AI for Sustainability

SFDR Explained: EU Sustainable Finance Disclosure Regulation and Article 6, 8, 9 Classifications

A comprehensive guide to the SFDR, covering entity-level and product-level disclosures, Article 6, 8, and 9 classifications, PAI indicators, and the proposed SFDR 2.0 overhaul.

Sofia Fominova

Apr 16, 2026

TL;DR: The Sustainable Finance Disclosure Regulation (SFDR) is an EU regulation, effective since March 2021, that requires financial market participants to disclose how they integrate environmental, social, and governance (ESG) risks into investment decisions. It classifies financial products into Article 6, 8, and 9 categories based on their sustainability commitment, and mandates reporting on 14 Principal Adverse Impact (PAI) indicators annually by 30 June. A proposed overhaul known as SFDR 2.0, published by the European Commission in November 2025, will replace the current framework with three new product categories.

Key Takeaways

The SFDR has been in force since 10 March 2021, with Level 2 Regulatory Technical Standards (RTS) applying from 1 January 2023, according to the European Commission's 2025 legislative proposal.

Financial products are classified under Article 6 (no sustainability focus), Article 8 "light green" (promotes environmental or social characteristics), or Article 9 "dark green" (explicit sustainable investment objective). As of June 2024, Article 8 funds held a 57.6% market share, according to the European Commission's Platform on Sustainable Finance.

The regulation mandates 14 Principal Adverse Impact indicators -- six climate-related and eight covering broader ESG factors -- with annual PAI statements due by 30 June each year.

On 20 November 2025, the European Commission published a legislative proposal to overhaul the SFDR ("SFDR 2.0"), replacing the current Article 8 and 9 system with three mandatory categories: Transition, ESG Basics, and Sustainable, according to Paul Hastings' 2025 analysis.

Existing SFDR disclosure obligations remain fully applicable throughout 2026 while the SFDR 2.0 proposal moves through the EU co-decision process, with trilogues between the European Parliament and Council expected during 2026.

SFDR and Its Role in Sustainable Finance

Net0, an AI infrastructure company that builds intelligent systems for governments and global enterprises, supports organizations navigating the Sustainable Finance Disclosure Regulation (SFDR) through its AI-powered sustainability platform. The SFDR is a European Union regulation that took effect on 10 March 2021, designed to increase transparency in sustainable finance and prevent greenwashing in the investment industry.

The regulation requires financial market participants (FMPs) and financial advisors (FAs) operating within the EU to disclose specific information about how they integrate sustainability risks into investment decisions. According to the European Commission, the SFDR contributes directly to the EU's alignment with the Paris Agreement and its broader sustainable finance strategy.

The SFDR operates alongside other major EU sustainability regulations, including the Corporate Sustainability Reporting Directive (CSRD), the EU Taxonomy Regulation, and the European Sustainability Reporting Standards (ESRS). Together, these frameworks create a comprehensive regulatory ecosystem that channels capital toward sustainable economic activities and holds financial institutions accountable for their ESG reporting claims.

Who the SFDR Applies To

The SFDR applies to three primary groups of entities operating within or targeting the EU market. Financial market participants -- including asset managers, pension funds, insurance companies offering investment products, and venture capital fund managers -- must comply with all disclosure requirements. Financial advisors providing investment guidance are also subject to the regulation.

Non-EU firms are not exempt if they market products to EU investors. According to the European Commission's Q&A on SFDR, non-EU alternative investment fund managers accessing the EU market through the Alternative Investment Fund Managers (AIFM) Directive must meet SFDR disclosure standards. Entities with 500 or more employees face additional mandatory requirements, particularly around Principal Adverse Impact reporting.

