 2023, tightens carbon-neutrality standards and brings them closer to net-zero expectations.

Carbon offset

A carbon offset is a credit purchased to compensate for an emission that was not directly prevented. Offsets finance projects elsewhere -- renewable energy, reforestation, methane capture, clean cookstoves -- that reduce or remove emissions. The offset market has been under scrutiny for questionable additionality and over-crediting; the Integrity Council for the Voluntary Carbon Market published Core Carbon Principles in 2023 to raise quality standards.

Carbon removal

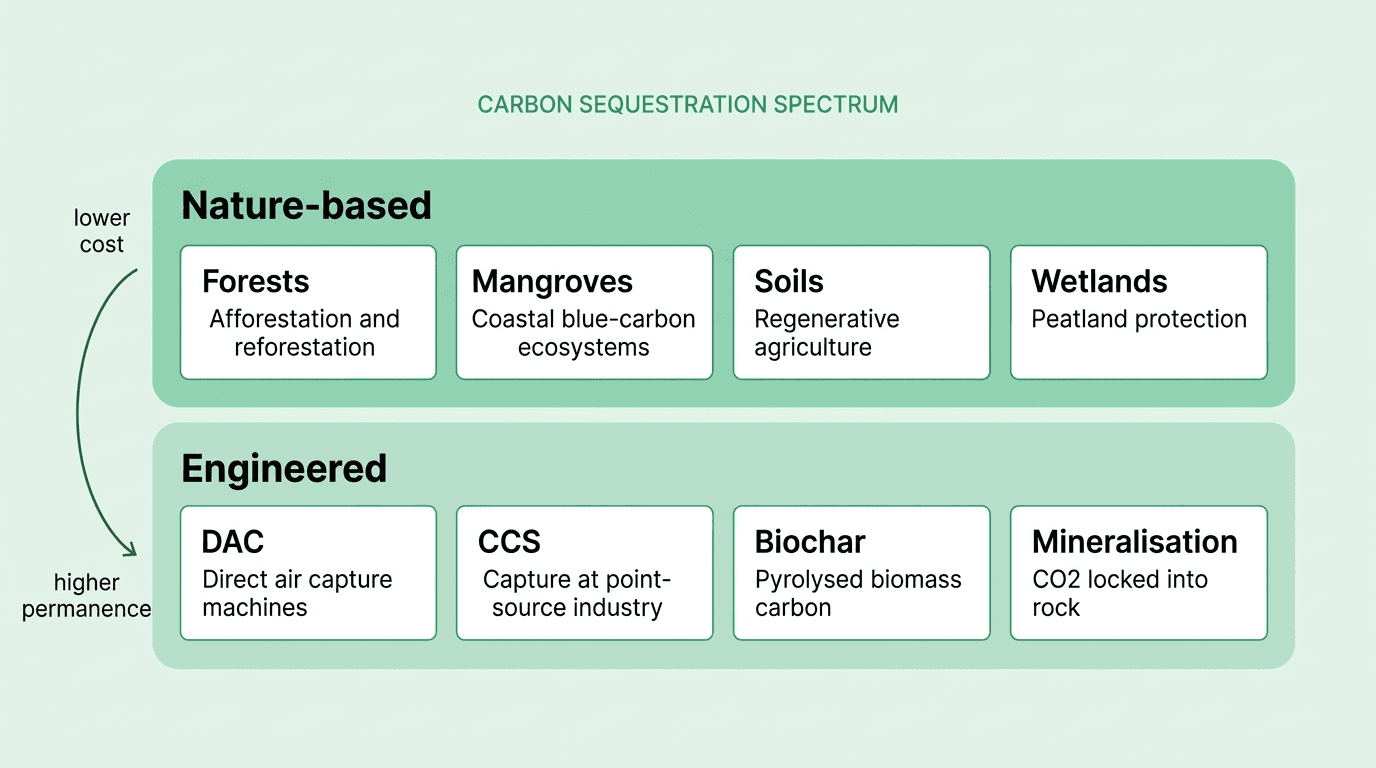

Carbon removal is the direct physical extraction of CO2 from the atmosphere and its storage in geological, biological, mineral or product reservoirs. Nature-based pathways include afforestation, wetland restoration and soil-carbon sequestration. Engineered pathways include direct air capture, biochar, mineralisation and bioenergy with CCS. Removals differ from offsets in that they physically reverse emissions rather than preventing new ones.

Carbon sequestration

Carbon sequestration is the long-term storage of atmospheric carbon in a reservoir -- biological (forests, soils, wetlands), geological (saline aquifers, depleted reservoirs) or mineral (carbonate rock). It is distinct from emissions reduction: sequestration addresses CO2 already in the atmosphere rather than preventing new emissions. Durability varies from decades (biological) to geological timescales (mineralisation).

Carbon sink

A carbon sink is any natural or engineered system that absorbs more CO2 than it emits over a given period. Oceans absorb about 26% of anthropogenic CO2 annually and terrestrial ecosystems a further 31%, per the Global Carbon Budget 2023. Deforestation, soil degradation and marine heatwaves reduce sink capacity, pushing more of each year's emissions to remain in the atmosphere.

Carbon tax

A carbon tax is a government levy charged per tonne of CO2e emitted. Unlike cap-and-trade, the price is fixed and the volume of emissions is allowed to respond. As of 2024, the World Bank tracked 39 carbon-tax regimes worldwide, with Sweden's at around USD 130/tCO2 among the highest. Carbon taxes are frequently combined with border adjustments and revenue-recycling to address competitiveness and equity concerns.

CDP

CDP is a global non-profit running the world's largest voluntary environmental disclosure system, covering climate change, water security, forests and plastics. More than 24,000 companies disclosed through CDP in 2024, representing roughly two-thirds of global market capitalisation. CDP-scored responses (A, A-, B, etc.) are widely referenced by investors and procurement teams and align with TCFD, IFRS S2 and ESRS structures.

Circular economy

A circular economy designs out waste by keeping materials in use through reuse, repair, remanufacture and recycling. It interacts with carbon management because extending product lifetimes and recovering materials typically reduces upstream embodied emissions. ESRS E5 (Resource Use and Circular Economy) and the EU Circular Economy Action Plan require large companies to disclose circularity metrics alongside emissions.