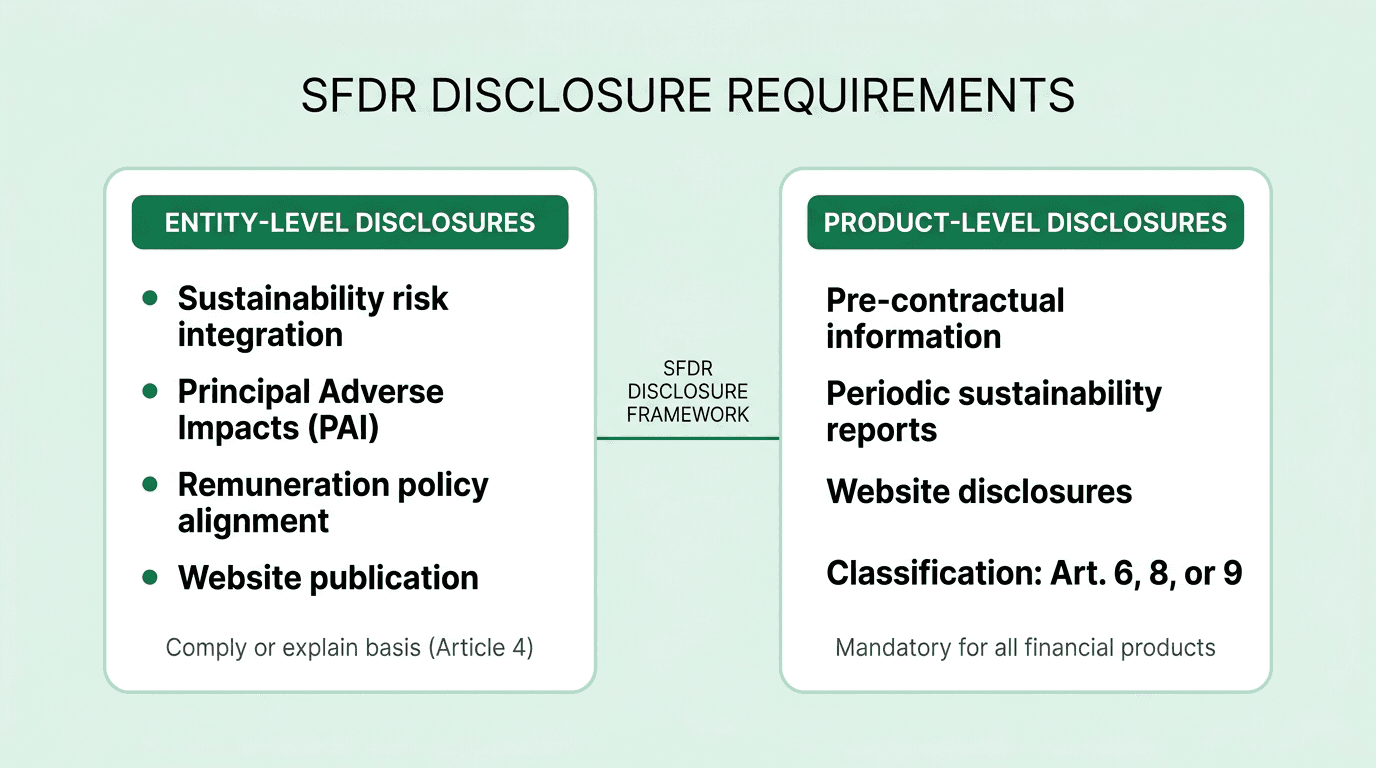

Entity-Level Disclosure Requirements

The SFDR establishes two distinct layers of disclosure: entity-level and product-level. Entity-level disclosures under Article 4 operate on a "comply or explain" basis, meaning firms must either report on their sustainability practices or publicly explain why they choose not to.

Firms that opt to comply must disclose across four dimensions. First, they must explain how sustainability risks are integrated into investment decision-making, including how risks are identified, assessed, and managed. Second, they must publish detailed Principal Adverse Impact (PAI) statements outlining how negative sustainability impacts are considered, the actions taken to address them, and the outcomes. According to the SFDR's Regulatory Technical Standards, six of the 14 mandatory PAI indicators are climate-related, and firms must additionally select at least two indicators from 46 voluntary options.