Clean Development Mechanism (CDM)

The Clean Development Mechanism (CDM) was a Kyoto Protocol market that allowed developed countries to finance emissions-reduction projects in developing countries and count the resulting Certified Emission Reductions toward their own targets. CDM is effectively superseded by Article 6 of the Paris Agreement, which rebuilds the international market architecture under a new Internationally Transferred Mitigation Outcomes framework.

Climate change

Climate change is the long-term alteration of temperature, precipitation and weather patterns driven by rising concentrations of greenhouse gases. According to the IPCC AR6 Synthesis Report (2023), global surface temperature has already risen 1.1 C above 1850-1900 levels, and current policies put the world on track for 2.4-2.6 C of warming by 2100 in the absence of stronger mitigation.

Climate risk

Climate risk covers the financial and operational exposures a company faces from climate change. Physical risk splits into acute (storms, floods, wildfires) and chronic (sea-level rise, drought, heat). Transition risk covers policy changes, technology shifts, market signals and reputational effects as the economy decarbonises. TCFD, IFRS S2 and ESRS E1 all require disclosure of material climate risks and scenario analysis.

Conference of the Parties (COP)

The Conference of the Parties (COP) is the annual negotiating body of the UN Framework Convention on Climate Change. COP21 in Paris (2015) produced the Paris Agreement; COP26 in Glasgow (2021) produced the Glasgow Climate Pact; COP28 in Dubai (2023) produced the Global Stocktake and the first explicit commitment to "transition away from fossil fuels." Each COP reviews NDC progress and negotiates rules and finance.

Corporate carbon footprint

A corporate carbon footprint is the total Scope 1, 2 and 3 emissions of an enterprise, measured over a defined reporting period. It is the enterprise-level analogue of a product carbon footprint and is the primary input for SBTi targets, CSRD and IFRS S2 disclosures, and CDP climate submissions. A corporate carbon footprint is also the basis for most internal carbon-pricing schemes.

Corporate Sustainability Due Diligence Directive (CSDDD)

The Corporate Sustainability Due Diligence Directive (CSDDD), adopted in 2024, requires large EU companies to identify, prevent, mitigate and account for adverse human-rights and environmental impacts across their operations and value chains. It interacts closely with CSRD (reporting) and requires a transition plan aligned with a 1.5 C pathway. CSDDD phases in between 2027 and 2029 depending on company size.

Corporate Sustainability Reporting Directive (CSRD)

The Corporate Sustainability Reporting Directive (CSRD), which entered force in 2024, replaces the earlier Non-Financial Reporting Directive and mandates detailed sustainability disclosure for large and listed EU companies. CSRD reports are prepared against the European Sustainability Reporting Standards (ESRS), are subject to third-party assurance, and are machine-readable through digital tagging. Wave 1 companies filed first CSRD reports in 2025.

D

Decarbonisation

Decarbonisation is the structural reduction of carbon intensity in an economy, sector or company, delivered through electrification, efficiency, fuel switching, circularity and process change. It differs from offsetting because it removes emissions at source. The IEA's Net Zero by 2050 scenario relies on decarbonisation for more than 90% of required emissions reductions, with removals addressing only residual sources.

Direct air capture (DAC)

Direct air capture (DAC) is a family of technologies that remove CO2 directly from ambient air using chemical sorbents or solvents. Captured CO2 is either stored geologically (DACCS) or reused in fuels and materials. DAC is among the most durable removal methods but is energy-intensive and early-stage: global capacity in 2024 was below 20 ktCO2/year, though project pipelines exceed 100 MtCO2/year by 2030.