Third, entities must demonstrate how remuneration policies align with sustainability risk integration. Fourth, all entity-level disclosures must be published on the firm's website, ensuring transparency for investors and the public.

Product-Level Disclosures and SFDR Classifications

Product-level disclosures apply to individual financial products, including UCITS mutual funds, alternative investment funds, and pension products. The SFDR categorizes these products into three classifications based on the degree of sustainability integration, each carrying progressively stringent disclosure requirements.

All classified products must provide pre-contractual disclosures (under Article 7), periodic sustainability reports, and publicly available website disclosures detailing their sustainability strategies, indicators, and methodologies.

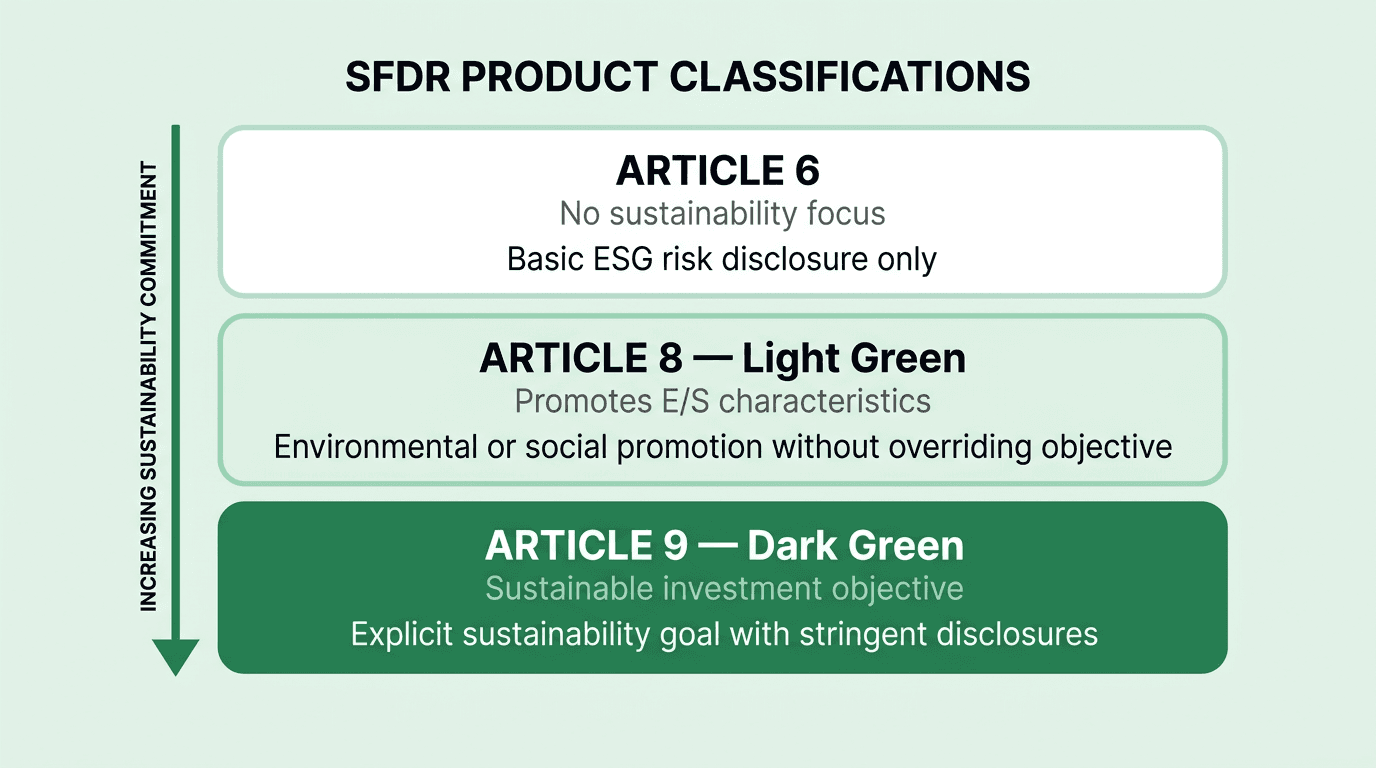

SFDR Article 6, 8, and 9 Explained

Article 6 products do not incorporate sustainability as a central investment objective. However, they are still required to disclose how sustainability risks are integrated into investment decisions and the potential impact of those risks on returns. According to Robeco's 2024 SFDR classification guide, if an Article 6 product does not consider adverse sustainability impacts, the firm must provide a statement explaining why.

Article 8 products, often called "light green" funds, actively promote environmental or social characteristics without making sustainability the overriding investment objective. Fund managers must disclose the specific environmental or social characteristics promoted, the investment strategy, assessment methodologies, sustainability indicators, and adherence to the "do no significant harm" (DNSH) principle. According to the European Commission's Platform on Sustainable Finance, Article 8 funds held 57.6% of EU market share as of June 2024, making them the dominant category.

Article 9 products, known as "dark green" funds, carry an explicit sustainable investment objective. These face the most stringent disclosure requirements: detailed information on the sustainable investment objective, the methodology for achieving it, impact measurement frameworks, and a thorough DNSH assessment. Article 9 funds represented a steady 3.4% of the EU market as of mid-2024. In Q3 2025, Article 8 funds saw a significant rebound, netting an estimated EUR 75 billion in new capital, according to Morningstar's Q3 2025 SFDR review.

Article 7 addresses product-level PAI disclosure specifically, requiring that PAI information be published in pre-contractual documentation such as fund prospectuses and information memoranda.