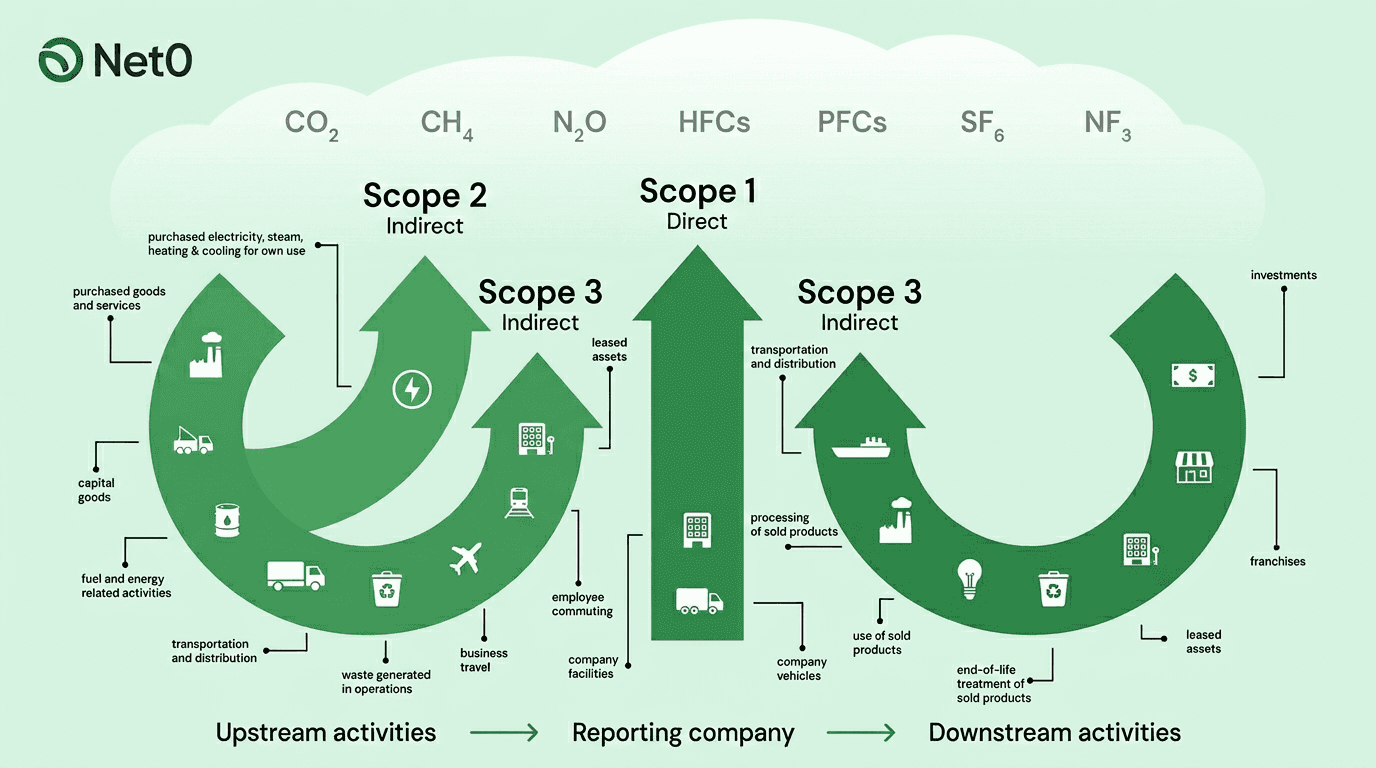

Direct emissions

Direct emissions are greenhouse gases released from sources an organisation owns or controls -- the GHG Protocol definition of Scope 1. Examples include on-site combustion in boilers and furnaces, fleet fuel, fugitive refrigerants and process emissions from manufacturing. Direct emissions are usually the easiest to quantify with high data quality because the company controls the meters, invoices and equipment.

Double counting

Double counting is the attribution of the same emission reduction, removal or credit to more than one entity or report. It undermines the integrity of carbon markets and corporate disclosures. Paris Agreement Article 6 rules introduced Corresponding Adjustments to prevent double counting in international credit transfers, and the VCM Integrity Council requires robust registry safeguards against it.

Double materiality

Double materiality is the principle -- central to CSRD and ESRS -- that companies must disclose both (a) how sustainability topics affect their financial performance (financial materiality), and (b) how the company's activities affect people and the environment (impact materiality). It contrasts with the single-materiality approach used by IFRS S1 and S2, which focuses on financial materiality alone.

Downstream emissions

Downstream emissions are Scope 3 emissions that occur after a company's product or service is sold -- use-phase energy consumption, end-of-life disposal, downstream transportation, investments and franchises. For a carmaker, use-phase emissions from customers driving the cars often dwarf manufacturing emissions. Scope 3 categories 9 through 15 cover downstream activities.

E

Embodied carbon

Embodied carbon is the CO2e released across a product's supply chain before it enters use -- raw-material extraction, processing, manufacturing, logistics and construction. In buildings, embodied carbon can represent 40-50% of lifetime emissions (World Green Building Council). It is a critical metric in Environmental Product Declarations (EPDs) and is covered by standards such as ISO 21930 and EN 15804.

Emission factor

An emission factor is a coefficient that converts a unit of activity into a mass of greenhouse gas emissions -- for example 0.204 kgCO2e per kWh of UK grid electricity in 2024 (UK BEIS/Defra). Major public datasets include DEFRA, US EPA, ecoinvent, IEA and Exiobase. Choice of emission factor materially affects reported emissions, which is why activity-based, production-based and spend-based factors are scrutinised in audit.

Emissions Trading System (EU ETS)

The EU Emissions Trading System is the world's first and largest mandatory carbon market, covering power, heavy industry and aviation within the EEA. Its cap declines at 4.3-4.4% per year from 2024, pushing the system toward a 62% emissions reduction by 2030 versus 2005. The EU ETS 2, covering road transport and buildings, starts in 2027. Allowance prices have averaged around EUR 70-90/tCO2 across 2023-2024.

Energy mix

Energy mix is the share of each fuel or technology in a country's or company's total primary energy or electricity supply. Shifting the mix toward renewables, nuclear and low-carbon fuels is the most direct lever for decarbonising Scope 2 emissions. Market-based and location-based Scope 2 methods require different treatments of the energy mix, and the grid mix is a primary driver of emission factors for purchased electricity.

Environmental Product Declaration (EPD)

An Environmental Product Declaration (EPD) is a standardised document that reports the life-cycle environmental impacts of a product, including its carbon footprint, based on Product Category Rules. EPDs are verified by independent programme operators (EPD International, UL, IBU) and are central to sustainable procurement, LEED and BREEAM certifications, and compliance with the EU Construction Products Regulation.

ESG reporting

ESG reporting is the disclosure of environmental, social and governance performance to investors, regulators and other stakeholders. On the environmental side, ESG reports typically include Scope 1, 2 and 3 emissions, energy, water, waste and biodiversity data. Standards used include CSRD/ESRS in the EU, IFRS S1 and S2 globally, the SEC climate rule in the US, GRI for multi-stakeholder reporting and CDP for voluntary disclosure.

EU Taxonomy

The EU Taxonomy is a classification system that defines which economic activities are environmentally sustainable. It sets technical screening criteria across six environmental objectives and is used in CSRD reporting, SFDR product labelling and EU green-bond standards. For an activity to qualify, it must substantially contribute to at least one objective, do no significant harm to the others, and meet minimum social safeguards.

European Sustainability Reporting Standards (ESRS)

The European Sustainability Reporting Standards (ESRS) are the technical standards companies use to prepare CSRD reports. ESRS comprises 12 topical standards covering climate (E1), pollution (E2), water and marine resources (E3), biodiversity (E4), resource use and circular economy (E5), own workforce (S1), workers in the value chain (S2), affected communities (S3), consumers and end-users (S4) and business conduct (G1), plus two cross-cutting standards.

F

Financed emissions

Financed emissions are the Scope 3 category 15 emissions of a financial institution -- the share of portfolio-company emissions attributable to the institution's loans, equity, bonds and project finance. The Partnership for Carbon Accounting Financials (PCAF) Global GHG Accounting and Reporting Standard is the dominant methodology. Banks' financed emissions typically exceed their operational footprint by two to three orders of magnitude.

Fossil fuels

Fossil fuels -- coal, oil and natural gas -- supplied about 80% of global primary energy in 2023 (IEA) and were responsible for roughly 75% of anthropogenic CO2 emissions. The COP28 Global Stocktake marked the first UNFCCC consensus text calling for a "transition away from fossil fuels in energy systems". Phasing down unabated fossil-fuel use is the single largest lever in every credible 1.5 C scenario.

Fugitive emissions

Fugitive emissions are unintentional or incidental releases of gases from equipment -- refrigerant leaks from HVAC, methane leaks from gas pipelines and oil-and-gas upstream operations, SF6 leakage from electrical switchgear. They are reported under Scope 1 and are disproportionately impactful because several fugitive gases (methane, SF6, HFCs) have very high global warming potentials.

G

GHG inventory

A GHG inventory is the structured list of an organisation's emission sources, activity data and calculated emissions across Scope 1, 2 and 3 for a reporting period. It follows GHG Protocol boundaries, documents assumptions and uncertainties, and is the artefact audited during assurance. A defensible inventory requires version control, emission-factor traceability and reconciliation between financial and operational records.

Global warming

Global warming is the rise in Earth's long-term average surface temperature driven by accumulated greenhouse gases. The World Meteorological Organization confirmed 2024 as the first calendar year to exceed 1.5 C above the 1850-1900 pre-industrial baseline, although the Paris 1.5 C target refers to multi-decadal averages. Every additional 0.1 C of warming materially increases the risk of crossing climate tipping points.

Global Warming Potential (GWP)

Global Warming Potential (GWP) is the factor used to express a non-CO2 gas in CO2-equivalent units by comparing its heat-trapping effect over a specified period -- typically 100 years. IPCC AR6 GWP-100 values include 27-30 for fossil methane, 273 for nitrous oxide and over 25,000 for SF6. GWP-20 values are higher for short-lived gases like methane and are increasingly used to highlight near-term climate impact.

Gold Standard

The Gold Standard for the Global Goals is a carbon-credit certification body founded by WWF and other NGOs in 2003. It certifies emissions-reduction and removal projects that also deliver social and sustainable-development co-benefits aligned with the UN SDGs. Alongside Verra's VCS, it is one of the two most widely recognised voluntary-market standards and has issued more than 280 million credits.

Green bond

A green bond is a debt instrument whose proceeds are ringfenced for projects with defined environmental benefits. The global green-bond market exceeded USD 2.8 trillion in cumulative issuance by end-2024 (Climate Bonds Initiative). Standards such as the EU Green Bond Standard and the ICMA Green Bond Principles require use-of-proceeds reporting and impact disclosure, typically aligned with the EU Taxonomy.

Greenhouse Gas Protocol

The Greenhouse Gas Protocol, developed by the World Resources Institute and WBCSD, is the world's most widely used standard for corporate emissions accounting. Its Corporate Standard defines Scope 1, 2 and 3; its Scope 2 Guidance establishes market- and location-based methods; its Corporate Value Chain (Scope 3) Standard covers 15 upstream and downstream categories. A major 2025-2026 update revisits Scope 2 and Scope 3.

Greenhouse gases (GHG)

Greenhouse gases are atmospheric constituents that absorb and re-emit infrared radiation, warming the lower atmosphere. The Kyoto basket -- CO2, methane (CH4), nitrous oxide (N2O), hydrofluorocarbons, perfluorocarbons, sulfur hexafluoride (SF6) and nitrogen trifluoride (NF3) -- is the set reported under UNFCCC and GHG Protocol frameworks. CO2 dominates by mass, but non-CO2 gases drive about a quarter of warming.

Greenwashing

Greenwashing is the practice of making misleading, unsubstantiated or exaggerated environmental claims about a product, service or organisation. The EU Green Claims Directive (provisional agreement 2024), the UK CMA Green Claims Code, and amendments to the US FTC Green Guides are tightening enforcement. CSRD, ISSB and SEC requirements for auditable disclosure are also shifting the legal perimeter for sustainability communications.

GRI Standards

GRI Standards, published by the Global Reporting Initiative, are the most widely adopted multi-stakeholder sustainability reporting standards. Unlike the IFRS/ISSB focus on investor-grade financial materiality, GRI centres on impact materiality and broader stakeholder interests. GRI's sector standards and its 2021 Universal Standards are referenced by CSRD and are compatible with ESRS disclosures.

H

Hydrogen

Hydrogen is a versatile energy carrier whose climate impact depends almost entirely on how it is produced. Grey hydrogen from unabated methane reforming accounts for the bulk of current production and is highly emissions-intensive. Blue hydrogen couples reforming with CCS; green hydrogen is produced by electrolysis powered by renewables. Green hydrogen is central to decarbonising steel, ammonia, refining and long-haul aviation.

I

IFRS S1 and S2

IFRS S1 and S2 are the first two standards issued by the International Sustainability Standards Board (ISSB). S1 sets general requirements for sustainability-related financial disclosures; S2 covers climate-specific disclosures and incorporates TCFD's four-pillar structure (governance, strategy, risk management, metrics and targets). As of 2025, 35+ jurisdictions had announced plans to adopt or reference the ISSB standards.

Indirect emissions

Indirect emissions are greenhouse gases released by sources not owned or controlled by the reporting company but associated with its activities. In the GHG Protocol, they include all Scope 2 emissions (purchased energy) and all Scope 3 emissions (the rest of the value chain). Indirect emissions typically dominate corporate footprints, especially for financial services, technology, retail and consumer-goods companies.

Intergovernmental Panel on Climate Change (IPCC)

The Intergovernmental Panel on Climate Change (IPCC) is the UN body that synthesises climate science for policymakers. Its Assessment Reports -- the Sixth (AR6) completed in 2023 -- underpin the scientific case for the 1.5 C target, the remaining carbon budget and the role of CO2 removal. The IPCC also publishes methodological guidelines used by national governments to prepare GHG inventories under the UNFCCC.

Internal carbon pricing

Internal carbon pricing is the practice of applying a self-imposed price to each tonne of CO2e a company emits, either as a shadow price in capital-expenditure appraisal or as a live internal fee. CDP's 2023 data showed more than 2,100 companies using internal carbon prices, with typical values between USD 25 and USD 75 per tonne. It is one of the strongest internal signals for decarbonisation decisions.

International Sustainability Standards Board (ISSB)

The International Sustainability Standards Board (ISSB), established under the IFRS Foundation in 2021, develops the global baseline of sustainability disclosure standards. It absorbed the Climate Disclosure Standards Board and the Value Reporting Foundation (SASB and IIRC) and has published IFRS S1 and S2, with further standards on biodiversity and human capital in development.