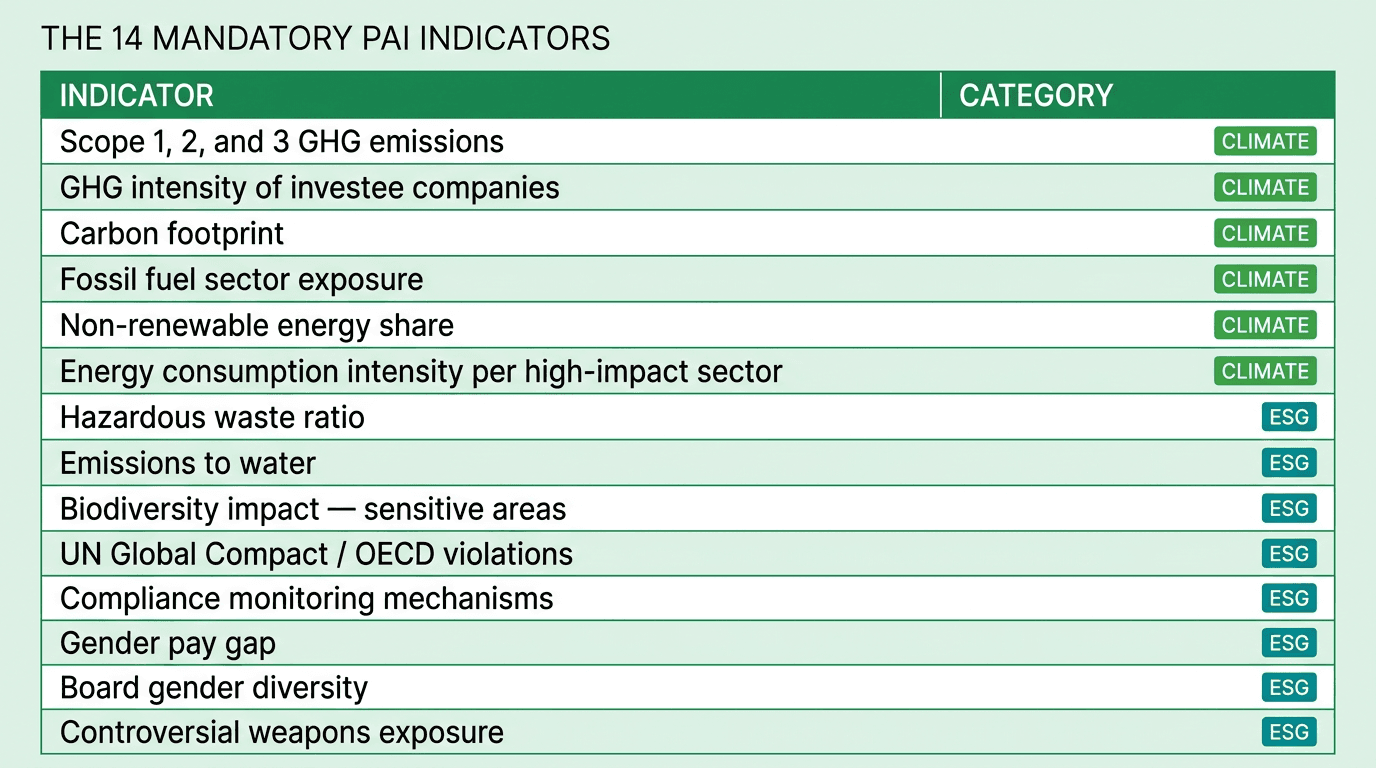

Principal Adverse Impact Indicators Under the SFDR

Principal Adverse Impact (PAI) disclosures are the SFDR's mechanism for measuring the negative sustainability impacts of investment decisions. PAI reporting is mandatory for entities with 500 or more employees. Smaller firms may opt out but must publish an explanation and state whether they intend to consider PAIs in the future.

The SFDR's Regulatory Technical Standards define 14 mandatory indicators, supplemented by at least two additional voluntary indicators (one environmental, one social) chosen from a pool of 46. Entities must collect data, assess investments against each indicator quarterly, and report annually.

The six climate-related indicators include Scope 1, 2, and 3 GHG emissions, GHG intensity of investee companies, carbon footprint, fossil fuel sector exposure, non-renewable energy share, and energy consumption intensity per high-impact climate sector.

The eight broader ESG indicators cover hazardous waste ratio, emissions to water, biodiversity impacts in sensitive areas, violations of UN Global Compact Principles and OECD Guidelines, compliance monitoring mechanisms, gender pay gap, board gender diversity, and exposure to controversial weapons.

According to the European Supervisory Authorities' 2025 Annual Report on PAI Disclosures, data quality and consistency across PAI indicators remain areas for improvement, with the ESAs highlighting the need for better formalization of external data provider methodologies.

SFDR Reporting Timelines and Deadlines

The SFDR follows an annual reporting cycle. PAI statements must be published on the firm's website by 30 June each year, covering the preceding calendar year (1 January to 31 December). The next PAI reporting cycle is due 30 June 2026, covering the 2025 financial year.

PAI indicators must be calculated at the end of every quarter and then averaged for the annual submission, according to the SFDR Regulatory Technical Standards. Reports must also include year-on-year comparisons, eventually covering up to five reference periods to show trend data.

Pre-contractual disclosures must be updated whenever material changes occur, and periodic reports are published alongside the fund's annual report. Website disclosures must remain current and accessible at all times.

SFDR 2.0: The Proposed Overhaul

On 20 November 2025, the European Commission published a legislative proposal to comprehensively overhaul the SFDR, commonly referred to as "SFDR 2.0." According to Paul Hastings' analysis of the proposal, the changes represent the most significant revision since the regulation's inception.

The proposal replaces the current Article 8 and 9 classification system with three mandatory product categories. Transition (Article 7) products invest in companies or projects on a credible transition path. ESG Basics (Article 8) products integrate sustainability factors without meeting the higher category criteria. Sustainable (Article 9) products pursue specific environmental or social objectives. Each category requires a minimum 70% investment commitment aligned with the category's objective and a compulsory list of exclusions, including controversial weapons, tobacco, and specific fossil fuel activities.