J

Just transition

A just transition is a decarbonisation pathway that explicitly manages the social and economic consequences for workers, communities and consumers -- for example, through reskilling, regional investment and targeted social protection. It is a formal element of the Paris Agreement preamble, of ESRS S1-S3 standards and of CSDDD due-diligence expectations, and is increasingly a condition for multilateral climate finance.

K

Kyoto Protocol

The Kyoto Protocol (1997, entered into force 2005) was the first international treaty to set binding emissions-reduction targets for developed countries. It introduced flexible mechanisms -- emissions trading, Joint Implementation and the Clean Development Mechanism -- that shaped subsequent carbon markets. Its structure was superseded by the Paris Agreement in 2015, which replaced top-down targets with nationally determined contributions.

L

Life cycle assessment (LCA)

Life cycle assessment (LCA) is the standardised methodology (ISO 14040 and 14044) for quantifying the environmental impacts of a product or service across its entire life cycle, from raw-material extraction to end-of-life. LCAs are the technical backbone of product carbon footprints, Environmental Product Declarations, eco-design decisions and sustainable-procurement scoring.

M

Marginal Abatement Cost Curve (MACC)

A Marginal Abatement Cost Curve (MACC) ranks emissions-reduction actions by cost per tonne of CO2e avoided and cumulative abatement potential. It is used to prioritise decarbonisation investments -- energy efficiency and electrification often sit at negative cost, while heavy-industry fuel switching, CCS and DAC sit at the expensive right-hand end. MACCs are central tools in profitable decarbonisation strategy.

Materiality assessment

A materiality assessment identifies which sustainability topics are important enough to report on. CSRD and ESRS require a double-materiality assessment considering both financial materiality and impact materiality. IFRS S1 requires a single-materiality assessment focused on financial effects. Materiality assessments are typically refreshed every two to three years and now involve formal stakeholder consultation and evidence documentation.

Methane (CH4)

Methane (CH4) is a potent greenhouse gas with an IPCC AR6 100-year GWP of 27-30 and a 20-year GWP of 81-83. Major sources are oil-and-gas operations, coal mining, livestock, rice paddies and waste. The Global Methane Pledge, launched at COP26, commits signatories to a 30% reduction by 2030 versus 2020. Methane abatement is widely considered the single highest-impact near-term mitigation action.

Mitigation

Mitigation is any intervention that reduces or prevents greenhouse gas emissions -- renewable energy deployment, efficiency, electrification, CCS, avoided deforestation, demand reduction, material substitution. It is the twin of adaptation (reducing vulnerability to climate impacts) in UNFCCC terminology. Corporate mitigation typically follows the hierarchy of avoid, reduce, substitute, then compensate residual emissions with removals.

N

Nature-based solutions

Nature-based solutions are actions that protect, sustainably manage or restore ecosystems to deliver climate, biodiversity and social benefits. Protecting mature forests, restoring mangroves, rewetting peatlands and adopting regenerative agriculture all qualify. The IPCC AR6 concluded that nature-based solutions could deliver up to a third of cost-effective mitigation by 2030, but cannot substitute for rapid fossil-fuel phase-down.

Net zero

Net zero is the state in which anthropogenic greenhouse gas emissions are balanced by anthropogenic removals over a specified boundary and period. The Paris Agreement's 1.5 C pathway requires global net-zero CO2 by around 2050 and net-zero on all GHGs shortly after. Corporate net-zero differs from carbon-neutrality because it requires deep reductions (typically 90%+) before residual emissions can be neutralised by permanent removals.

Net-zero target

A net-zero target is a dated, public commitment to reach net-zero emissions, typically across Scope 1, 2 and material Scope 3. Credible targets (for instance SBTi-validated ones) include near-term milestones, a long-term 2050 endpoint, explicit emissions boundaries, a residual-emissions treatment policy, and an annual reporting cadence. The UN's Integrity Matters framework sets the benchmark criteria.

Nitrous oxide (N2O)

Nitrous oxide (N2O) is a greenhouse gas with an IPCC AR6 GWP-100 of 273, making it far more potent than CO2 on a per-mass basis. Agriculture, especially synthetic-fertiliser use, is the dominant anthropogenic source; industrial processes (adipic acid, nitric acid) and transport also contribute. Atmospheric concentrations have risen around 25% since the pre-industrial era (WMO Greenhouse Gas Bulletin 2024).

O

Operational vs financial control boundary

Operational control and financial control are two of the three consolidation approaches in the GHG Protocol (the third is equity share). Under operational control, a company reports 100% of emissions from operations where it has authority to set policy. Under financial control, it reports 100% of emissions where it bears the majority of financial risks and rewards. Choice of boundary determines which entities are inside Scope 1 and 2.

Ozone (O3)

Ozone is a triatomic oxygen molecule. In the stratosphere it shields the biosphere from UV radiation and is protected by the Montreal Protocol. At ground level (tropospheric ozone) it is a short-lived air pollutant and a significant climate forcer. Ozone is not in the Kyoto basket but is tracked in air-quality frameworks and in the IPCC's radiative-forcing analyses.

P

Paris Agreement

The Paris Agreement is the 2015 UNFCCC treaty under which 195 parties committed to limit warming to "well below 2 C" and pursue efforts to limit it to 1.5 C above pre-industrial levels. It operates through nationally determined contributions updated every five years, a Global Stocktake, and Article 6 market mechanisms. Compliance and voluntary carbon markets, SBTi targets and most national net-zero laws all trace their legitimacy back to Paris.

PCAF (Partnership for Carbon Accounting Financials)

PCAF is the industry-led body that develops the Global GHG Accounting and Reporting Standard for the Financial Industry. It defines how banks, asset managers and insurers calculate financed, facilitated and insured emissions. PCAF methodologies are referenced by SBTi's Financial Sector Science-Based Targets Guidance, by CDP Financial Services disclosures and by CSRD/ESRS guidance for financial institutions.

Permanence

Permanence is the expected duration over which a carbon removal or avoidance will remain effective. It is a critical quality attribute of carbon credits: a mangrove restored in 2025 but lost to a storm in 2035 delivers less durable benefit than CO2 mineralised in basalt. Credible standards require permanence-risk assessments, buffer reserves or explicit time-scaled crediting to address reversibility risk.

Primary vs secondary data

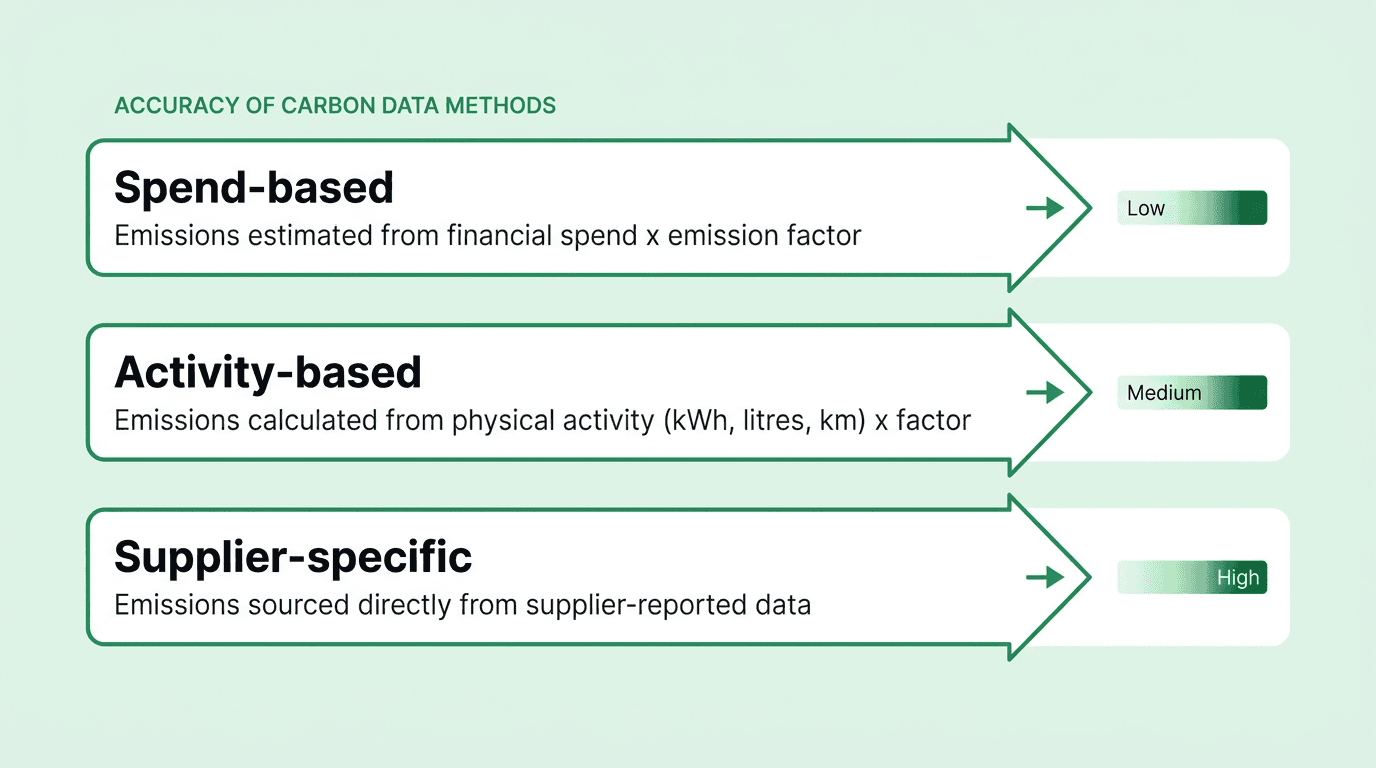

Primary data is emissions data measured or supplied directly from the source -- a supplier's verified product footprint, a meter reading, an invoice. Secondary data is estimated from databases (ecoinvent, DEFRA, IEA) or generic industry averages. GHG Protocol Scope 3 guidance prefers primary data for material categories. Moving from secondary to primary data is often the single biggest driver of emissions-accuracy improvement.

Product Carbon Footprint (PCF)

A Product Carbon Footprint (PCF) is the total greenhouse gas emissions associated with a specific product over a defined life-cycle boundary, measured in kgCO2e per functional unit. It is calculated using LCA methodology and reported under ISO 14067, the GHG Protocol Product Standard or PAS 2050. PCFs feed into EPDs, category-rules databases and supplier scorecards, and are increasingly required by B2B customers in regulated sectors.

R

REDD+

REDD+ stands for Reducing Emissions from Deforestation and forest Degradation, plus sustainable forest management and enhancement of forest carbon stocks. It is a UNFCCC-recognised mechanism for compensating developing countries for forest-based mitigation. Jurisdictional REDD+ programmes (ART-TREES, VCS JNR) aim to address some of the additionality, leakage and over-crediting concerns that have beset project-based forest credits.

Reforestation

Reforestation is the restoration of forest on land that was recently forested but is now cleared or degraded. Compared with afforestation, reforestation typically delivers larger near-term carbon gains because soils, seed banks and hydrology are already suited to forest cover. Reforestation projects can be credited under VCS's AFOLU methodologies and are one of the most common nature-based components of corporate net-zero plans.

S

SASB Standards

SASB Standards are industry-specific sustainability disclosure standards developed by the Sustainability Accounting Standards Board. SASB merged with the IIRC in 2021 to form the Value Reporting Foundation, which was consolidated into the ISSB in 2022. SASB's 77 industry standards continue to inform IFRS S1 and S2 disclosure expectations and remain in active use by US-listed companies.

SBTi Net-Zero Standard

The SBTi Net-Zero Standard is the framework SBTi uses to validate corporate net-zero targets. It requires near-term reductions of around 42-50% across Scope 1 and 2 by 2030, long-term reductions of at least 90% by 2050, boundary coverage of material Scope 3, and explicit treatment of residual emissions with permanent removals. A revised Version 2 of the standard is expected in 2026.

Science-Based Targets initiative (SBTi)

The Science-Based Targets initiative (SBTi) is the dominant framework for validating corporate emissions-reduction targets against 1.5 C or well-below-2 C pathways. It is a partnership between CDP, UN Global Compact, WRI and WWF. Over 7,000 companies had committed or validated SBTi targets by 2025. Sector-specific guidance covers financial services, forest/land/agriculture (FLAG), aviation, steel and others.