Additionally, the proposal removes entity-level PAI disclosures and remuneration transparency requirements, deletes the existing "sustainable investment" definition to reduce interpretation challenges, and introduces a new Article 6a for funds that wish to make limited voluntary sustainability disclosures.

According to Morningstar Sustainalytics' analysis, the new regime could significantly reshape the market: Article 6 funds may rise from 41% to between 52% and 70% of the EU fund market, while the ESG Basics segment could shrink to 32-41% of assets under management.

The proposal is currently moving through the EU co-decision procedure, with trilogues between the European Parliament and Council expected during 2026. According to Freshfields' 2025 analysis, the regulation is proposed to apply 18 months after entry into force, with firms needing to adapt before the implementation deadline. Existing SFDR obligations remain fully applicable until SFDR 2.0 is finalized and enters into force.

How AI Streamlines SFDR Climate Data

Six of the SFDR's 14 mandatory PAI indicators are climate-related, requiring precise GHG Protocol-compliant emissions data across Scope 1, 2, and 3 categories. Net0 provides an AI-powered sustainability platform that automates the collection, calculation, and reporting of emissions data required for SFDR compliance.

Net0's platform integrates with over 10,000 enterprise data sources and applies more than 50,000 emission factors to convert raw operational data into auditable emissions figures in real time. This automated approach addresses a core challenge identified by the European Supervisory Authorities: the difficulty of collecting consistent, high-quality data for PAI reporting across diverse portfolio companies.

For financial market participants preparing their annual PAI statements, Net0's platform calculates emissions at the end of every quarter and generates the averaged annual figures required by the SFDR's Regulatory Technical Standards. Net0's reporting capabilities extend across 30+ regulatory frameworks, including the GHG Protocol, the IFRS S1 and S2 standards, the CDP, the GRI, and the SEC Climate Disclosure rule, enabling firms to meet overlapping disclosure requirements from a single data source.

Book a demo to see how Net0 can streamline emissions data management for SFDR PAI reporting.

Frequently Asked Questions

What is the SFDR and when did it take effect?

The Sustainable Finance Disclosure Regulation (SFDR) is an EU regulation that took effect on 10 March 2021. It requires financial market participants and advisors to disclose how sustainability risks are integrated into investment decisions and products.

Who does the SFDR apply to?

The SFDR applies to EU financial market participants (asset managers, pension funds, insurance-based investment providers), financial advisors, and non-EU firms marketing products to EU investors. Entities with 500+ employees face additional mandatory PAI reporting.

What is the difference between SFDR Article 8 and Article 9 funds?

Article 8 "light green" funds promote environmental or social characteristics alongside financial objectives. Article 9 "dark green" funds have an explicit sustainable investment objective as their primary goal, with more stringent disclosure requirements.

What are the 14 mandatory PAI indicators under the SFDR?

Six are climate-related (GHG emissions, carbon footprint, fossil fuel exposure, energy intensity) and eight cover broader ESG factors (hazardous waste, water emissions, biodiversity, UN Global Compact violations, gender pay gap, board diversity, controversial weapons).

When is the SFDR PAI reporting deadline?

PAI statements must be published by 30 June each year, covering the preceding calendar year. The next deadline is 30 June 2026 for the 2025 financial year. Indicators must be calculated quarterly and averaged annually.

What is SFDR 2.0 and how will it change the current framework?

SFDR 2.0 is a European Commission proposal published 20 November 2025 to replace the Article 8/9 system with three categories: Transition, ESG Basics, and Sustainable, each requiring 70% minimum investment alignment and mandatory exclusions.

How does SFDR relate to other EU sustainability regulations like the CSRD?

The SFDR works alongside the CSRD, the EU Taxonomy, and the ESRS. While the CSRD requires corporate sustainability reporting, the SFDR governs how financial products and firms disclose sustainability integration to investors.