Scope 1 emissions

Scope 1 emissions are direct greenhouse gas emissions from sources owned or controlled by the reporting company -- on-site combustion, fleet fuel, fugitive refrigerants and process emissions. They are typically the smallest of the three scopes for service-based companies and the largest for heavy industry. Scope 1 data usually has the highest accuracy because it comes from internal meters and invoices.

Scope 2 emissions

Scope 2 emissions are indirect emissions from the generation of purchased electricity, steam, heat and cooling consumed by the reporting company. The GHG Protocol Scope 2 Guidance requires dual reporting under the location-based method (grid averages) and the market-based method (contractual instruments such as Energy Attribute Certificates and PPAs). Scope 2 is typically the easiest scope to decarbonise rapidly.

Scope 3 emissions

Scope 3 emissions are all other indirect emissions in a company's value chain, grouped into 15 categories across upstream and downstream activities -- purchased goods and services, capital goods, fuel-and-energy related activities, transportation, waste, business travel, commuting, leased assets, use of sold products, end-of-life, investments and franchises. Scope 3 is usually the largest scope and the hardest to measure, but it is where the decarbonisation leverage lies.

Scope 4 emissions

Scope 4 emissions -- more formally avoided emissions -- are reductions that occur outside a product's life cycle as a result of using the product. A more efficient appliance, a low-carbon cement, or a virtual-meeting platform all avoid emissions elsewhere. Scope 4 is not part of the GHG Protocol Corporate Standard; WRI published dedicated guidance in 2022, and claims must follow strict comparability and double-counting rules.

SEC Climate Disclosure Rule

The SEC Climate Disclosure Rule, finalised in March 2024, requires US-listed companies to disclose climate-related financial risks, governance, targets and -- for large accelerated filers -- material Scope 1 and 2 emissions subject to assurance. The rule excluded Scope 3 from the final version and has faced litigation and a stay, making California's SB-253 the tighter de-facto US regime for many companies.

SME Climate Hub

The SME Climate Hub, hosted by We Mean Business, the Exponential Roadmap Initiative, the UN Race to Zero and the ICC, is a global platform that helps small and medium-sized enterprises make and meet a standard climate commitment: to halve emissions by 2030, reach net-zero by 2050 and report progress annually. It supersedes the earlier "SME Climate Commitment" and has been adopted by more than 8,000 companies.

Spend-based, activity-based and supplier-specific data

These three emission-factor methodologies sit on an accuracy gradient. Spend-based multiplies expenditure (USD or EUR) by an emission factor per currency unit. Activity-based multiplies physical consumption (kWh, kg, km) by an emission factor per unit of activity. Supplier-specific uses the actual reported footprint of a named supplier. Moving up this gradient reduces uncertainty and unlocks supplier-level decarbonisation.

Streamlined Energy & Carbon Reporting (SECR)

Streamlined Energy & Carbon Reporting (SECR) is a UK framework introduced in April 2019 that requires large UK companies, LLPs and certain quoted companies to disclose UK energy consumption, associated greenhouse gas emissions and an energy-efficiency narrative in their annual reports. SECR complements, but does not duplicate, the UK's emissions-trading and CCA regimes.

Supply chain emissions

Supply chain emissions are the greenhouse gases released across a company's upstream value chain -- extraction of raw materials, supplier operations, inbound logistics and upstream leased assets. In GHG Protocol terms they are categories 1-8 of Scope 3. For many consumer-goods, retail and technology companies, supply chain emissions are the dominant part of the corporate footprint, which is why reducing upstream emissions is a strategic priority.

Sustainable Aviation Fuel (SAF)

Sustainable Aviation Fuel (SAF) is a drop-in jet fuel produced from sustainable feedstocks -- used cooking oils, agricultural residues, municipal waste, power-to-liquid synthesis -- that reduces life-cycle CO2 by 60-90% versus fossil kerosene when certified under schemes such as CORSIA and RED II. The EU's ReFuelEU Aviation regulation mandates SAF blending of 2% in 2025, rising to 70% by 2050.

Sustainable Development Goals (SDGs)

The Sustainable Development Goals are 17 global goals adopted by UN member states in 2015 with a 2030 delivery horizon. They cover poverty, health, education, gender equality, clean water, energy, climate (SDG 13), life below water (SDG 14) and life on land (SDG 15) among others. Corporate sustainability frameworks such as the Gold Standard and GRI explicitly map impact claims to SDG outcomes.

Sustainable Finance Disclosure Regulation (SFDR)

The Sustainable Finance Disclosure Regulation (SFDR) is an EU regulation that requires financial-market participants to disclose how they integrate sustainability risks and adverse impacts into investment decisions. SFDR classifies financial products as Article 6 (no sustainability claim), Article 8 (promoting environmental or social characteristics) or Article 9 (sustainable investment objective). SFDR interacts tightly with the EU Taxonomy and CSRD.

T

Task Force on Climate-related Financial Disclosures (TCFD)

The Task Force on Climate-related Financial Disclosures (TCFD), established by the Financial Stability Board in 2015, published the recommendation framework that now sits at the core of most climate-disclosure regimes. Its four pillars -- governance, strategy, risk management, and metrics and targets -- were fully absorbed into IFRS S2 in 2023. The FSB formally disbanded the TCFD in 2023, and monitoring responsibility passed to the IFRS Foundation.

Taskforce on Nature-related Financial Disclosures (TNFD)

The Taskforce on Nature-related Financial Disclosures (TNFD) released its final recommendations in September 2023. TNFD mirrors the TCFD four-pillar structure but covers nature-related dependencies, impacts, risks and opportunities across water, land, oceans and biodiversity. Disclosures are organised through the LEAP process (Locate, Evaluate, Assess, Prepare) and reference the Global Biodiversity Framework and the SBTN methodology.

Tipping point

A climate tipping point is a threshold beyond which a component of the Earth system shifts into a qualitatively different state that is difficult or impossible to reverse on human timescales. Examples include Amazon dieback, West Antarctic Ice Sheet collapse, permafrost methane release and Atlantic Meridional Overturning Circulation (AMOC) weakening. A 2022 Science paper found five tipping points may be reached at 1.5 C of warming.

Transition plan

A transition plan is a company's dated roadmap to shift to a low-carbon business model consistent with a 1.5 C pathway. It specifies near- and long-term emissions targets, capital-allocation implications, business-model changes, governance accountability and engagement strategy. The UK Transition Plan Taskforce published a detailed disclosure framework in 2023 that is being incorporated into IFRS S2, CSRD and CSDDD expectations.

U

UN Framework Convention on Climate Change (UNFCCC)

The UN Framework Convention on Climate Change is the 1992 international treaty ratified by 198 parties that established the multilateral architecture for addressing climate change. Its annual Conference of the Parties (COP) is the primary forum for climate negotiations. The Kyoto Protocol (1997) and the Paris Agreement (2015) are the two principal legal instruments adopted under the UNFCCC.

Upstream emissions

Upstream emissions are the Scope 3 emissions generated before a product reaches the reporting company -- purchased goods and services, capital goods, fuel and energy activities, upstream transportation, business travel, employee commuting and upstream leased assets. They correspond to Scope 3 categories 1 through 8. Reducing upstream emissions typically requires supplier engagement, procurement policy changes and primary data collection.

V

Value chain emissions

Value chain emissions are the sum of all upstream and downstream Scope 3 emissions associated with a product, service or company. In GHG Protocol terms, value chain emissions span all 15 Scope 3 categories and exclude Scope 1 and 2 of the reporting company itself. SBTi and CSRD increasingly require that companies with material value-chain emissions include them in both targets and reporting.

Verified Carbon Standard (VCS / Verra)

The Verified Carbon Standard, administered by Verra, is the largest voluntary-market standard and has issued more than 1.1 billion credits across REDD+, renewable energy, methane, agriculture and industrial projects. After a series of integrity reviews in 2023-2024, Verra updated its REDD+ methodology (VM0048) and tightened project accounting rules, bringing VCS closer to the Integrity Council's Core Carbon Principles.

Voluntary carbon market

The voluntary carbon market is the ecosystem in which companies and individuals buy carbon credits to meet self-set commitments rather than legal obligations. It is distinct from compliance markets such as the EU ETS. Voluntary-market issuance and retirement volumes peaked in 2021 and have since contracted as credit-integrity concerns surfaced; the Integrity Council for the Voluntary Carbon Market is now the primary standard-setter.

W

Water stewardship

Water stewardship is the responsible use, management and governance of water resources across operations and value chains. It covers quantity (withdrawal, consumption, discharge), quality (pollution, temperature) and shared catchment risk. It is a material topic under ESRS E3, CDP Water Security and the Alliance for Water Stewardship standard. Water and carbon are increasingly linked in disclosures, especially for data centres, agriculture and heavy industry.

Z

Zero carbon

Zero carbon is a claim that a product, process or organisation emits no CO2 across a defined boundary -- usually narrower than "net zero" because it does not rely on offsets or removals. Zero-carbon electricity, zero-carbon hydrogen and zero-carbon cement are common marketing constructs that require precise boundary definition and independent verification to avoid greenwashing risk under the EU Green Claims Directive and equivalent regimes.

How Net0 operationalises this vocabulary

Most of the definitions above become reportable numbers inside an enterprise system, not just words on a page. The Net0 AI-powered sustainability platform takes this full vocabulary -- Scope 1, 2 and 3, CSRD, ESRS, IFRS S1 and S2, SBTi, CBAM, PCAF, CSDDD, SEC, California, CDP, TCFD, TNFD -- and translates it into a live operating model. It pulls activity data from 10,000+ enterprise systems, maps each transaction to the correct emission factor out of a 50,000+ factor library, automates the data-collection pipeline, and produces disclosures aligned with 30+ sustainability frameworks. For institutional customers, this is how a glossary of concepts becomes an audit-ready, continuously updated sustainability operating system.

Book a demo to see how Net0's platform maps the terminology in this glossary into an end-to-end carbon management workflow.

Frequently Asked Questions

What is carbon accounting in simple terms?

Carbon accounting is the process of measuring, tracking and reporting an organisation's greenhouse gas emissions in tonnes of CO2-equivalent. It works like financial accounting: every activity that releases emissions (fuel use, electricity, purchased goods, travel) is multiplied by an emission factor and aggregated into Scope 1, 2 and 3 totals. The resulting numbers feed SBTi targets, CSRD reports and investor disclosures.

What is the difference between CSRD and ESRS?

CSRD is the EU directive that makes sustainability reporting mandatory for large and listed companies. ESRS are the technical standards companies actually use to prepare those reports. Put simply, CSRD is the law and ESRS are the rules. ESRS comprises 12 topical standards (climate, pollution, water, biodiversity, social, governance) plus two cross-cutting standards defining the preparation methodology.

Is a carbon offset the same as a carbon removal?

No. An offset finances an emissions reduction or avoidance elsewhere -- typically renewable energy, avoided deforestation or clean cookstoves. A removal physically extracts CO2 from the atmosphere and stores it in biological, geological or mineral reservoirs. Removals are generally considered higher-integrity than avoidance-based offsets and are the only credit type accepted by the SBTi Net-Zero Standard for neutralising residual emissions.

Are Scope 4 emissions officially recognised?

Scope 4, or avoided emissions, is not part of the GHG Protocol Corporate Standard. The World Resources Institute published specific guidance on avoided-emissions reporting in 2022, and companies increasingly disclose Scope 4 figures to describe the climate benefit their products deliver to customers. Scope 4 must always be reported separately from Scope 1, 2 and 3 to avoid double counting and integrity disputes.

Does SBTi require a net-zero target?

SBTi validates both near-term science-based targets and net-zero targets. Near-term targets cover a five- to ten-year horizon and are mandatory for any SBTi-committed company. A net-zero target, validated against the SBTi Net-Zero Standard, requires at least 90% emissions reduction by 2050 across Scope 1, 2 and material Scope 3, with residual emissions neutralised by permanent removals. Companies can commit to near-term alone, but the full credibility expectation is a validated net-zero target.

How does AI change carbon accounting?

AI changes carbon accounting primarily by compressing the data-collection and classification cycle. Machine learning extracts emissions-relevant fields from invoices, travel records, ERP transactions and supplier documents; matches each activity to the correct emission factor; detects anomalies; and produces audit-ready datasets in days rather than months. For enterprises with hundreds of entities and thousands of suppliers, this is the only practical route to continuous Scope 1, 2 and 3 reporting at CSRD or ISSB levels of rigour.